Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Berkshire Hathaway AGM, Baby Bust or Boom, Compare Pears with Pears, Wages Growth and More.

20th May 2022

It’s election eve, and this week the coalition found a new policy to give their campaign some last-minute momentum. It is, of course, Mr Morrison’s ‘it’s your money’ scheme which would allow first home buyers to withdraw 40 per cent of their super up to a maximum of $50,000 to put towards the purchase of their first home.

With much of the policy detail yet to be released, the merits of the proposal remain to be seen. However, in a clever political twist, where on sale of the home, the amount taken out plus a proportion of capital gain must be put back into super – we think Mr Morrison will be pretty pleased with himself. It is hard for Labor to argue the scheme is a raid on retirement savings and, as industry funds are structured to benefit from the massive mandated cash flow from contributions, anything involving money going out will cause them to have to rethink their strategies. For more context, our ‘compare the pears with pears, not apples’ article further down the page is a good read.

This week’s data threw up mixed messages, which didn’t help our politicians much either. The unemployment rate was down to 3.9%, yet wages growth was only 0.65%. Naturally, Morrison is stroking the unemployment rate and Albanese the low wages growth. Interpretive data is always about context! More on wages growth below.

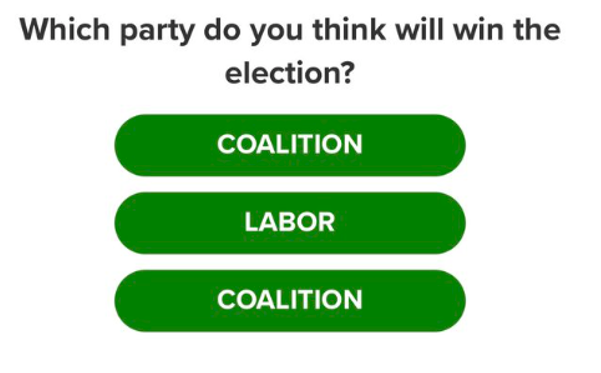

Who will come out on top tomorrow night is hard to call. Polling numbers don’t necessarily help, particularly when systems are compromised, such as this graphic televised on Nine during the final leader’s debate.

Let’s hope that whoever it is, the weeks and months ahead bring us a calm, informed examination of the many issues that face this country, and a determination to do something about them.

On that note, happy voting tomorrow! For added fun on Saturday night, you can’t go past Election Bingo (courtesy of Firstlinks). The clichés the politicians and commentators rely on are sure to get a run. The first person to complete a row or column wins. For a print-friendly version, click here. If you are planning an election party, saddle up for a late one; it is predicted that up to half of all votes this year have been cast pre-election, it may be sometime before we have a result.

Market Update

Markets remain shaky, with US indexes all on track to finish the week down at least 2.9%, while interestingly, the Australian market rose strongly as the week ended.

The themes spooking markets remain unchanged:

- Russia’s war on Ukraine – Sanctions against Russia and supply chain disruptions have intensified shortages of key commodities, stoking inflation.

- Inflation is hovering at a four-decade high in the US and, central banks are making it very clear they will not risk inflation spiralling out of control.

- Rising interest rates – investors continue to move away from the speculative end of the market (junk bonds, meme stocks, cryptocurrency and fast growing tech companies). Pandemic stars such as Netflix and Zoom have also suffered recently, as investors re-evaluate how much consumer behaviour really has changed.

- China’s lockdown – Chinese manufacturers struggle to keep factories going and, truck routes and ports are severely disrupted. Consumer demand has also taken a big hit, casting a shadow over the country’s economic outlook.

Considering the current environment, where markets are susceptible to good or bad news, we expect the situation to remain choppy for some time to come. However, among the many messages investors receive when markets fall is this useful reminder from Shane Oliver of AMP:

“If you look at the daily movements in the share market, they are down almost as much as they are up, with only just over 50% of days seeing positive gains. But if you only look monthly and allow for dividends, the historical experience tells us you will only get bad news around a third of the time. Looking only on a calendar year basis, data back to 1900 indicates the probability of a loss slides to just 20% in Australian shares and 26% for US shares. And if you go all the way out to once a decade, since 1900 positive returns have been seen 100% of the time for Australian shares and 82% for US shares.”

Berkshire Hathaway Comments – Annual Shareholders Meeting

Investment teams from around the world ( a mere 20,000 plus enthusiasts…), descended on Omaha, Nebraska, earlier this month to make the pilgrimage to the Berkshire Hathaway AGM. This meeting was significant in that it was the first live AGM since Covid-19 and likely one of the last meetings where both Warren Buffett (91) and Charlie Munger (98) attended together in their current capacity within the firm (both have recently reduced commitments outside of Berkshire). Both took to the stage for a remarkable 6 hours, offering their characteristic wisdom and entertainment over 21 questions from shareholders.

Berkshire Hathaway is likely one of the most studied organisations on the planet, and yet seemingly no one has been able to replicate what they have achieved over the last 53 years. This suggests that beyond their well-studied process, the intangible factor that can not be replicated is the famous ‘Buffett and Munger magic’. We can only imagine that attending the AGM in person is to witness this phenomenon first-hand. Today we share some of the more poignant ‘Warren and Charlie’ wisdom from the April 30th meeting.

- On cash

“We believe in having cash. If you don’t have cash, you don’t get to play the next day. It is like oxygen, it is there all the time and if you don’t have it for a few minutes, it is all over.” – Warren Buffet

- On oil

“I have a different view to most on this subject. I like having the reserves. If I were running the United States, I would just leave most of the oil we have here, and I’d pay whatever the Arabs charge for their oil and I’d pay it cheerfully and conserve my own. I think it’s going to be very precious stuff over the next 200 years. Nobody else has my view – it doesn’t bother me – I just think they’re all wrong”. – Charles Munger

“It was not long ago that the idea that anybody produced a barrel of oil was somehow, something terrible… In the end, I think at the moment, at least, most people feel that it’s nice to have some oil in this country than not have it. And we’re using a lot of it. And if we were to try and change over (to alternative energy sources) in 3 years or 5 years, nobody knows what would happen, but the odds that it would work, well are extremely low”. – Warren Buffet

- On inflation

“Nothing in economics is the same the second time after it happens the first, because the first affects people’s attitudes, and the second, their attitudes always influence the activity itself. I mean, it is an interesting phenomenon. There are people who write a textbook and they really run it based on the last experience. People read the textbook, so they behave differently next time. And they wonder why they’re getting a different result than they got the time before”. – Warren Buffet

“The best investment by far is anything that develops yourself. If you’re the one they pick out to do any particular activity – sing or play baseball or be their lawyer, whatever it may be -whatever abilities you have can’t be taken away from you. They can’t actually be inflated away from you.” – Warren Buffet

- On bitcoin

“I got some advice for you. When you have your own retirement account and your friendly adviser suggests you put all the money into bitcoin, just say no”. – Charlie Munger

“…if you told me you owned all of the Bitcoin in the world, and you offered it to me for $25, I wouldn’t take it because what would I do with it? I have to sell it back to you one way or another. I mean maybe I’m insane people, but it isn’t going to do anything…. that explains the difference between productive assets and something that depends on the next guy paying you more than the last guy got”. – Warren Buffet

- On investing

“Markets do crazy things and occasionally Berkshire gets a chance to do something. It’s not because we’re smart. It’s because the only thing I say we’re qualified on is that I think we’re sane. And that’s the main requirement in this business.” – Warren Buffet

“It’s almost a mania of speculation that we now have. We have computers with algorithms trading against other computers. We have people that know nothing about stocks being advised by stock brokers who know even less.” – Charles Munger

“We haven’t the faintest idea what the stock market is going to do when it opens on Monday. We never have had. We have not been good at timing. We’ve been reasonably good at figuring out when we were getting value for our money.” – Warren Buffet

Baby Bust Or Boom

We have a new theme headlining global demographics.

Since the years of the Baby Boom, fertility rates in Australia and around the world have long been in decline. From 3.55 babies per woman on average in 1961, fertility rates fell to around 1.74 babies per woman on average in 2018. This trend has been driven by a combination of short and long-term factors: the age at which women have children has been increasing over time, and the total number of children per family has been falling over time. Enter the pandemic, and things got a whole lot worse. For perspective, the general consensus amongst demographers is that a country’s population can only grow without net inward migration if couples have at least 2.1 children on average. During the pandemic, this figure fell to around 1.54 on average.

There is, however, some good news. With the pandemic having run much of its course, experts now believe global fertility rates may be bottoming and could rise significantly over the long run. According to new research from BCA research, around 75 per cent of the babies that were deferred due to Covid will be recuperated by 2032.

What does this mean?

Fertility rates have a huge impact on the population, and a country’s population has serious long-term economic impacts, particularly as the cohort of taxpayers continuously falls in size compared to the aged population. In Australia, the ratio of working-age people to those over 65 has fallen from 7.3 in 1975 to 4 today.

Based on a fertility rate of 1.6 babies per woman, each generation would be 20 per cent smaller than the last – Stopping or even reversing the trend is good news indeed!

Compare Pears With Pears, Not Apples

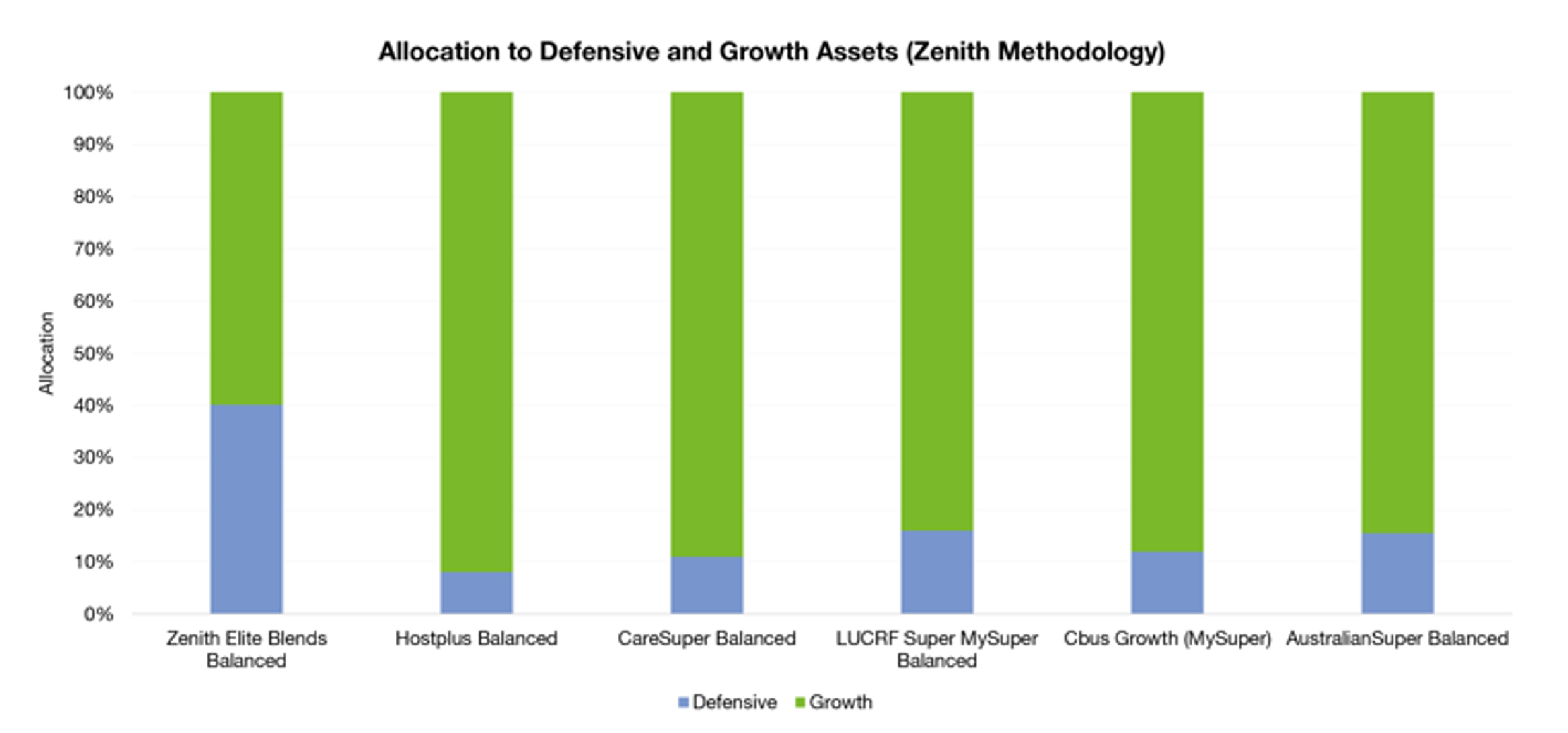

Australia’s Industry Super Funds have been running the highly effective ‘compare the pair’ campaign for many years now. However, Zenith (a leading research consulting firm) argue in a recent paper that “this comparison is not straightforward and is often misleading”.

Zenith’s research focuses on what constitutes a ‘balanced’ super fund portfolio. They argue that most people’s definition of ‘balanced’ is something like a 60/40 mix of Growth and Defensive assets. However, without an industry standard, differences in categorisation lead to portfolios with the same branding (e.g. balanced) having divergent levels of embedded risk.

Generally speaking, Industry super funds often exhibit a lower level of transparency, partly due to their significant exposures to unlisted assets such as commercial property and infrastructure. Given their size, continued strong inflows of SG contributions (compulsory superannuation contributions) and a typically young membership base, they are able to take on the illiquidity risk associated with such assets (this may change if people begin to take out $50K to subsidise their first home…). Whilst there is merit in investing in these types of assets (given appropriate vehicles and time horizons), these assets have a higher level of risk than traditional fixed income. Zenith argues that for typical model portfolios, they would be considered growth assets.

In the chart below, Zenith reclassifies the assets as per the ‘normal’ definition of growth and defensive assets for a subset of industry super funds to demonstrate the deviation from a typical Balanced split of 60% growth/40% defensive assets.

In most cases, industry super funds allocate a much higher exposure to growth assets, and therefore, their absolute performance is not comparable to portfolios with the same risk profile name or volatility (i.e. they are riskier).

Zenith concludes by urging investors to look under the hood and compare pears with pears, not apples! Read the full article here.

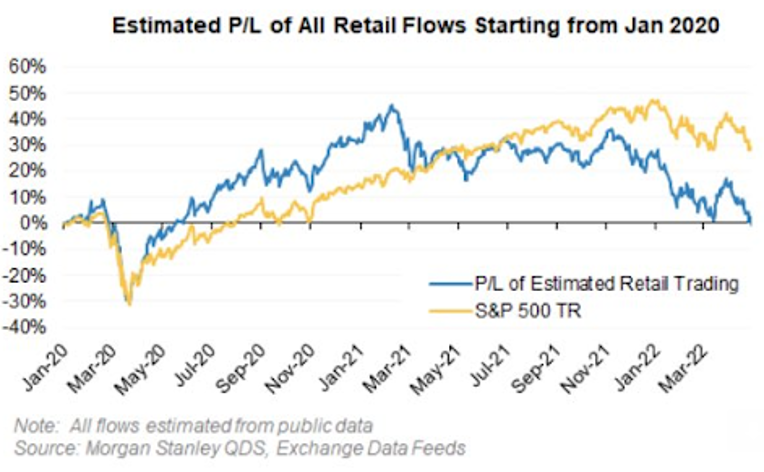

Chart of the Week

Anyone holding a share portfolio with large allocations to tech and small companies knows their investments have taken a hit. Morgan Stanley estimates that the millions of amateur and first-time investors who came into the market (cast your mind back to the day traders of the meme stock era) in pandemic 2020-21 and enjoyed a stellar start are now facing losses greater than their gains.

An ugly reminder that investing is about maintaining perspective and the discipline to not get caught up in the hype. As one of our favourite adages goes, ‘only when the tide goes out do you discover who’s been swimming naked.’

Every three months, the Bureau of Statistics releases the lesser-known cousin of the consumer price index. It’s called the Wage Price Index (WPI), and it records changes in the overall level of wages in the same way the price index records changes in the overall level of consumer prices.

Rarely does it generate headlines, but coming three days before an election and showing the worst performance ever compared with the consumer price index, it has provided strong evidence that the buying power of wages is shrinking.

Contrary to hopes that lower unemployment would spark higher wage growth, the WPI barely budged in the year to March: climbing 2.4%, up from 2.3% in the year to December.

The consumer price index for the year to March grew twice as fast, by 5.1%. It means real wages (the buying power of wages) shrank 2.7% over the year to March in aggregate – one of the fastest and steepest declines on record.

The mechanics of supply and demand would normally mean inflation originates in the labour market, but not so this time around – it is a full-frontal challenge to conventional economics.

There are, of course, a few moving parts at play here. But, primarily, it is worth remembering that measures are off the bottom, so we won’t know the full impact until we have seen a full calendar year’s results.

In the context of zero population growth, questionable participation rates post covid, and no productivity gains since WorkChoices cost John Howard office in 2007, whatever Saturday’s election result is, it won’t be an easy first year for the government to navigate.

Gasoline Humour

Finally, it may be humour through an American lens, but we can all relate!

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.