Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Record dividends, augmented entertainment, iron ore & more…

|

Issue: 17th September 2021 |

| The September curse strikes again.

The S&P/ASX 200 has fallen nearly 2 per cent since the start of the month and is down 3 per cent from a peak a month ago, placing the benchmark on track for its first monthly loss since September last year. The decline comes despite increasingly good news on vaccination rates, which are edging higher with a greater local supply of vaccines, bringing closer the potential end to lockdowns in New South Wales and Victoria. The fall for Australian shares mirrors a decline in the US, where the S&P 500 has fallen by a similar margin since the start of the month. European shares have fared better but are also down slightly from a peak in early September. Fund managers are now coming to terms with the potential drop-off in terms of profits for the 2022 financial year after the lofty highs registered in this financial year to June (more on this below). In something of a surprise to the consensus view, the RBA has flagged a tapering of its bond purchasing program, announcing at the September meeting last week that asset purchases will be reduced from $5 billion a week to $4 billion a week. The move indicates the RBA foresees a sharp economic rebound once NSW and Vic begin to exit lockdowns, with its base case being positive economic growth in Q4 and solid growth through next year. The RBA was also resolute in its guidance that it does not expect to lift the cash rate until at least 2024. However, many experts say otherwise, including the esteemed Bill Evans (Chief Economist at Westpac) and an accurate predictor of RBA policy who believes it will likely be a year earlier. With valuations at the high end of fair value and the number of ongoing uncertainties, holding some cash as a defensive position may prove valuable. |

|

| The August profit reporting season is now behind us, meaning that most companies on the Aussie markets have told investors how they are tracking to 30 June. And, it didn’t disappoint. Companies lavished investors with almost $40 billion in ordinary and special dividends. Such has been the earnings recovery that it was almost double the dividends paid in a typical reporting period.

The bumper profit and dividend picture is well ahead of the target to recover from the 2020 collapse when aggregate profits fell from $101 billion in 2019 to just $36 billion. A fall outweighing that of the US, where many companies (e.g. the likes of ‘FANG’ Facebook, Amazon, Netflix and Google) were either not affected or boomed from the COVID lockdowns. Doing most of the heavy lifting is the resources sector and our big banks. Three companies accounted for approx. $30 billion of the gains – Fortescue Metals, BHP and Rio Tinto (Westpac, ANZ and NAB won’t report until November). A decade after the iron ore industry was assumed to have peaked, the combined profits from the big miners doubled those generated during the “mining boom” of 2011. What does this mean for investors?

Although the RBA is seemingly optimistic, there is no shortage of potential risks as covid lingers. The Australian economy may have avoided a ‘technical recession’ (two consecutive quarters of negative growth), but this is only due to the measurement method, i.e. the dates that make up a technical quarter. The earnings and dividends outlook could quickly sour if the virus mutates and lockdowns last longer than expected or if rising inflation resurfaces in the US, lifting expectations that central banks will have to raise rates sooner than expected. Dividends from the latest profit season should not be something we get used to.

|

|

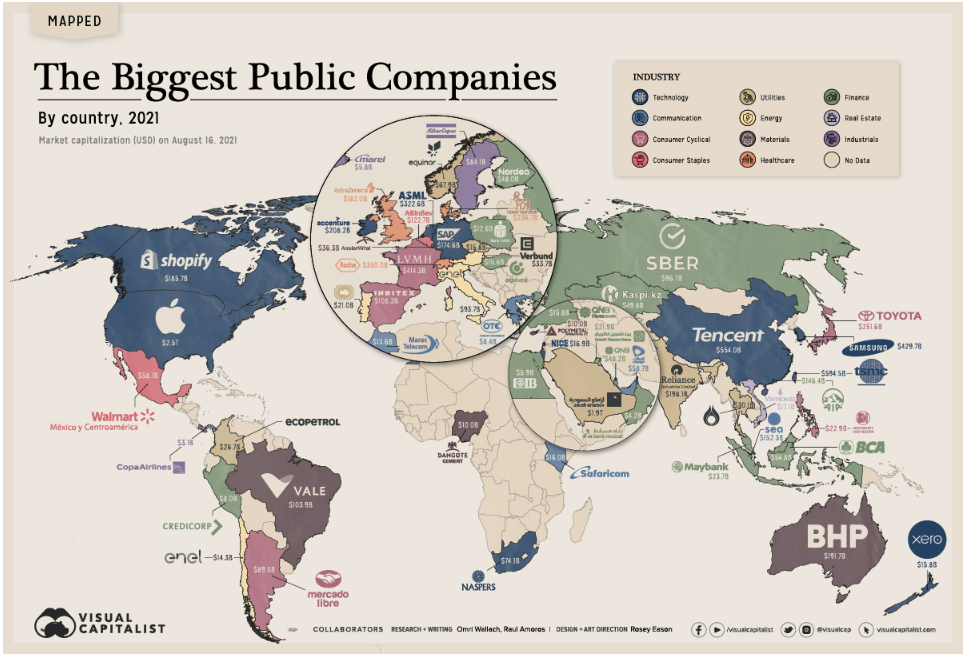

| Despite accounting for the largest market caps worldwide—with trillion-dollar companies like Apple and contenders including Tencent and Samsung—tech wealth is largely concentrated in just a handful of countries.

So what are the biggest companies in each country? Visual Capitalist has mapped the largest company by market cap across 60 countries in August 2021 – These are the companies currently polarising the 60+ stock exchanges around the world.

|

|

| If Darryl Kerrigan was penning this missive, “tell him he’s dreaming” would have been his response to anyone touting that iron ore prices would reach above US$200+ per tonne. After all, 18 months ago, federal, state governments and every expert in between had factored in US$50 per tonne at best.

How quickly we forget! Now accustomed to the big numbers, this morning’s headlines were all but reporting the demise of iron ore as it drops towards US$100 per tonne (not a free fall, just back to 2020 levels…).

Rout, healthy adjustment or just a simple case of supply and demand? On the supply side – Iron ore broke away from other commodities in January 2019 when the worlds largest exporter, Brazil’s Vale was taken out of the market by a catastrophic dam collapse that closed its main ore mines. Due to covid lockdowns, these mines and ports have remained closed ever since. With Vale out of the market and Chinese demand remaining strong, iron ore prices have kept surging. Australian mines and ports have kept operating throughout the pandemic and have reaped the windfall accordingly. Now that covid is easing, Brazil has been making a strong return to the market, with analysts estimating that their supply of iron ore has increased by 12% this year. On the demand side – China is still heavily reliant on Australia for iron ore. It has been trying to develop alternative low-cost supplies, particularly in Africa, but this is still many years away (the lead time from exploration to mining is not a short one). Our view remains that the threat of import penalties, like those inflicted on other Aussie imports, is low until China has genuine options. At the start of August, China did inflict a penalty of a different kind when it ordered dramatic cuts to steel production, primarily to reduce greenhouse gas emissions (many theorise they do not want a cloud of smog hanging over Beijing for the Winter Olympics in Feb 2022). Regardless it triggered sharp falls in the spot price of iron ore and the miner’s share prices followed suit. Will iron ore prices, profits and dividends resume their lofty highs? Unlikely. Chinese construction and infrastructure spending will remain relatively strong albeit at softer levels (China has now urbanised half of its population, bringing years of massive growth and industrialisation – the explosiveness has dissipated), but as Brazil continues to open up and Pilbara output increases (there are several unlisted smaller mines expanding output) supply is likely just as an important lever keeping prices in check.

|

|

| You’ve seen the headlines, and possibly the for sale signs dotted along suburban streets: property is booming and people are cashing in. When covid first hit in March 2020, industry pundits were predicting falls of around 30 per cent. Instead, over the past year, Sydney house prices have risen almost 23.8 per cent, Melbourne 16 per cent, Brisbane 23.1 per cent and Adelaide 18 per cent – the fastest rise in 30 years.

The responsible parties are, of course, the homebuilder incentives (this uncapped government program exceeded Treasury’s objectives for new dwelling construction by 330%), pent up savings, constrained investment choices and low-interest rates. Is it sustainable and for how long? In this article from the inside investor, finance journalist Ishan Dan looks at why some experts are forecasting a base case with a significantly larger decline than the consensus view or that of the RBA. Spoiler alert, excess housing and immigration come into play. Read the full article here.

|

|

| In the last View, it was autonomous vehicles, this week it’s digital entertainment in part 3 of our Capital Group series on the ten most exciting (and in some cases life-changing) developments they believe will shape our world in a decades time.

Content is king. But the platform is the kingdom. They say the entertainment of the future will feel more like it’s in the real world and less like something we sit and consume through a screen. We’ll walk into the action, be part of the theatre, and create simultaneously. Imagine being able to have your favourite band come and perform in your home for your birthday. Or explore a stage from behind the scenes while the actors are performing. The show will go on, and we’ll be in it… Investment director Brad Barrett believes that in 2030 it will be all about the digital platforms that offer the richest ways to experience entertainment, at the lowest prices as virtual reality grows in leaps and bounds. The shift to streaming content accelerated in the wake of covid, but it may still be in its earliest stages. Roughly one-third of all content consumption is currently transacted via streaming, but by 2030 I think that’s going to increase to more than 80%. You have this incredible combination of streaming being both better and cheaper than traditional television, and I don’t see that changing. The network effect can be extremely powerful — the bigger a streaming platform gets, the more it can reinvest in content, which could help lower costs and attract even more users. Due to economies of scale and high barriers to entry, I expect a winner-take-most market structure in the future, and those are the type of companies I want to be invested in. Similarly, the video game industry will likely continue its explosive growth into the next decade. I also suspect virtual and augmented reality will become more mainstream. As the technology evolves, these may even achieve an experience similar to attending a concert, sporting event or show, but likely at a fraction of the cost. With all this content streaming directly into our homes one must wonder what innovation traditional businesses such as cinemas will create to remain relevant.

|

|

| The Natixis Global Retirement Index evaluates how 44 countries manage material wellbeing, health, finances and quality of life for their citizens in retirement.

With an overall score of 76%, this year Australia remained in seventh place behind Iceland, Switzerland, Norway, Ireland, the Netherlands and New Zealand. According to the report, Australia’s ranked particularly well in two areas — fourth in finances for retirement and 10th for health — while it was ranked in the top 16 countries for quality of life. Conversely, scores for the bank non-performing loans, interest rates, old-age dependency and government indebtedness indicators all dropped compared to a year earlier. Natixis derived its results based on a survey of 400 Australian investors, 19 per cent of whom were classified as high net worth more than US$1 million in net investable assets, with a further 22 per cent classified as emerging high net worth with US$500,000 to $1 million in net investable assets. Despite this representation, 35 per cent of Australian investors said they were worried retirement would not be an option, and 31 per cent agreed they would never have enough money to retire. The survey highlights the need for Australians at all levels of wealth to engage with their retirement. Working with a financial adviser to develop a plan tailored to the needs and goals of the individual will always highlight strategies they may not have even considered. In fact, the data tells us that the portfolios of advised Australians are approximately 5.2 per cent better off than the non-advised (value of and adviser report, Russel Investments). The Natixis Global Retirement Index report can be found here. |

|

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |

|

|