Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – What investors, retirees, downsizers and SMSFs need to know about the budget

4th November 2022

In a macro sense, last week’s Federal Budget was incredibly modest. Looking at the spending packages as a proportion of GDP they came in at just 0.1%. Really it was just about delivering on the election promises.

In the context of previous budgets, in May 2022 spending initiatives came in at 1.7% of GDP, in 2021 during covid they were 4.1% of GDP and in 2020 5.5% of GDP – Even pre-covid the numbers were far larger.

The reason of course for leaving the number low is to avoid upward pressure on demand which would exasperate the Reserve Bank’s plan to slow down the economy and fight inflation. We saw the example of Liz Truss’s UK budget and a situation where monetary policy works against fiscal policy, not a scenario anyone wants to repeat.

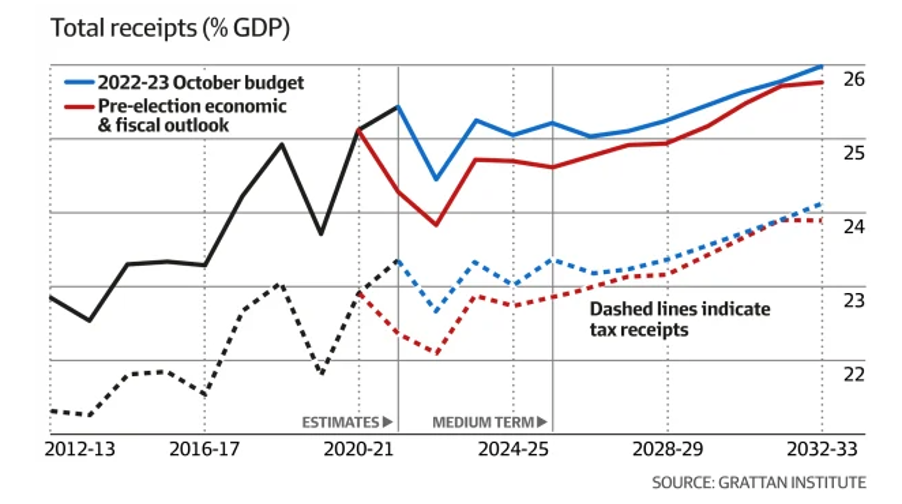

Looking at the budget position there have been some big changes. But, how much of it is due to new policy and what can be contributed to parameter variations (changes in the economic forecast and in any policy decisions unrelated to spending or raising money)? As the below chart depicts, compared with PEFO (the Pre-election Economic and Fiscal Outlook report) revenue was lifted by $158 billion but only $13 billion of this was due to new policies (black) and the rest was due to upgrades in growth eg. high commodity prices (red). Expenses are up by $115 billion and overall the deficit is lower by $42.7 billion relative to PEFO.

Source: Westpac Chief Economist, Bill Evans

Looking ahead.

In this chart, the red line illustrates the October budget where the proportion of gross debt to GDP reaches 47% and doesn’t fall – even after 2032/33. Whereas in the PEFO budget it got down to 40% of GDP. Mmm… Somewhere in the last few months, a 7% hole has been created, not a pretty picture and illustrates the fiscal challenges Australia faces.

Source: Westpac Chief Economist, Bill Evans

As the problem wasn’t addressed in this budget we have to expect that the next budget will be tough. May 2023 will be two years out from the next election and really the government’s only chance to try and fix the problem – May 2024 will be too late (we’ll be in election mode) and 2025 could either be just before or just after the election.

Budget 2023 will represent the challenge this government has to try and deal with the rapidly deteriorating fiscal position of the economy.

In this issue of the View, we look at the broader announcements through a financial advice lens and how from a planning perspective, it might affect you.

Budget Report – What changed for super and retirement planning

While the budget confirmed some changes already in play, there was not much new on superannuation and retirement front. As one FinSec adviser touted, “I don’t recall a Federal Budget with less to say about superannuation in my career of over 20 years.”

Of particular relevance, the announcements included:

- Decreasing the eligibility age for downsizer contributions from age 60 to 55;

- Deferring residency tests for SMSFs;

- Increasing the exclusion time that proceeds from a house sale are excluded from the assets and income tests for the age pension; and

- Increasing access to the Commonwealth Seniors Health Card by raising cut-off-income limits.

Beyond this, it was more about what was not announced. Perhaps of most importance is that while there were some announcements about prior Budget measures that the Government is either deferring or not proceeding with, there was no update regarding the 2021/22 Budget announcement for the unwinding of legacy pensions in superannuation.

The loud silence on this issue suggests perhaps that it is simply not on the Government’s radar. It is a change that we consider long overdue, creates no great revenue leakage for the Government and recognises that the tax and regulatory environment has moved on enormously since people put these in place (they haven’t been an option as a brand-new pension since 2007). Let’s hope it is an oversight and rectified next May when the next traditional Budget is scheduled to be delivered.

Further, as anticipated and effectively confirmed by the Government, there were no announcements about:

- winding back the Stage 3 tax cuts due to take effect in July 2024;

- limiting the amount that could be accumulated in super; or

- changing indexation of contribution or other superannuation thresholds.

A list of measures affecting superannuation, social security and aged care can be found here.

The Budget and Markets

This budget reverses the pro-growth agenda that was set out by the former Government in May 2022 and instead, adopts more conservative fiscal policies given the elevated inflationary backdrop and the need to move in the same direction as the RBA.

Traditionally, budgets don’t have a major or prolonged impact on the equity market, and it is doubtful that we’ll see the current combination of policies as anything different. Few households or businesses are likely to feel worse off, but simultaneously, a few will hopefully feel better off as any cost-of-living adjustments are appreciated.

We doubt the budget will lift sentiment or confidence a great deal, and in turn, it is unlikely to drive households or businesses to raise investment, employment or consumption to any large degree. It would seem the intention of this budget is to support areas of weakness – particularly around social security – rather than provide a strong lift in aggregate demand. Similarly, we think consumers are more likely to hold on to any gains given the ongoing uncertainty around the growth and inflation outlook.

A view of how this will play out in the market is discussed below (source investment strategy team at Macquarie).

For the bond market, the budget provides some confidence that the Government will not fritter away the gains from high commodity prices even during a time when growth is weak. This reduces inflationary pressures from expansionary fiscal policies, helping keep bond yields relatively suppressed and more at the whim of global developments. We think the same can be said for the A$, which is being driven lower by a relatively more muted inflation and interest rate outlook in Australia compared with the US.

For the equity market, outside of a boost to earnings, we see no reason to think that this budget will have any material impact on the risk premium and/or valuations. This would imply that the forces which have been driving the market throughout the past six months (rising bond yields and slowing earnings growth) will remain intact without much of an offset by fiscal policy.

We believe the initiatives aimed at improving access to affordable housing can serve as a tailwind for the building and construction-linked sector. That’s as long as it can get traction… (see our article on the National Housing Accord below).

On a similar note, the consumer spending outlook remains solid heading into the first Christmas period in 3 years where there have been no lockdown restrictions, and this should see a strong spending environment, even if only temporary.

The most important drivers of Australia’s financial markets will continue to be the interplay between the following elements:

- Inflation: If prices remain elevated, financial markets will continue to be volatile until there is greater transparency on how services inflation is picking up and when peak rates will be seen.

- Monetary Policy: We believe monetary policy, domestically and abroad, is the most important factor for driving financial market movements. At this stage, and even though the RBA has slowed its pace of rate hikes, further increases are still to come.

- Global growth momentum: As the outlook for global growth continues to deteriorate, financial markets will continue to be vulnerable to this weakness, particularly as bottom-up earnings expectations remain elevated versus what would be expected during a period of slowing economic growth.

We remain cautious on the Australian equity market and see little chance that it will break with the direction of global markets. This budget is neither positive nor negative for the market, barring housing-linked stocks, and we think its impact will not be long-lasting as investors settle back and refocus on the same drivers that have been impacting markets since the start of the year.

Australian equity earnings depend on the global economy.

Source: FactSet, MWM Research, October 2022

Charts of the Week

Great work from the AFR with these ‘five budget charts’.

1. Tax Receipts are up

As mentioned in opening comments, soaring commodity prices and a booming jobs market have delivered the Government billions in extra revenue, a boost that even the Treasury says will be hard to repeat.

A crackdown on tax avoidance, higher levies on off-market share buy-backs and a one-off increase in skilled migration are among the new measures the Albanese government expects will net $9.4 billion over the next four years.

2. Higher NDIS, interest cost

Treasury expects the NDIS to cost $97 billion by June 2033 and eclipse the age pension as the Government’s most expensive federal government social program (a scary thought indeed…). Interestingly, the papers seem to be silent on the cost of medicare which we understand is forecasted to be around $90 billion this year.

In addition, annual interest payments are tipped to hit $70.5 billion in the next decade, about $30.5 billion higher than forecast just seven months ago.

3. Cost of living pressures

Electricity and gas costs are expected to increase as rising energy costs are passed onto households. The budget forecasts prices will increase by 20 per cent in the second half of 2022 and a further 30 per cent in 2023-24 (eek…get used to turning those lights off people!).

This increase is expected to add 0.75 percentage points to inflation this financial year, with overall inflation forecast to peak at 7.75 per cent in this quarter.

4. Wage growth remains modest

The budget also forecasts wages will grow at the fastest pace in more than a decade over the next year, rising almost 4 per cent. Despite this optimistic forecast, workers will still be worse off as inflation will still outpace wage growth and no doubt many businesses will be forced to pass the cost on.

5. Structural deficit to persist

Structural deficit is forecast to remain at about $50 billion over the decade. This works out to about 2 per cent of gross domestic product – not an insurmountable problem but again as discussed in our opening comments shows that the Government will have to eventually make some very tough decisions on spending, tax and economic reform.

Crypto got a mention – An asset for CGT, not a currency

One of the announcements to jump out at us from the monotony of budget night was that bitcoin got a mention, with Treasury feeling the need to clarify that authorities consider it an asset for capital gains tax purposes and not a foreign currency. Yes, crypto gains are officially in the tax law.

Investors will pay capital gains tax when they sell crypto assets through an exchange (if they have made a profit) as well as when they trade digital assets for each other. The usual capital gains tax discount will also apply. Investors must also own the asset for a full year to avoid income tax.

Given what has happened with Crypto this year, it’s unlikely this will be a big problem anytime soon!

National Housing Accord – A mammoth task

While not directly a superannuation initiative, the government has also announced a National Housing Accord aimed at bringing together various stakeholders to increase the housing supply. The challenge ahead is an interesting one.

In the budget papers, they talk about building one million new houses over the course of four years. The $700 million pledged by the government is for 20,000 new homes, and the financing for the other 980,000 is going to have to come from the private sector.

In thinking about this measure we reflect on the number of new dwellings currently approved yearly – around 180,000. So, this measure suggests we build more than double that figure.

Demand will need to be boosted, and we will need a huge lift in investment. The heavy lifting here, of course, is on the shoulders of the managed fund sector (and must be done in a way that meets both the sole purpose test and an obligation to invest for the best financial interest of members).

On the supply side, state governments will need to come to the party (they have agreed in theory), not to mention the resources; timber, steel, glass, cement and, of course, the workers to make it happen.

It is hard to see that all the stars will align in getting near the one million mark. But, rather than focusing on the number, we should focus on any progress we can make! It is fantastic to see a government giving it a go and recognising the fact that you need to think big in order to deal with the housing affordability crisis we have (this includes two years of migration catch-up as we aim to fill the gaps in our workforce.. who will need somewhere to live).

The next step in the discussions will be the Treasurer’s Investor Roundtable on November 25, which will include representatives from all stakeholders.

Pic of the Week

There were a few brave soles out and about on Monday night, but nothing compared to the normal tribe of trick-or-treaters on Halloween night. At first, we attributed the low numbers to the absolutely freezing conditions, but on reflection perhaps it was this costume sale!

For the curious, a great article by National Geographic on the history of trick-or-treating can be found here.

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.