Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Australia’s Honey Pot, NCC Trap, Retiree Reflections, 2022 Value of an Adviser Report and More

24th February 2023

Any hope that superannuation regulations will remain unchanged again in the next Federal Budget on 9 May 2023 is fading fast. Super was untouched in 2022, but the Financial Services Minister, Stephen Jones, has done enough jawboning to indicate he is ready to strike. And, with Prime Minister Anthony Albanese (National Press Club) making the below comment yesterday, it seems the super wars could be back on.

“We said that we would not have any major changes in superannuation, and that is certainly our intention. But we’ll receive the review and the report into superannuation, we think that it is important that this continue, and that we do have a debate about the purposing of superannuation.”

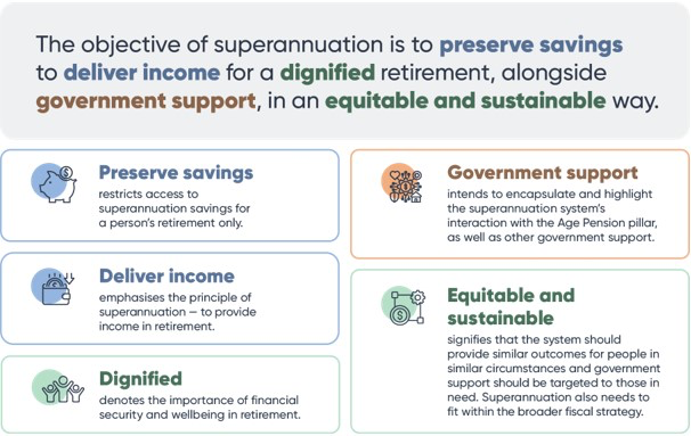

There was a lot of angst this week about the objective of superannuation, but it’s not the definition that will really matter. It’s the legislated rules that follow. The Prime Minister and Treasurer will claim that capping superannuation is not a ‘major change’ as it affects relatively few people.

Jim Chalmers told Radio 2GB that he was not looking at a higher tax rate on contributions or income but hinted at a limit on super of $3 million.

“If you think about the average balance in super is about 150 grand, I think, but for less than 1% of people in the system, they’ve got balances higher than $3 million. The average among that group is $5.8 million.”

Whether or not it is a ‘major change’ remains subjective. It may not affect the majority, but it will involve many people, particularly those with illiquid assets in their SMSFs, who will be forced into asset sales and a substantial reorganisation of their retirement planning. How the government will actually manage the limit remains to be seen. Balances fluctuate daily. Let’s hope they consult widely to ensure the solution isn’t harder to manage than the problem.

While the Government wants to believe that, to quote Jim Chalmers, “an objective will end the super wars once and for all“, we can’t help but think the subjectivity of the objective itself (Dignified. Equitable. Sustainable. Security. all mean different things to different people) and confirms that the years of arguments about superannuation are most likely not about to cease.

Market Update

It has been a big fortnight for economic data and a mixed bag for markets.

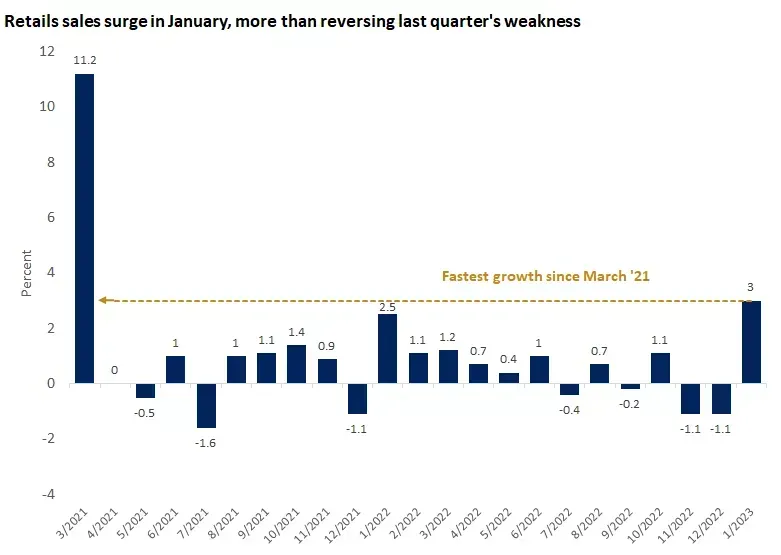

2023 is off to a strong start for consumer spending

The highlight last week was the release of U.S. retail sales, which soared the most in almost two years. Sales for January rose 3% from the prior month, well ahead of expectations for a 2% increase and more than offsetting December’s decline. This strength in spending is underpinned by a tight labour market with historically low unemployment and solid wage gains.

This backdrop is hardly what one would expect from an economy that is still navigating inflationary pressures and the most aggressive Fed tightening cycle in four decades. Which begs the question: Does the Fed need to do more? The bond market appears to think so, but equities have remained largely unfazed.

Consumer spending represents approximately 70% of U.S. GDP, and therefore the economy follows the consumer. With consumption accelerating and the labour market remaining exceptionally strong, some market experts have now added a third scenario to the soft landing vs hard landing debate. In the so-called “no landing” scenario, one in which the economy powers through the Fed’s rate hikes without slowing down. While a resilient economy is always the most desired outcome when inflation is subdued, in the current environment, it would likely invite more aggressive Fed action and risk an economic crunch.

Disinflation continues, but the pace slows

January’s inflation data (U.S.) also released last week, offered mixed takeaways and contributed to the uptick in market volatility. The consumer price index (CPI) continued its path lower, but the pace was slower than expected. Headline inflation eased slightly from 6.5% year-over-year in December to 6.4% in January, and core CPI moved from 5.7% to 5.6% – Higher than consensus estimates but still the lowest reading for headline inflation since October 2021, and the seventh straight month of improvement from its peak in June.

The measure that the Fed has highlighted recently and is paying close attention to is core services inflation excluding shelter, which is largely a function of the labour market. This ticked lower, both on a monthly and an annual basis. This modest progress is welcome but is likely not enough to keep the Fed from continuing to raise rates at the coming meetings.

Bottom line

January’s unexpected consumer strength, exceptionally tight labour market and persistent inflation challenge the Fed to keep interest rates higher for longer. If policymakers are sensitive to avoiding a repeat of the 1970s mistake when the Fed prematurely declared inflation over, they may even be inclined to take a harder line.

The upshot is that a resilient economy adds upside risk to the Fed’s tightening path. However, there is another unemployment report and another inflation reading before the Fed’s March meeting, which could again change this narrative.

Chart of the Week

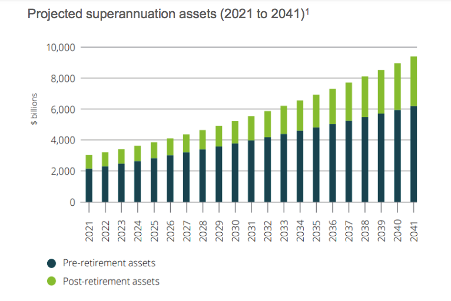

It’s little wonder that everyone is looking to cash in on the “honey pot”, a term that assistant Treasurer Stephen Jones has used to describe Australia’s superannuation pot (convention for the self-managed-super fund industry, 23 February 2023).

According to Generation Life, the balance is projected to reach a whopping $8 trillion-plus by 2040 and makes for our chart of the week.

Such is the scale of the number that most people struggle to comprehend it. For perspective (using the context of time), there are 3 600 seconds in an hour, 86 400 seconds in a day, 31.5 million seconds in a year, one billion seconds in 32 years, and one trillion seconds in 32 000 years.

NCC Trap

Making a personal deductible superannuation contribution should not be difficult. Unfortunately, many are discovering that this may not be the case.

It’s important to understand the process

Personal contributions are non-concessional contributions and count towards your contributions cap unless you claim a tax deduction for them – ie, lodge a notice of intent (NOI) to claim a deduction with your fund, have it acknowledged and claim the same on your tax return.

The ATO makes its assessment using information from your super fund(s) and tax return, and sometimes it’s too quick in issuing excess contribution determinations – like where you’ve lodged your tax return, but the ATO hasn’t yet processed it.

Without your tax return being processed, contributions are treated as a non-concessional contribution. If you exceed your non-concessional contribution cap, the ATO issues an excess determination explaining your options, and you have 60 days to decide.

Option one allows you to withdraw the excess contributions and 85 per cent of “associated earnings”. The earnings are then taxed at your marginal rate plus Medicare levy less a 15 per cent tax offset for tax already paid.

Option two is to leave the contributions and earnings in super, but the excess will be taxed at 47 per cent. As non-concessional contributions are from after-tax money, you’re effectively paying double tax. This option must be selected if your only super is in a defined benefit fund.

Do nothing, and the ATO automatically defaults you to option one.

There is plenty of upside to the benefits of tax-deductible super contributions but it can be a confusing and complex area to navigate – our advice is always to discuss with your adviser first. MyGov does provide ‘checks and balances’ but only if your tax return is up to date.

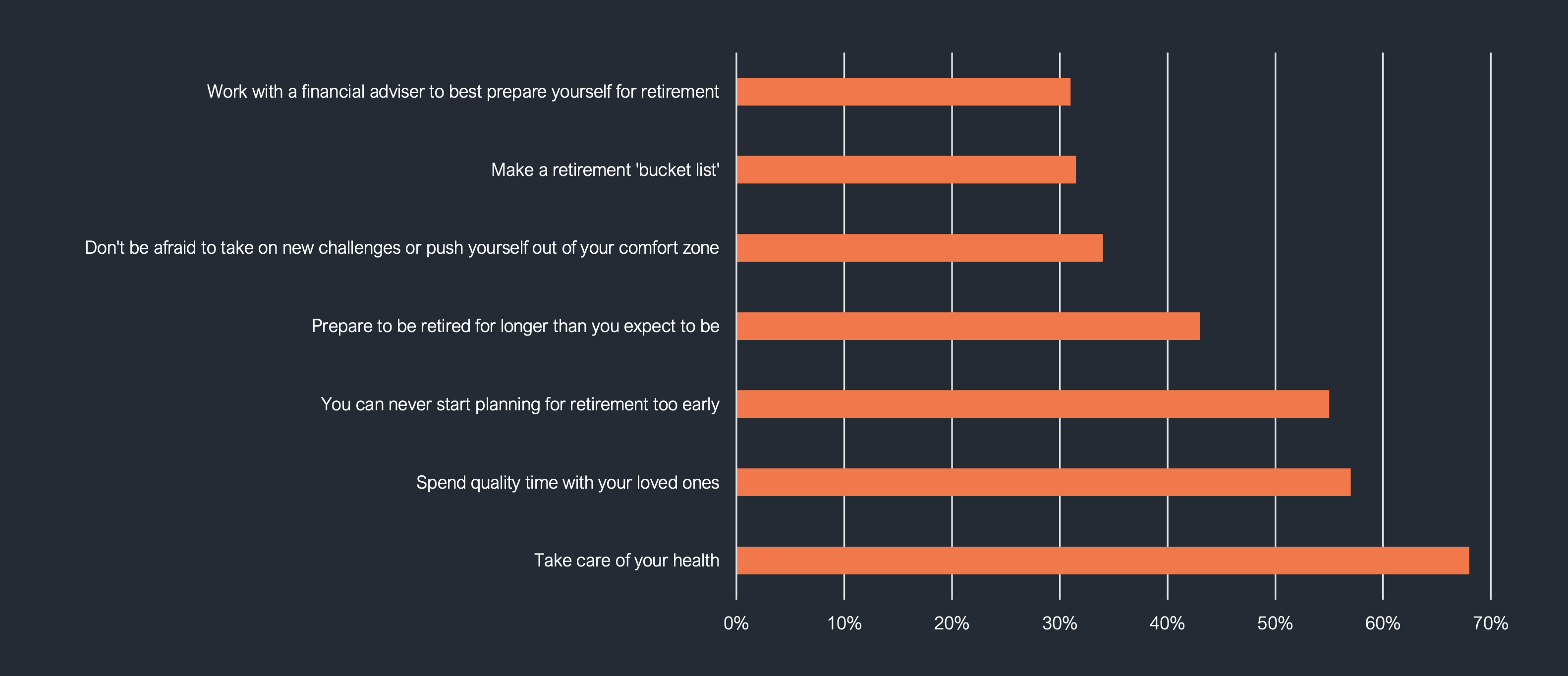

Retiree Wisdom

Always a favourite with our readers – nuggets of wisdom from those in retirement for those planning for it.

In a survey for Netwealth, two thousand 75+ year-olds shared this simple advice for making the most of your golden years (click to enlarge).

BCD Scholarship – A Reflection

As we’ve mentioned in previous missives, FinSec is a proud sponsor of Behind Closed Doors (BCD) and their emerging leaders’ scholarship. As such, it was with delight that we received this note from 2022 recipient Maryke van Diermen earlier this week.

With Maryke’s permission, we thought it fitting to share her reflections with our community.

As a recipient of the emerging leaders BCD scholarship, I have gained a wealth of knowledge, skills, and experiences that will serve me well throughout my career. Through the various workshops, seminars, and training sessions provided by BCD, I have honed my leadership, communication, and professional skills. In particular, my skills in strategic planning and those needed for ‘difficult conversations’.

I have had the opportunity to network with other accomplished women and have built many valued relationships. Furthermore, the scholarship has provided me with access to invaluable mentorship and coaching opportunities. All of these experiences and opportunities have contributed to my personal and professional growth and set me on a path towards success.

The scholarship helps to build confidence and provides the tools and resources needed for successful leadership.

For those considering applying or joining BCD, here are a few tips to keep in mind:

- Prepare a strong application that highlights your achievements and goals.

- Embrace the nerves and fear, be open and vulnerable in the sessions.

- Take advantage of networking opportunities and make connections with other women.

- Be open to learning and be willing to invest time and effort into your professional development.

- Utilise the resources and support provided by the scholarship program to help you achieve your goals.

Thank you for this opportunity, it will be an experience I will always value.

Maryke van Diermen, KWY Aboriginal Corporation

Applications for this year’s scholarship close soon.

To apply, please email heather.price@finsecpartners.com.au with your CV, and a cover email on what winning the scholarship would mean to you and your organisation.

More information can be found here.

Naracoorte (Next Visit) & Grain Seminars

A quick reminder for our regional clients.

Naracoorte – Next Onsite

Our next Naracoorte visit is scheduled for Wednesday 22nd and Thursday 23rd of March. If you would like to book an appointment, please call the office or email heather.price@finsecpartners.com.au. Alternatively, you can book online by clicking here.

Grain seminars

Managing Partner Andrew Creaser is again off to the ‘Penninsulas’ to deliver wealth advice to our regional grain growers. This year’s presentations (from a team of speakers) will focus on an integrated framework for turning the functions of tax, banking, superannuation, succession planning and wealth management into strategic business assets.

Dates: 7th, 8th and 9th March (Cleve, Cummins, Coonalpyn, Jamestown and Wallaroo). Your spot can be booked here. More information can be found here.

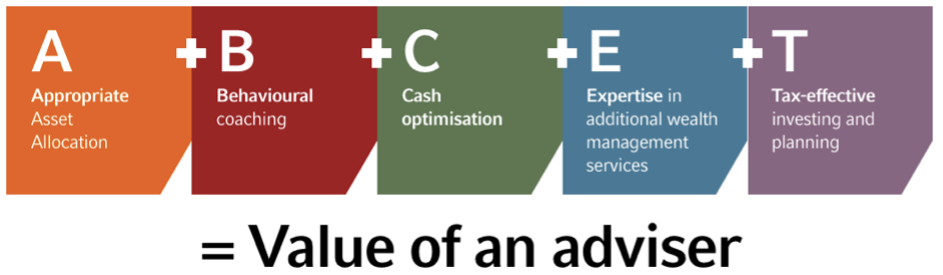

2022 ‘Value of an Adviser’ Report

According to the 2022 ASX Investor Study, just 30 per cent of investors received advice from a financial planner or wealth manager in the 12 months to June.

The other 70 per cent may want to take a look at the latest findings from investment house Russell Investments demonstrating the value good advice can add to personal wealth.

The fund manager’s number crunchers have estimated in their latest report (2022) that financial advisers can add at least 5.8 per cent per annum in monetary value to their clients even (or perhaps especially) in challenging investing climates.

How is this number quantified, you may ask? According to Russell, the ‘value of an adviser’ formula is calculated using five key components.

- APPROPRIATE ASSET ALLOCATION & ACTIVE RE-BALANCING OF YOUR PORTFOLIO

= 1.6% P.A. - BEHAVIOURAL COACHING

= 2.9% P.A. - CASH OPTIMISATION

= VARIABLE (based on your life stage and needs) - EXPERTISE

= PRICELESS - TAX-EFFECTIVE INVESTING & PLANNING

= 1.3% P.A.

Access to professional advice in Australia may not be an option for everyone; however, we can only hope this analysis goes part way to bridging that gap.

This Month in History

< >In February 1814, Australia’s first currency was introduced. Known as the ‘holey dollar’, the coins were minted from imported Spanish ‘pieces of eight’. NSW Governor Lachlan Macquarie imported 40,000 Spanish reals and had convicted forger William Henshall cut the centre out of each, to double the number of available coins. The coins were then counterstamped so they could not be re-exported.

The outer ring became known as the holey dollar, with the centre named the dump. Governor Macquarie set the value of the holey dollar at five shillings, with 15 pence for the dump. These days, it is estimated there are only around 300 holey dollars and just over 1000 dumps remaining in existence. Today, a dump might sell for between $5,000 and $40,000, depending on quality. A holey dollar is likely to be worth $50,000 to $500,000.

For the trivia buffs amongst us, the Macquarie logo was designed to represent the holey dollar.

Friday Fun

It would seem the whacking of crypto has gone mainstream. It’s now not just media ‘outlets’ having a swing.

Insurance is certainly not something to laugh at, but this made us smile.

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.