Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Markets, Immigration, Magellan, Alex Carey and more

|

Issue: 10th December 2021 |

| It’s beginning to look a lot like Christmas. Decorations are out in force, trees adorn every office, and many Australians, newly out of lockdown, are out painting the town a festive shade of red. And while we have suffered through a touch of volatility over the past few weeks, December, as it has in previous years, has started with a bang (the ASX200 and S&P are both up around 2%).

It is quite extraordinary to think we are only three short weeks away from celebrating a new year. But, as we seem to say, every year … where has the last 12 months gone?! This View will be our last for 2021; however, you can still expect our customary ‘year in review and outlook for the next 12 months’ before the holiday break. In recent days our inboxes have been flooded with fund managers predictions for 2022, so we expect some good content. For today’s commentary, we cover markets, immigration woes, Australia’s impending wealth transfer, a note on Magellan and a big shout out to Alex Carey. We hope you enjoy the read. |

|

Equity markets are heading for their third consecutive above-average calendar year, and as discussed in Views before, at work here are three main drivers:

Over the last month, we have seen new developments on all three fronts. Firstly, on the virus front… The year began with COVID as the biggest threat to the economy, and it looks like it may end in the same way. Not surprisingly, the virus is still causing real economic consequences. Globally the number of cases has been rising again, particularly in Europe and parts of the United States. And, of course, more recently, we have the new Omicron strain. The good news in Australia is that the number of cases has come down from their highs, both in Victoria and New South Wales, but they are still lingering at reasonably elevated levels. What’s critical is the hospitalisation rate, and that shows that vaccines continue to work. In Australia, 78 per cent of the total population (including infants and children) have had their first dose. And 73 per cent are fully vaccinated. That’s above the developed nation average, and it’s still rising. The pandemic is far from over, but 2022 should see us move from the pandemic to the endemic stage of the virus. Vaccines are so far highly effective in preventing serious illness but are less effective in preventing infection and transmission. Health professionals are predicting if the hospitalisation rates can stay low then hospital systems around the world should be able to manage as re-openings continue. We still don’t know much about the Omicron strain. However, doctors in South Africa say it does not cause particularly severe disease (the World Health Organisation has urged caution given the limited data available). The pessimistic scenario is that it’s more transmissible and turns out to be more virulent than Delta, necessitating a rollout of new vaccines, which will delay the recovery. The optimistic scenario is that it’s less virulent, more transmissible and becomes the dominant strain. For those interested in understanding how this works, click here. On the monetary front, the key factor is the outlook for inflation. Initially, central bankers dismissed inflation as ‘transient’, but over the last month, one by one have admitted that they may need to accelerate their rate hike plans. Even US Fed Chair Jay Powell acknowledged that it might be time to retire the term, announcing (on the last day of November) that the risk of higher inflation has increased. Markets had already factored in earlier rate hikes, so the collective stirring to date hasn’t rattled markets too much. In our view, pandemic related pressures in supply chains are still in part transient and will subside as economies fully reopen and people’s spending habits shift away from goods and back to services. However, this could be offset by pressure in wages (as we have seen in the US) and energy prices (volatile oil prices was a major theme for November). Even with growth in economic activity slowing, we agree with experts that we won’t see core inflation in the US peaking until the end of next year. Australian inflation will also become more of an issue in 2022. Economists forecast that underlying inflation will get to about 2.6 per cent by the middle of next year, which is in the centre of the RBA target range. It’s likely to remain there, and hence why it is also likely that the RBA will raise rates towards the end of next year. From a fiscal perspective, the positive developments over the past month lie with the progress of Biden’s $1.2 Trillion stimulus package and, on his broader, $3.5 Trillion ‘Build Back Better’ programs focussing on welfare and climate change. The recent confluence of these drivers (uncertainties by any other name), along with liquidity constraints that often affect financial markets at year-end, will most likely be a recipe for volatility heading into 2022. The challenges facing central banks globally are complex, but they can also create opportunities for active investors that can nimbly respond to divergences in policy and asset prices.

|

|

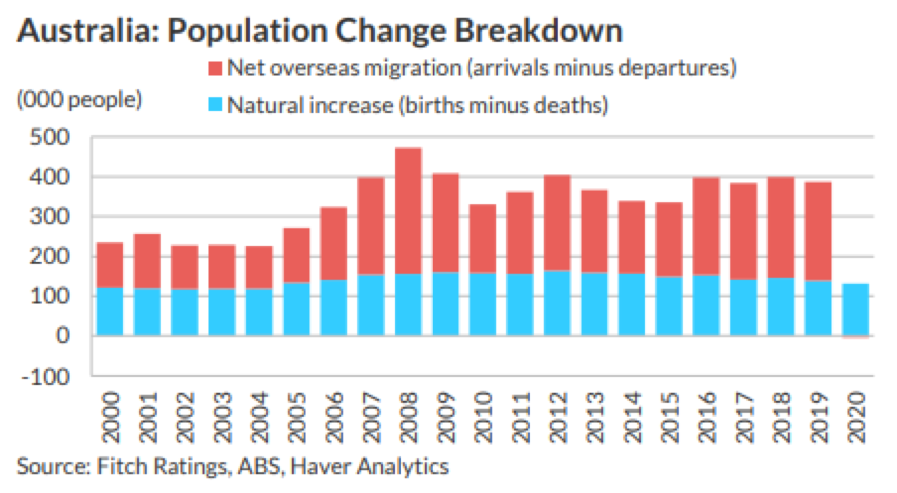

Migration and particularly the welcoming of skilled migrants, has been a central cog in the success of the Australian economic model. It has allowed the ‘Lucky Country’ to fulfil the need for everything from fruit pickers to doctors and engineers. Between 2000 and 2019, Australia experienced the fastest population growth among large developed markets. And for the last ten years, from a supply side, population growth has been the main source of growth for Australia’s economy. So, what happens when an economic model built on migration has to deal with a global pandemic and a sudden halt in the flow. The chart above tells a clear story of the dramatic cessation in net overseas migration due to the pandemic, and the chart below sets out very clearly what this has done for job vacancies.

Without a rapid return to immigration, Australia will likely run into capacity constraints in the coming years. This could likely lead to wage pressure over the next 24 months. The Reserve Bank published updated quarterly forecasts that showed wage growth could hit 3 per cent by the end of 2023 — it would be the fastest rate of growth in Australian wages for a decade. Typically, businesses will pass through higher labour costs into prices to preserve profit margins in an environment of strong demand. Then we certainly would have inflation. Only time will tell how quickly the migration tap can be turned back on in a world still significantly disjointed… |

|

| Many of you would have seen the Magellan media coverage over recent weeks.

Unfortunately, the press has chosen to be quite negative about Magellan as a business, a fund manager and the personal lives of those at the helm – seeking to combine a number of issues and speculative rumours in their coverage. This week’s departure of Chief Executive Brett Cairns added further fuel to the innuendo fires. There has also been much talk of their underperformance over the last 12 months, an issue we have already discussed with many of you. We would like to reiterate that we remain comfortable with Magellan’s approach, believing that the fund’s conservative strategy through the pandemic has delivered and continues to deliver a level of diversification that remains important. To address any concerns our clients may have, we are hopeful of securing Hamish for a Q&A session in the New Year. We will keep you informed accordingly.

|

|

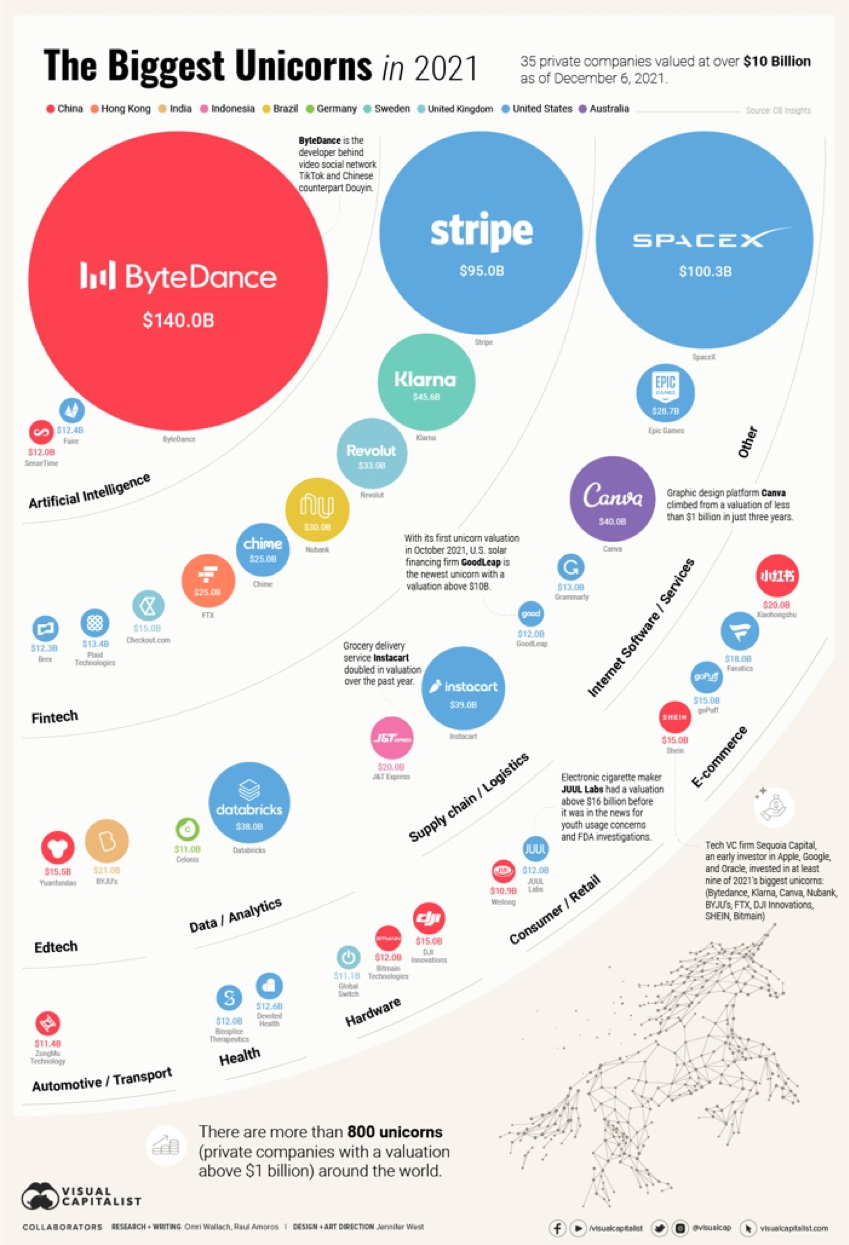

| The World’s Biggest Startups: Top Unicorns of 2021

Many entrepreneurs start businesses, but only the most successful new companies hit “unicorn” status (a valuation above US$1 billion). Some unicorns are little-known companies making quiet but impactful strides in software, healthcare, automotive, and other fields. Others have already become well-known industry leaders and household names. In total, there are more than a phenomenal 800 unicorn startups globally – too many to visualise! Instead, our chart of the week hones in on the world’s decacorns (unicorns with valuations above $10 billion) as of December 2021, according to CB Insights intelligence platform.

To enlarge, click on the image, alternatively view by clicking here. |

|

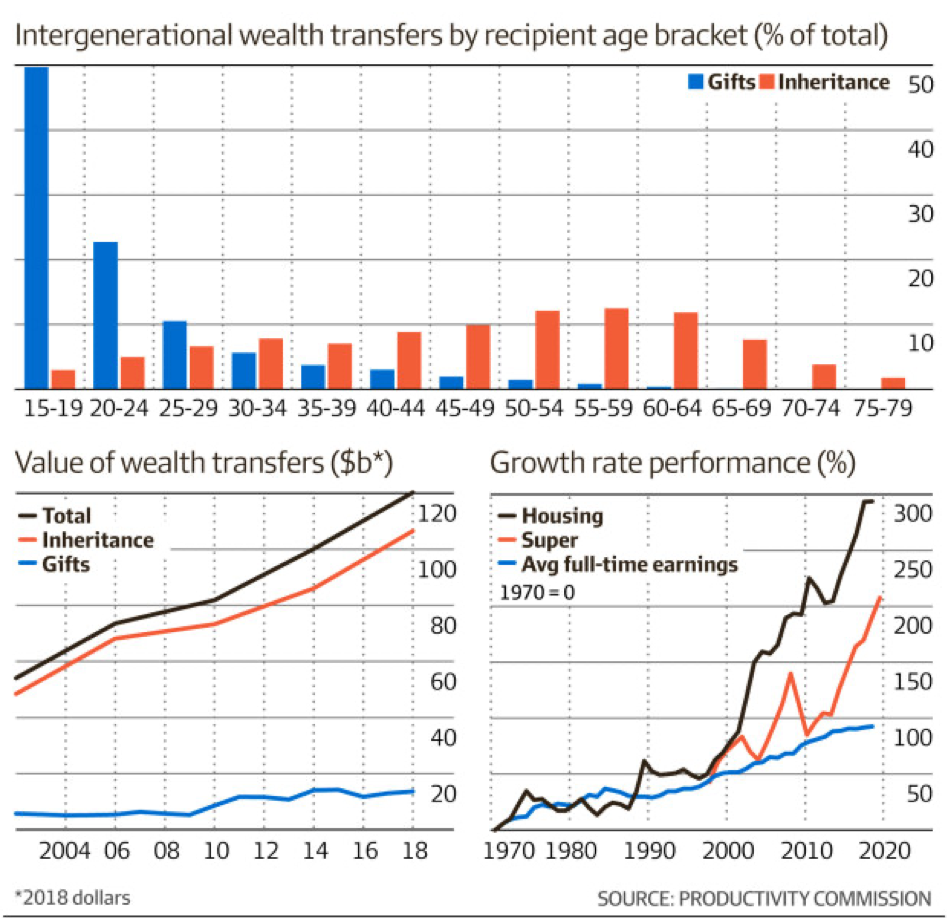

| Baby Boomers will pass on an estimated $224 billion each year in inheritances by 2050 as record housing, super wealth, and fewer heirs create a $3.5 trillion bonanza for younger Australians.

In the first-ever official study of wealth transfers in Australia, the Productivity Commission has projected a fourfold increase in the value of inheritances over the next 30 years.

The $224 billion estimates are based on the finding that $1.5 trillion was transferred between Australian generations between 2002 and 2018, 90 per cent of which was made up of inheritance payments and the remainder of gifts to mostly younger adult children. Assumptions on housing and sharemarket returns are factored in, along with expectations that the older generation will hold a growing share of the total wealth (longevity rates are increasing) and have fewer children to bequeath to because of lower fertility rates. The report, released this week, found the main beneficiary of inheritances, in absolute terms, are people who are already financially comfortable. “The average recipient of an inheritance was, at about 50 years old, close to peak earning capacity, established in a house..” About 90 per cent of transfers were inheritances from deceased estates. The rest was mainly made up of gifts to adult children. Just 2 per cent of wealth transfers went to charities. Mmm… With current capital gains tax legislation and the death tax within superannuation, the government could be in for a windfall as the baby boomer generation passes.

|

|

| It is near-impossible to ignore cricket during an Aussie summer, and with the Ashes on Aussie soil, this year is already promising to be a big one…

Here at FinSec, our level of enthusiasm is already in top gear! On Wednesday, our own Alex Carey (Alex worked as a Client Services Officer with FinSec up until full-time cricket took over in 2016… and yes, we still like to claim him as our own) made his test debut and didn’t disappoint. Taking three catches in a solid performance behind the stumps and a stabilising partnership with Travis Head in his maiden innings with the bat, we will be watching with great interest as he (hopefully) continues to shine throughout the rest of the series. A huge congratulations to Alex; we couldn’t be more proud of your achievements!

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |

|

|

| We have enjoyed receiving much positive feedback in relation to this publication. Many have asked if they can share with family and friends and we would be delighted if you did! To ensure the integrity of the links please forward via the ‘send to a friend’ link at the very bottom of this email. |