Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – How inflation impacts different investments, Fed rate watch, New enhanced FDS legislation and more…

Issue: 25th June 2021

On Wednesday, the Federal Reserve released a new set of eagerly anticipated economic projections. The questions on everyone’s lips was, of course, inflation – what can we expect? And, interest rates – how soon can we presume to see a rise?The Fed has two mandates: maximize employment and keep prices stable at around 2%. When the pandemic first hit, the Fed’s policy response – cutting interest rates and buying up a bunch of bonds – helped on both fronts. Fast forward to today, and inflation is running far higher than the Fed’s target rate while the jobs market still needs time to convalesce. If the Fed were to raise rates, that would help inflation, but it would also slow economic growth and hurt the recovering labour market. By keeping rates steady, though, it’s risking even more significant inflation.

The members of the Federal Reserve Open Markets Committee (FOMC) are nearing a tough choice.For now, they’ve decided that the jobs market remains the bigger concern. In its June meeting, they gave no indication with regard to cutting back on their aggressive bond buying program and made the decision to keep interest rates at near zero levels (albeit indicating the possibility of two rate rises as soon as 2023). On this basis, it raised its headline inflation projection a full percentage point higher than its March projection to 3.4%.

While the Fed continues to say this will all be transitory (the board still believes the long-run forecast remains near 2%), it’s hard not to ponder if that at least in part this inflation gain is here to stay.

How Inflation Impacts Different Types of Investments

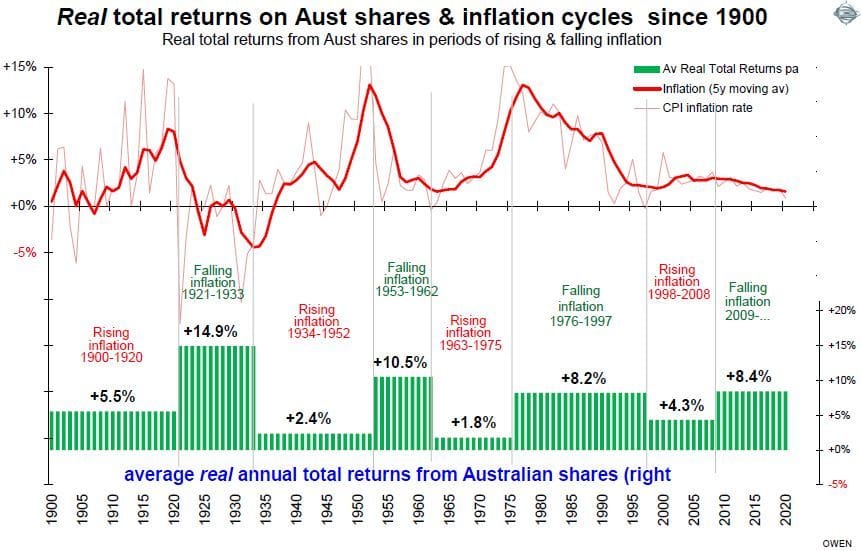

Continuing on with the inflation theme, this week we bring you a remarkable study by Chief Investment Officer, Ashley Owen of Stanford Brown. It charts the impact of inflation on 120 years of Australian asset performance, including shares, property, bonds and precious metals.With inflation surfacing, it’s essential reading.

Key takeaways include:

- The recent above-average returns are not sustainable unless inflation remains low and/or keeps falling

- All asset classes perform worse with high/rising inflation

- Shares post the highest returns in all inflation conditions across a full cycle

- The temptation to chase speculation in a lower-return world will be stronger (investors beware)

- Asset allocation does not change radically in rising/high inflation conditions

- (Shares do best, followed by commercial property (post pandemic warehousing and industrial are on the rise whether retail and office space come back remains to be seen), housing in the middle, then bonds and cash at the bottom with the lowest real total returns).

- Active management, particularly asset and sector selection combined with tactical shifts, will be increasingly important.

The positive aspects of the inflation shift will, of course, be that portfolio income (dividends from shares, rents from real estate, interest from bonds) are likely to be higher than in the low/falling inflation phases. In addition, asset price volatility is also likely to be lower, especially for equity markets.In this environment, now more than ever, the key to equity investing will be in-depth research and selectivity. Whether it be growth or value, this means companies and other assets with genuinely rising profits, dividends and income streams and spelling the end of a cycle where good returns can simply come from investing in an index.

Chart of the Week

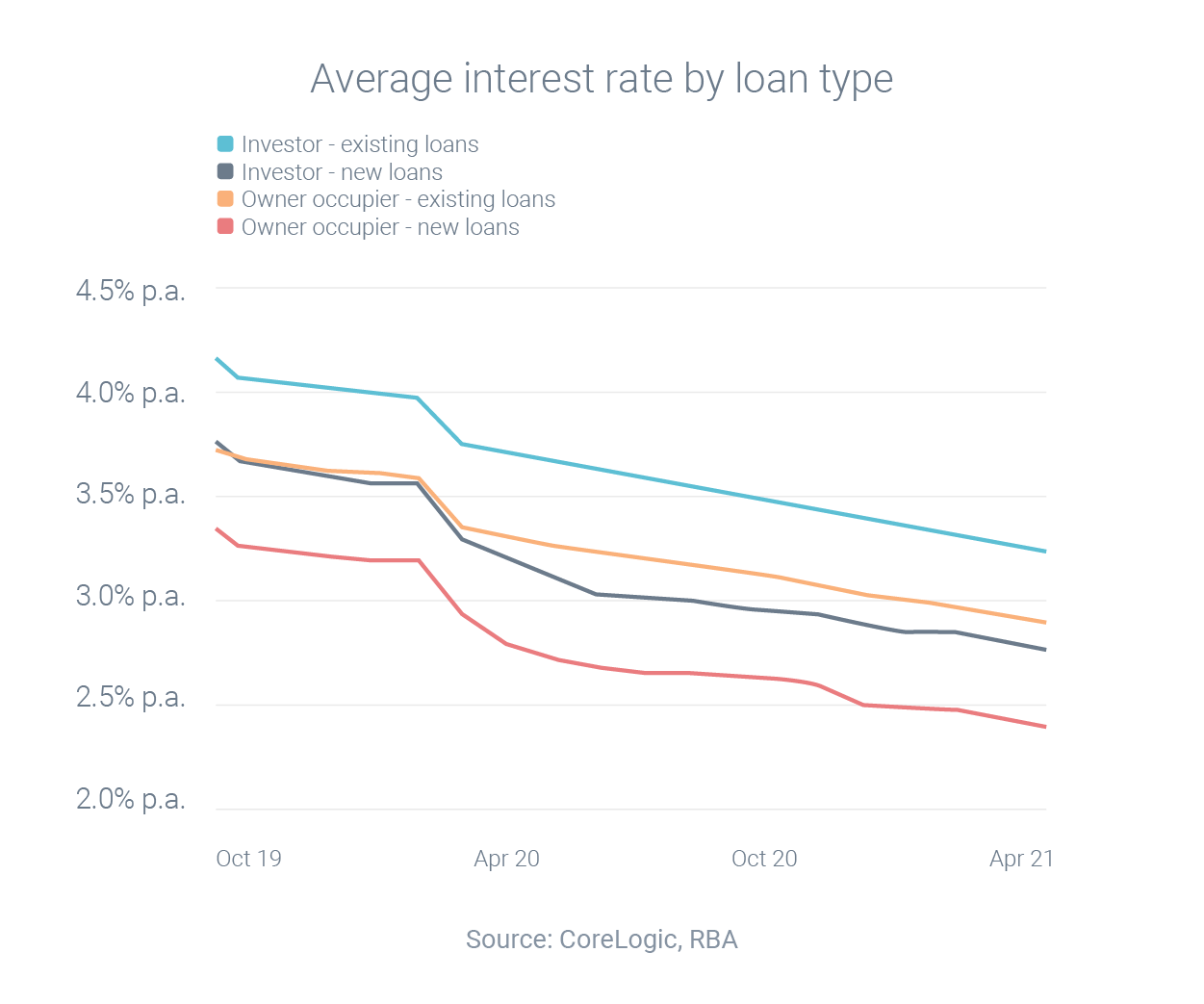

Our chart of the week may put a stone in the shoe of many. Apparently, many borrowers who stick with the same lender year after year are likely being slugged with a ‘loyalty tax’.According to new data from CoreLogic, owner-occupiers who took out new variable loans in April were charged an average interest rate of 2.77% p.a.. However, owner-occupiers with existing variable mortgages were charged an average of 3.10% p.a. a loyalty tax of 0.33 percentage points. Mmm, those interest rate differentials add up to a lot of money over the life of the loan!

If these stats have you reeling, don’t forget that as a client of FinSec you have access to our own in-house ‘debt specialist’, Brenton Moyle. If you believe a complimentary health check of your mortgage could be in order, please contact your adviser.

JP Morgan Investor Conference – The ‘Top Questions’ Answered

Earlier this month JP Morgan hosted its virtual APAC Investment Conference. Bringing together some of the biggest names in global investing, this is a coveted, invitation-only event. This week, we were fortunate enough to get our hands on the whitepaper summarising the conference’s “Top Questions” to provide a synopsis for our readers below.

What areas of the equity market are still showing signs of acceleration despite COVID?

- Many trends that were underway prior to the pandemic have accelerated over the past year, and the impact of the disruption is visible across multiple sectors.

- Rapid adoption of digital trends such as working from home, accelerated adoption of online alternatives for retail, payments, food delivery services etc. The companies that provide the hardware, software and support services to enable these changes have been key beneficiaries. The focus on big data, artificial intelligence and the shift to public cloud also accelerated during the pandemic.

- The healthcare space has also undergone accelerated innovation, not only in drug research but in the areas of telemedicine and remote patient monitoring. Covid-19 has resulted in rapid increases in alternative sites of care, with virtual appointments being one such example.

- Going green – We witnessed a migration away from metropolitan cities and millions of people who were spending more time at home required more stable power support. This is a durable theme where structural demand trends for battery growth and opportunities for distributed power management will continue.

How long can value continue to outperform growth?

- Over the past decade, and more specifically since the pandemic took hold in 2020, markets have seen a clear growth leadership until recently. After compounding at 20% returns for a decade, some of these growth companies, particularly the leading technology companies, represent an unusually large proportion of equity indices. These companies may be considered growth stocks, but they are exceptionally profitable, as evidenced yet again by a stunning set of earnings reports this quarter. The growth trends driving these profits look likely to continue for many years to come.

- Not all growth stocks are created equal – Software profits look more durable than earnings for hardware, such as smartphones. And while the valuations of the biggest companies seem broadly rational, there are some clear areas of excesses in mid-cap stocks in certain investment themes. Consider that at least five electric vehicle companies have projected USD 10 billion of revenues within seven years of earning their first dollar. The current record for this achievement, held by Google, is eight years as an example, making these claims in aggregate seem implausible.

- Value stocks look well-positioned to deliver strong performance in 2021:

- Strong earnings growth – We haven’t seen corporate earnings growth like this for a decade and believe the next two years of profits growth will act as a tailwind for lower priced companies.

- Extraordinary fiscal and monetary stimulus in much of the developed and emerging worlds will likely continue to fuel the earnings recovery.

- Even a modest rise in inflation should provide a tailwind for value stocks, given inflation links to the cost of equity and cost of money.

Is inflation transitory? What are the warning signals we should look for?

- Our market insights team believes that inflation in the U.S. should gradually ease in the second half of the year as the low base effect from last year fades and some of the supply side bottlenecks are resolved.

- We are monitoring wage inflation closely since supplementary unemployment benefits are creating some temporary distortions between labour demand and supply.

- We’re also seeing increases in other short-term consumer and producer price movements that have more to do with pent-up demand, pockets of supply constraints, and increased spending of stimulus money.

- The Federal Reserve is expected to start signalling its desire to taper bond purchases before the year-end and begin the process in early 2022.

How does the rising debt burden resolve itself?

- The high debt burden is less of a problem when borrowing costs are low, and central banks seem to be happy to provide support where needed via bond purchase programs.

- The risk from higher debt would come if inflation accelerates, leading to higher bond yields, or if governments were reluctant to consolidate their fiscal position.

- The ideal situation is for economies to resume consistent growth and this would allow governments, or borrowers, to grow out of their debt.

How will the role of retail investors cause hedge funds to rethink the way they invest?

- The prevailing view is that retail investors’ primary impact on financial markets is a change in trading patterns.

- Relative to institutional investors, retail trading is associated with markets that are driven more by sentiment factors and a generally shorter time horizon. This tends to manifest through an increase in volatility for securities heavily owned by retail investors. The implications of this dynamic can both present opportunities as well as increase risk.

Important Update: New Enhanced Fee Disclosure Statement (FDS) from July 1

As part of the 2019 findings from the Royal Commission into Financial Services, Commissioner Hayne recommended that the law should be amended to provide that ongoing advice fee arrangements (whenever made):

- must be renewed annually; and

- may neither permit nor require payment of fees from any account held for or on behalf of the client except on the client’s express written authority to the entity.

These recommendations were legislated in December last year and come into effect next week from July 1, 2021.Whilst Finsec has been operating in line with these new laws for several years (the changes simply make our process mandatory, rather than best practice), there are some significant developments regarding our FDS process that we would like you to be aware of.

For clients with an ongoing fee arrangement, moving forward, the law requires that you provide formal written consent on an annual basis:

- in order for us to continue providing ongoing advice and services; and

- for all providers to deduct fees from your account.

This consent will need to be provided within a dictated period of time.To simplify this process, FinSec has created a revised ‘Client Annual Renewal Agreement’. This agreement includes the documents required for legislative purposes and any supporting material as are necessary for broader context.

It is our intention that this agreement will be presented annually, in-person and where possible at your review meeting.More information will be provided in due course, however should you have any questions please do not hesitate to contact managing partner, Andrew Creaser.

Things that make you go MMM…

Tech company Canon has come up with an inventive way to tackle the problem of workplace morale: it’s installed cameras with AI-enabled “smile recognition” technology in the offices of its Chinese subsidiary Canon Information Technology. The cameras only let smiling workers enter rooms or book meetings, ensuring that every employee is definitely, 100 percent happy all the time.Apparently, the move is part of a larger trend of worker management. In April 2019, it was reported Amazon was instituting a system to track warehouse workers’ “time off task,” and in 2020 it was revealed the company used a “Relations Heatmap” to track employees’ likelihood of forming a union. Businesses can now buy software products that allow employers to monitor workers’ keyboard and mouse activity, GPS locations, emails and web-browsing activity.

“Workers are not being replaced by algorithms and artificial intelligence,” King’s College London researcher Adam Srnicek told the Financial Times, “Instead, the management is being sort of augmented by these technologies. Technologies are increasing the pace for people who work with machines instead of the other way around, just like what happened during the industrial revolution in the 18th century.”

Mmm… Or you could create a workplace where people trust each other to do the right thing and are actually happy to come to work.

Stay safe and look after one another. Enjoy the weekend and as always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.