Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – A quandary, 8 billion people, housekeeping matters, Non-Fungible Trump and More

10th February 2023

Welcome to the first issue of the View for 2023. After a January sabbatical (editorially speaking), it is good to be back, and we trust all our readers had an enjoyable holiday break. This year, more than usual, it feels like a time to stocktake and check one’s goals for the year ahead. Nobody hands out a card that profiles the future, and everybody needs to plan their own 2023 objectives, including financial and investment goals based on their life, their resources, their desires, and these objectives.

Although every financial newsletter shares the tea leaf reading of market experts at the start of the year, here’s how legendary investor Warren Buffet colourfully describes these efforts:

“A prediction about the direction of the stock market tells you nothing about where stocks are headed, but a whole lot about the person doing the predicting.”

In determining where the market is going… we expect volatility, so up, down and flat pretty much covers it! For completeness, here is what the “experts” are predicting for 2023 (to our point, a mixed bag indeed…):

- Goldman’s: Global growth 1.8%. Issues with China reopening and the European recession

- Morgan Stanley: Global weakness in economies but markets “ok”. Housing to recover via supply shortages

- BlackRock: Down markets and increased volatility. Sticky high inflation

- Deutsche: Opposite to Blackrock. Inflation tamed and markets up.

- HSBC: Good 2023 for Bonds (yields falling), slight fall in equities. Strong real estate.

As we read recently in publication, Incognito;

“A bit like the reason that the NRL and AFL have not had any player/coaches for years, I reckon it is sometimes better to get the drone in the air for a distant view of the markets rather than be knee deep in trying to eek a living out of it.”

So, are we bullish or bearish?

The short answer remains – BOTH! More on this below.

***

June 30 will be here in the blink of an eye, so in the spirit of planning, next issue, we begin our ‘lead-up’. Watch this space for important information on making personal deductible super contributions, the new $1.9m transfer balance cap, insurance as a tax strategy and more.

Economic Update

January was a good month for equity markets, more than regaining the ground lost in December. Bond markets also did well, more than recovering their December declines, with bond yields falling back in January after rising in December.

Therein lies the quandary. Rising share markets point to good times ahead, but declining bond yields point to rate cuts and a likely recession (US and Europe).

From early October, the market started to see US inflation easing and sensed the Fed would soon ‘pivot’ towards less aggressive rate hikes – After a string of hikes of +0.75% each time, the Fed did slow its hiking to +0.5% on 15 December, and +0.25% on 1 February. The European Central Bank and Bank of England also made further hikes at the start of February. This hoped-for ‘pivot’ has lifted investor confidence and therefore share prices since October last year.

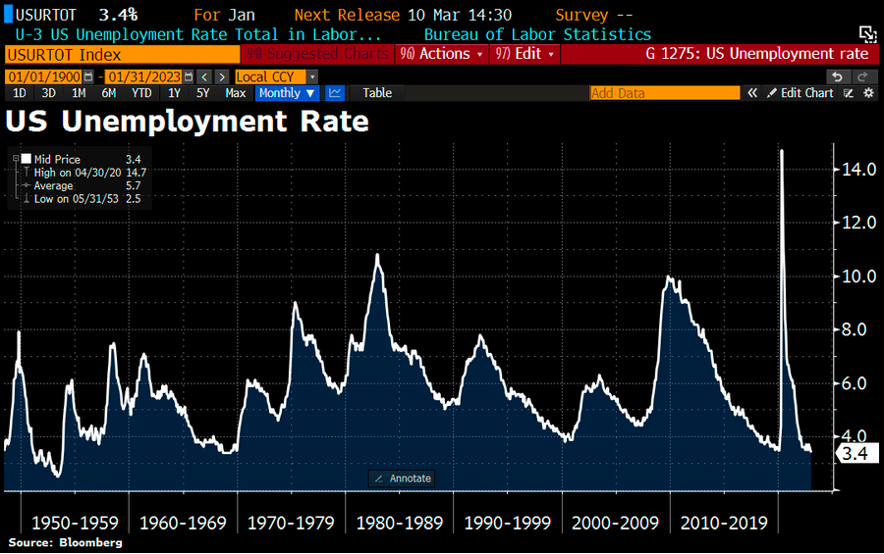

The other main factor is unemployment. Thus far, job markets have remained very strong due to border closures and strong spending.

US unemployment data released last week was very strong – the lowest unemployment since the 1950s.

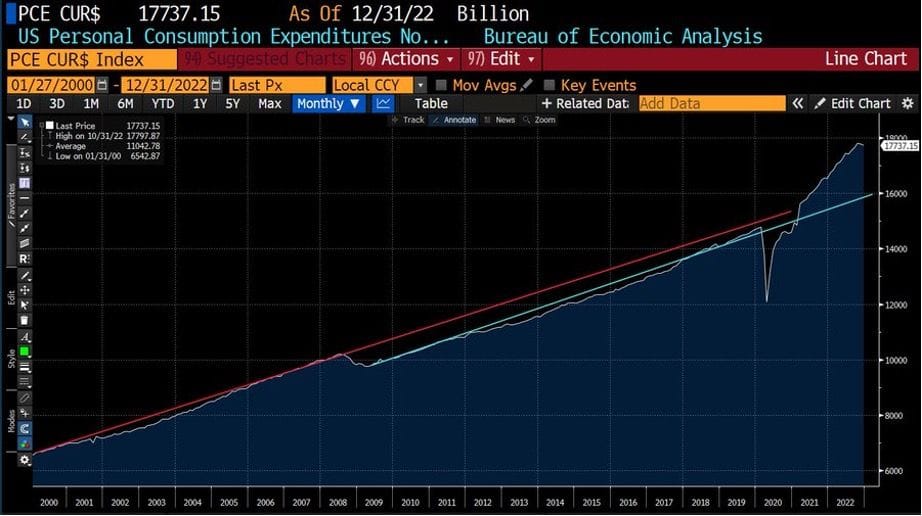

US spending is well above pre-Covid levels.

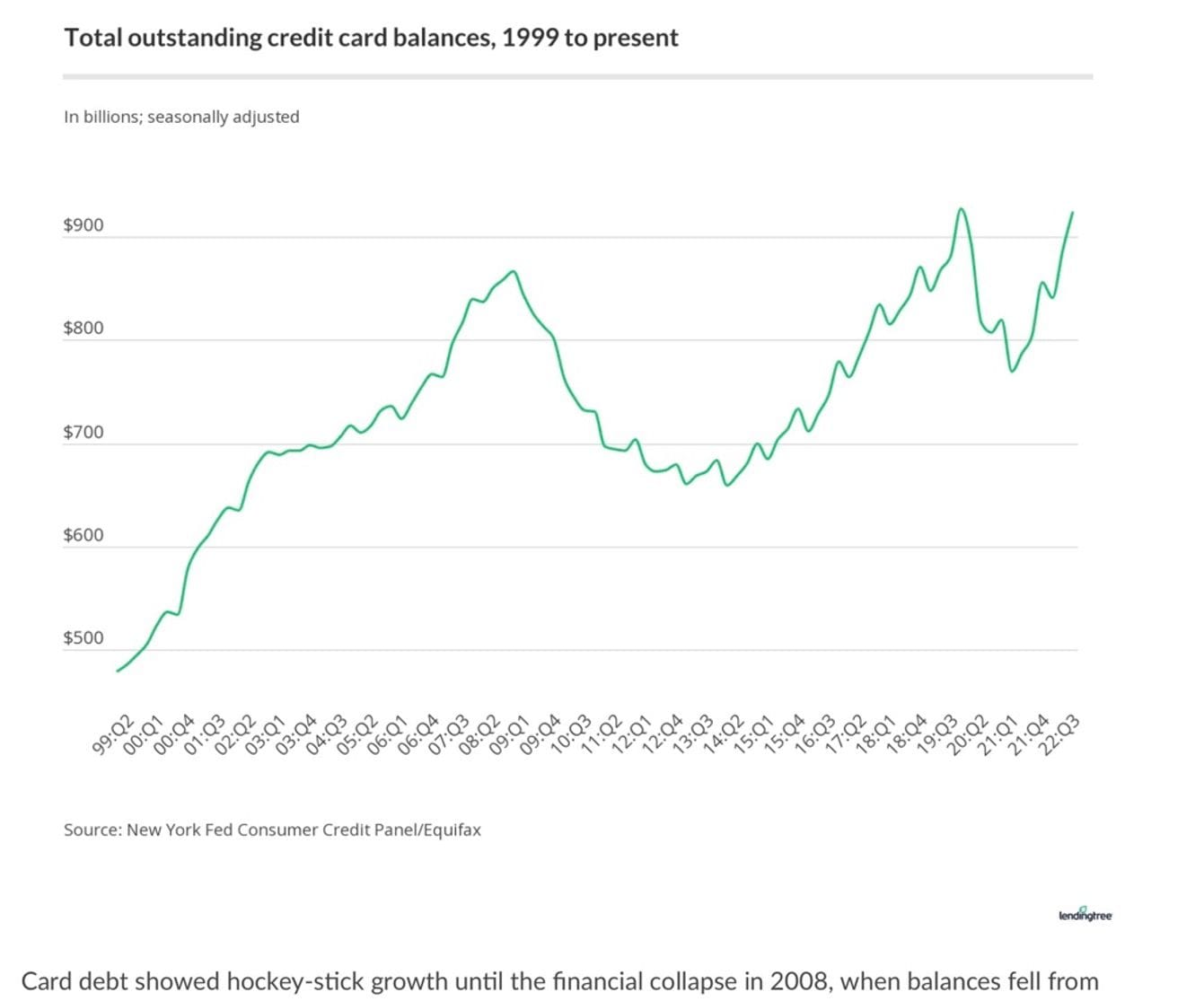

Albeit, as the chart below shows, those spending figures seem to be propped up by personal credit card debt.

Unfortunately, the very resilience that gives the equity market hope (good employment, spending holding up) may just be the architect of misadventure. The central banks need to crush inflation, slow spending and for employment to be weaker. If it refuses to oblige, then they may be forced to hike higher for longer.

This combination of rising share prices and falling bond yields represents ‘bookend’ scenarios. At one end, markets are assuming inflation will fall back to target without recessions, which would allow central banks to start cutting rates later this year. This is the ‘goldilocks’ soft landing scenario. Bond yields, on the other hand, are implying something a little harder. A not-so-soft landing in which inflation comes down to target because of serious economic slowdowns and thus forcing central banks to cut rates to stimulate jobs and spending.

We remain cautiously optimistic and believe we will see something in between – Whilst it’s hard to see inflation magically falling below target and staying there of its own accord, there is still plenty to be positive about (more on this below).

On home ground

In Australia, the cash rate is still well below ‘neutral’, and inflation is not coming down as quickly as it is in the US, so we may see a few more rate hikes from the RBA. One major difference between Australia and the rest of the world is that most home loans are floating (variable rates), which are more directly impacted by rising interest rates. We are yet to see the full impact of recent rises on mortgage repayments and household spending. We also have more than half a million fixed-rate loans converting to much higher floating rates over the coming year. This will more than double their repayments, cut into discretionary household spending and contribute to mortgage stress. A further factor is the looming construction slowdown with lower house prices.

Plenty of room for optimism in 2023

Inflation, interest rates and servicing of debt will continue to be major themes of 2023; however, there are many positives.

Markets have already sold off in 2022, removing much, or even most of, the boom time overpricing. The tech sector is still considered expensive, but other sectors are more reasonable, having already priced in weaker profits and dividends in 2023.

Bond markets saw their worst year in 2022. Bond yields have now risen most of the way back up to average or neutral levels. All central banks except Japan have now ended quantitative easing ‘QE’ (the buying of bonds to reduce interest rates, increase money supply and suppress yields) and have now started quantitative tightening ‘QT’ (where central banks reduce their bond holdings by selling them or letting them mature). QT will most likely continue for some time into the future, limiting any negative impacts on bond prices.

Cash is now paying a return again!

Commercial and residential property markets will be affected by rising interest rates and falling asset prices. However, mortgage stress and foreclosures will most likely be limited to highly geared pockets of the market. Remember also that banks are much better capitalised than they once were and more de-risked since the GFC.

Australian commodities are seeing a rise in demand – China’s reopening, increased infrastructure, defence spending and demand for renewables.

Covid and the Russian invasion of Ukraine have accelerated several global shifts, including; on-shoring (or near-shoring) of manufacturing, self-sufficiency of critical supplies, new economic alliances, the strengthening of NATO and not to mention the flow-on that will occur from India overtaking China as the most populous country and potential driver of global growth.

Great companies will always find ways to prosper from changes like these in both local and global markets, and great fund managers will seek out and find these great companies!

8 Billion

We made a comment above re/India’s takeover of China; this is one of the best charts we’ve seen in recent weeks acknowledging both this major milestone and that of the global population passing 8 billion. For perspective, Australia is represented by that tiny purple triangle on the left. No wonder we Aussies love to think we punch above our weight! (Click the image to enlarge).

For Context

An interesting video from Darko Kuzmanovic, Janus Henderson’s global natural resources portfolio manager, in which he talks about the ‘new’ commodity super-cycle.

Far from simply being a China story this time around, it’s now a global theme that is driven by demand, and also regulations as countries around the world implement clean-energy targets into 2050 and beyond.

Chart(s) of the week

A bit scattergun, but we wanted to cover a few interesting charts we’ve seen of late.

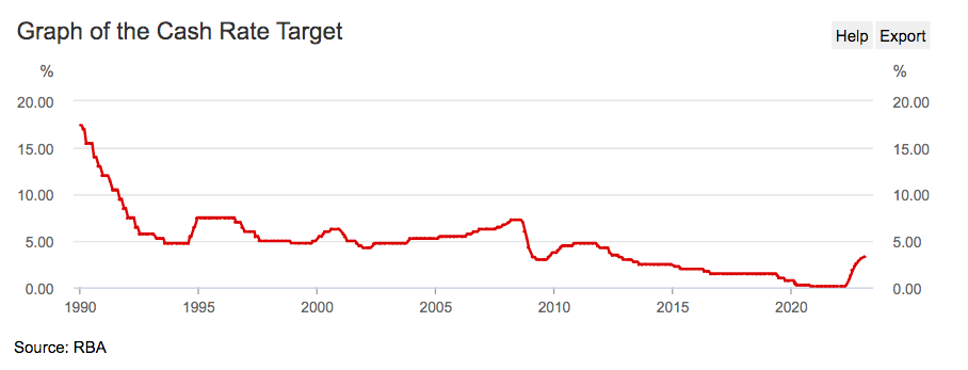

Straight from the RBA website itself, this chart brings a little perspective to the cash rate.

The media is in a frenzy about ‘crippling’ interest rates, but this chart demonstrates that we’re still at the low end of normal.

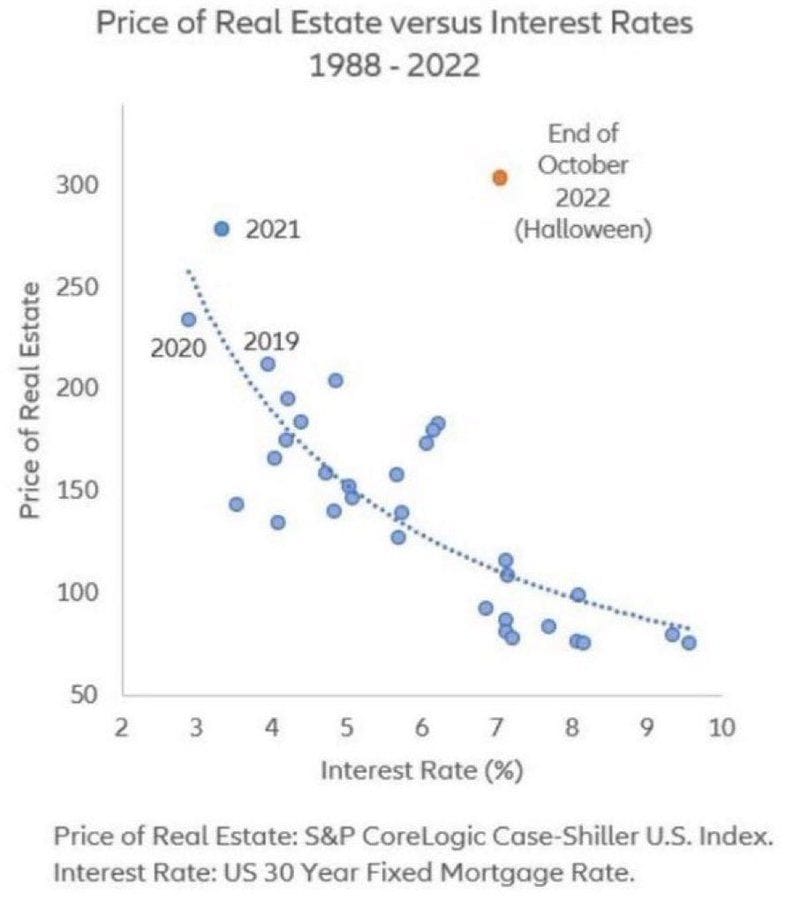

Housing demand (amongst other things) is a function of cost, of which interest rates are meant to be a major determinant. Currently, it would seem the US is out of whack (and by quite a lot). It shows interest rate rises are yet to really bite!

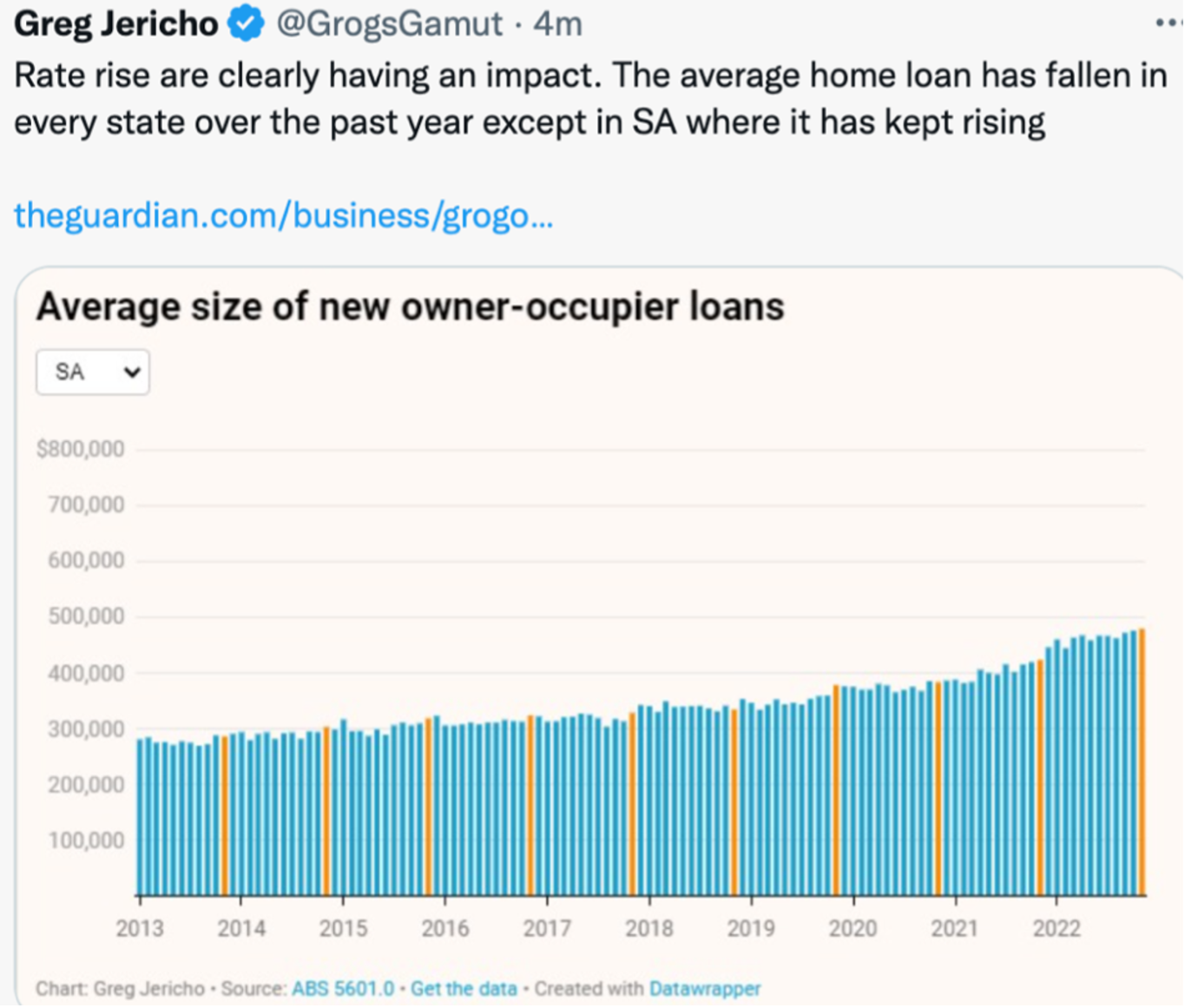

Australian house prices are falling (but still much higher than pre-Covid), and the last bastions holding out against the fall were Adelaide and Darwin. Even they are now adjusting, albeit more slowly than the eastern seaboard. SA loan sizes are still moving higher, which is against the grain too. We can only assume that gearing levels and outright housing prices make the difference. As the majority of our readers are in SA, we thought this chart would be of interest.

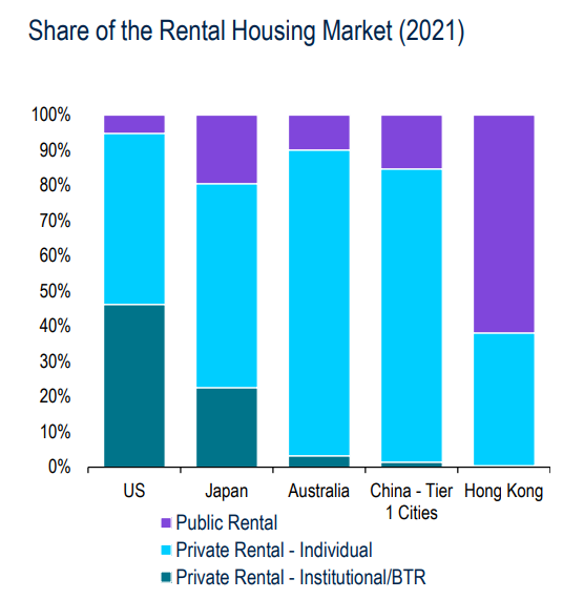

Onto the rental market, and sticking with structural differences, you can see below just how different our housing rental market is compared to overseas. We leave the bulk of the heavy lifting to be done by private investors, whilst others either give the big institutional players a big slice of the pie or have government social housing as a priority.

* BTR stands for ‘Build to rent’ and refers to purpose-built housing designed for rent rather than sale. It is an initiative we’ve heard much about from Federal Treasurer Jim Chalmers. He is keen for super funds to get involved in a bid to direct more money into affordable housing. You can read more in our previous article ‘Labor’s Super Plan to Move Beyond Superannuation Wars’ here.

Housekeeping matters

Encrypting documents with passwords

A quick piece of housekeeping for our clients.

As most would be aware, when we send you a document containing ‘sensitive’ information (e.g. financial information), it is encrypted with a password. Currently, this password is provided via a secondary and separate email.

We wish to advise that moving forward; these passwords will now be provided via sms message to your mobile phone.

With scams and hackers becoming increasingly sophisticated, it is imperative that we try and stay one step ahead in our efforts to protect your information. After all, if someone has hacked your email, then sending a password via the same method becomes somewhat defunct.

For those who do not have a mobile phone, we will provide passwords in person via your landline.

Should you have any questions regarding this new initiative, please do not hesitate to contact our client services team on 08 8357 7840.

BCD Scholarship – Applications now open

We are proud to announce that applications for the FinSec’s Behind Closed Doors (BCD)’ SA Emerging Leader Scholarship are now open!

This scholarship will enable an emerging South Australian female leader in the Not-For-Profit/For Purpose sector to join the national BCD community.

The scholarship includes the following:

- $1,500 towards a BCD membership

- Up to eight three-hour peer coaching and mentoring sessions

- Six one2one coaching sessions with a carefully matched Coach/Mentor

The applicant must:

- Identify as Female

- Work in a non-executive role in the For Purpose/Not-For-Profit sector

To nominate a potential applicant, please email

If this is you, or if you know of someone you would like to nominate please apply directly via email to heather.price@finsecpartners.com.au with your CV, and a cover email on what winning the Scholarship would mean to you and your organisation.

Applications close on Friday 24th February, 2023.

Before my husband’s death, I thought we had our affairs in order. I was wrong — here’s what you should expect

A nightmare of administration is the unfortunate bureaucracy that awaits many people when their spouse passes away. This article from the ABC is worth reading regardless of your life stage and contains some simple but sage advice for anyone looking to get their affairs in order.

- Obtain certified copies of original certificates, birth and marriage;

- Have ready certified copies of identity documents, passport, driver’s licence etc. (even if you no longer drive or travel, keep them updated);

- Ensure you know where the latest will is, get a certified copy, and have the superannuation fund details ready;

- Make sure there is enough money available to tide a widow/widower over for at least several months after death;

- Have a trusted adviser to help you plan for the worse and navigate the minefield of administration after the event.

Quote of the week

It’s our second Buffet quote for this issue, but we think it’s timely.

“The stock market is a device to transfer money from the impatient to the patient.”

~ WARREN BUFFETT

Non-Fungible Trump

When the Trump NFT came out, we were certain it was a joke, but sadly no. Sold out. “Major announcement” indeed!

And finally… Just for fun

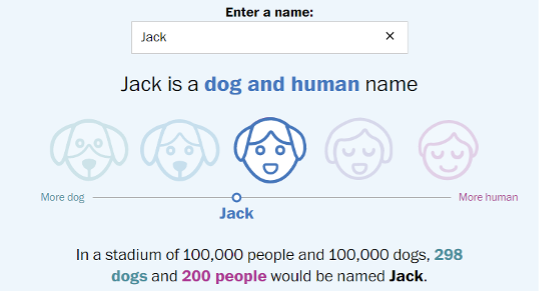

How common are dogs with human names? Or humans with dog names? Glad you asked. The Washington Post explored the names of 61,000 dogs available for adoption on the Petfinder website and compared them with baby names stretching back to 1880. If your name is Emily, you’re almost certainly human. Rover? 100% dog. Jack? See below.

Now we know what you’re thinking. You really wish you could test out your name and see the results. As always, we’re here to help. You can do it here.

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.