Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Property, Gas & oil, Revenge of the deadly trinity of zeroes and More…

|

Issue: 29th October 2021 |

| As we head into the final quarter of 2021 cautious optimism, both economically and socially sums up our feeling at present. Sydney and Melbourne are emerging from their long lockdowns, summer is coming, and Australian vaccinations rates are high and moving higher. If we look to similar countries overseas, high vaccination rates are increasingly allowing people to move back towards the lives they’re used to living. The pandemic is moving off the front pages and lower in people’s consciousness.

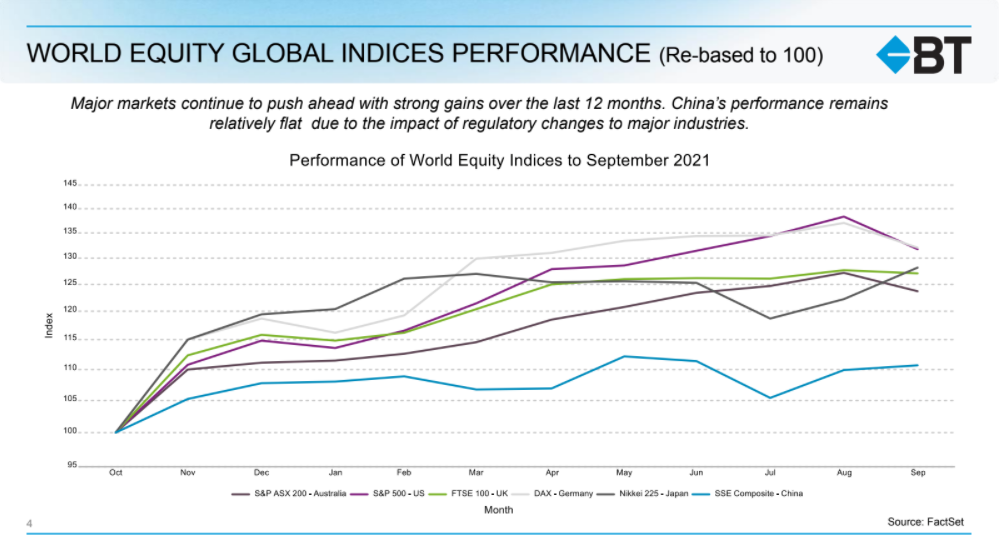

Markets and economies seem to be following a similar theme. Economies around the world are reopening and border restrictions are loosening, though supply chain pressures remain. Global equity markets continue to rise: the MSCI All Country World index rose 3.9% over the last quarter and Australian equities increased too, albeit at a slower rate. The S&P/ASX 300 Accumulation index gained 1.8% over the last quarter, although have now given back 1.3% at the time of writing. Now for the cautious bit. Three main areas are causing consternation, with the potential to destabilise the recovery. Firstly inflation, which continues to be furrowing brows as it creeps higher. Is it a transient blip, or do we need to bring it down? Secondly, geopolitics – China and the US continue their high-level jockeying for position, gradually increasing tension and drawing other countries into the struggle. Thirdly, equities, still the shining light for investors as ultra-low interest rates continue, but how long can it continue (more on this later in the View)? For our avid readers no surprises here – these are all themes we have unpacked many times before in past Views. While these risks remain, we think the outlook for financial markets is largely positive (with a cautious caveat). Governments look set to continue their economic support packages and central banks seem similarly set on keeping interest rates low as long as possible. This is likely to drive a surge in economic activity as countries and economies reopen and both businesses and consumers have the confidence to spend.

|

|

| Headline writers reaching for superlatives to describe the rise in Australian house prices in the last 12 months (up 19.3% on the CoreLogic 5 Capital City Aggregate) make regular references to ‘the fastest increase in 33 years’. So, what was the story in 1988? In just one quarter (June 1988), residential property prices rose 9.6%, but that’s where the similarities end.

Between September and November 1987 (who could forget Black Monday/Tuesday), the ASX fell 50% and thus prompted an asset switch to the security of property, both commercial and residential. Kicking it along, the cash rate fell 1.5% between September 1987 and June 1988. Cash rates down, money flowing into property… Sounds like 2021? Not quite. The cash rate fell from 15% to 13.5%. Such rates would bury current day borrowers financing at around 2% when the 2021 debt to income ratios are profoundly different. What’s more, the current flows to property are not a switch from equities, which are themselves experiencing major inflows. The 2021 property boom is funded by the ready availability of debt. And, here’s another difference. Back then, while paying a mortgage at 13.5% was no mean feat, inflation was also high, and wages kept pace with rising prices. Over the years, the debt was inflated away, such that most people had paid off their mortgage when they entered retirement. Today, inflation is low and therefore, debt retains its current value for longer into the future. If someone takes a loan for six times their income (according to the Australian Prudential Regulation Authority (APRA), 22% of new mortgages in the June 2021 quarter went to borrowers with debt-to-income ratios above this), while they can service the interest repayments due to low rates, they make little inroads into the principal. Inflation no longer fixes the debt burden, and far more people will potentially enter retirement with large mortgages. It certainly has long-term consequences. If superannuation becomes the vehicle for paying off the debt, then the retirement incomes of many Australians are set to be compromised – not to mention the ramifications for our social security system. The dynamic of real estate markets has changed dramatically and we watch with interest to see what comes next!

|

|

| Equities have continued to be the first port of call for most investors as ultra-low interest rates drag down returns in most defensive asset classes. The emergence of the Delta COVID variant, and subsequent slower economic reopening, has dampened, but not put out, the ‘equity glow’.

Conditions are, on the whole, positive toward equities continuing to deliver healthy returns. While expectations of a services boom as economies rebound may be slightly overblown, pent-up demand for travel, hospitality and entertainment will increase consumer spending in many countries. Just as the great lockdown created many winners (home delivery, electrical goods, internet services) and losers (tourism and hospitality) it is reasonable to expect the same in reverse as countries reopen. While this is likely to cause markets to continue to rise overall, we expect it could be a bumpy ride as policy decisions rumble through global markets and companies readjust to a new phase of the pandemic.

|

|

| Europe’s gas prices surged again over the last week after it was confirmed that Russia would not be increasing gas supplies to continental Europe.

Now, sitting at over $30/mmbtu (metric million British thermal units), Europe’s gas price is at a record high, having risen threefold year to date. Causing the shortage is a combination of the strong rebound in economic activity, supply issues, underinvestment in power infrastructure and a continent heading into winter. Even if Russia does decide to supply some additional gas in the foreseeable future, Europe is unlikely to find enough volume from traditional suppliers to fill the deficit quickly – making for an expensive and strained winter period. The best hopes now lie with a mild northern hemisphere winter. Flow-on effects In the US… The US gas price has more than doubled over the past year. Despite the US being home to an abundance of gas resources, until recently, low prices and weak balance sheets have left little incentive to invest in LNG exports. Consequently, the US has been a relatively small supplier in the global market. It is our view that we should expect to see US gas production and exports increase over the medium-term (even if just as a transition fuel until grid investment catches up to cope with the renewable generation). Consumers… There is a valid argument that this recent gas rally is also fuelling the oil rally. LNG and European gas prices are currently equivalent to over $150 per barrel of oil – versus an oil price of closer to $80 per barrel. This has led to an uncomfortable shift to burning oil in Asia. Whether OPEC will step in to increase oil output remains to be seen, but regardless consumers are going to feel the effects. Using the US as our proxy, half its power is derived from gas. The increase in prices implies there will be huge consequences to the cost of filling the tank and to direct fuel costs for gas power generators and household heating. For investors, there’s much to consider. If shutdowns in China’s industrial sector accelerate (power shortages have seen high energy sectors such as steel, aluminium and chemicals experience shutdowns), or if power prices continue to rise for industrial users, there will likely be implications for domestic and global economic growth. Note: Desperate to ease electricity shortages; China is opening up new coal production. According to The New York Times, this extra coal will increase humanity’s output of planet-warming carbon dioxide by a full percentage point. So, we have a (potentially) large cost to the global effort in fighting climate change, a very real risk of a power crunch across major economies and higher power prices through the winter months. As well as the impact to economic activity, this could have meaningful implications for inflation.

|

|

| After a couple of decades of falling and low inflation, expectations from policymakers have been that this state will continue for the foreseeable future. However, COVID-19 is causing massive disruptions to supply chains (read above) and shifting spending patterns. The result has been a spike in inflation, and while the official line has been that this spike will be transitory, pressures (read below) continue to build.

So, how should investors position themselves for such an uncertain economic and policy outlook? In this week’s white paper, fund manager Sage Capital considers three main scenarios.

|

|

| The world is on the cusp of a new ‘renewable’ revolution that is set to re-shape many of our supply chains, ‘low-carbon technologies’.

At the centre of this shift sits the humble battery. The growth of electric vehicles (EVs), and renewable power generation/storage, will increase demand for a range of raw materials. A rapid ramp-up of such technologies will require a concurrent increase in the materials used in them. Significant investments in mining and technology will be required to meet the needs of the burgeoning battery market. It’s got our Investment Committee’s attention and takes out our stat of the week!

The amount by which the global lithium supply will have to grow by 2030 to meet current projected demand for electric vehicles (source: Holon Global Investments).

|

|

| This week we end with an extremely interesting read from Mark Tinker, CIO of Toscafund Hong Kong and the founder of Market Thinking.

He muses that Central banks everywhere, have spent years trying to stimulate inflation through ultra-loose monetary policy and now that it is here, they’re not sure what to do about it. The problem being that in reality their policies have had nothing to do with the arrival of inflation and many, rightly, fear that if they now switch to tighter policy (i.e. raise interest rates) they will end up with the worst of all worlds, which is stagflation. Tinker believes that a combination of zero COVID fracturing global supply chains and, the ratchet effect of multiple rounds of zero-carbon policies on both energy costs and energy supplies have done the inflation job for them. However, the real problem now is that the inflation we are seeing is not in discretionary items, but in essential goods and services. This is a supply issue rather than a demand one and the idea of raising the cost of mortgages in a bid to collapse discretionary consumer demand makes no sense. It won’t change demand for the essential goods and services, they are, after all, essential, but it will affect everything else. The supply problems are of course a function of COVID restrictions, but they have revealed the fragility of the global ‘just-in-time’ supply chain. He believes this will be slower to unwind than we first thought. Meanwhile, climate activism (and the politics that go with it) are also having an impact on supply. Raising the cost of energy, or limiting its usage for zero-carbon reasons, will, by definition both increase the cost and reduce the supply of ‘stuff’. Tinker goes on to say that this all comes back to the concept of “The China Price”, essentially that because of its huge scale, whatever China wants to buy goes up in price and whatever China makes and is trying to sell goes down in price. China obviously knows its power here, particularly on the purchasing side, which is why periodically it seeks to choke off speculative buying of commodities like iron ore, but it is not clear if economic models have properly accounted for the disinflationary side of China i.e. ensuring that there are more than enough goods, or the impact that their disappearance will have (the shutdowns caused by the current power shortages, mentioned in our previous article have given an early insight into how this may turn out). On balance, Tinker surmises that we should expect to see a step-up in price levels rather than an inflation spiral, leaving markets to find a new equilibrium. The full article can be found here, noting that it is behind the paywall. |