Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Why the super cap matters, Aus’s new lifecycle shift, Golf or surfing?, The gold standard and more.

10th March 2023

As experts begin to unpack the proposed new tax on super accounts above $3m, the true consequences of the measure are starting to show. And Chalmers is now in full defence mode. In one press conference over the weekend, within a few sentences, he said the word ‘modest’ five times and ‘simple’ four times.

It’s a Shakespearean reminder of Hamlet, where his mother, Gertrude, is asked about the queen in a play who repeatedly states she would not remarry if her husband dies. The famous reply, “The lady doth protest too much, methinks“.

The tax might be simple for large super funds that do not need to administer it, but not so simple for the individuals affected.

What’s most important is that the changes are made in a sensible and fair way – which is where indexation and taxation of unrealised gains (in particular) invite so much heat. More on this below.

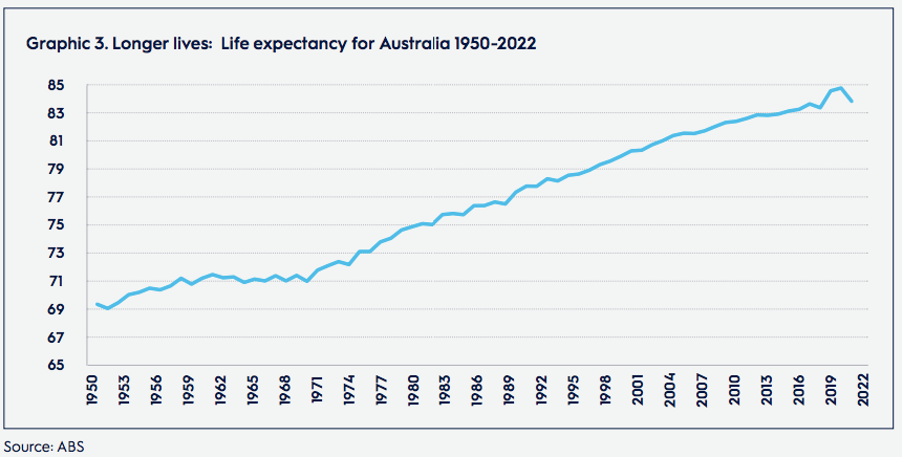

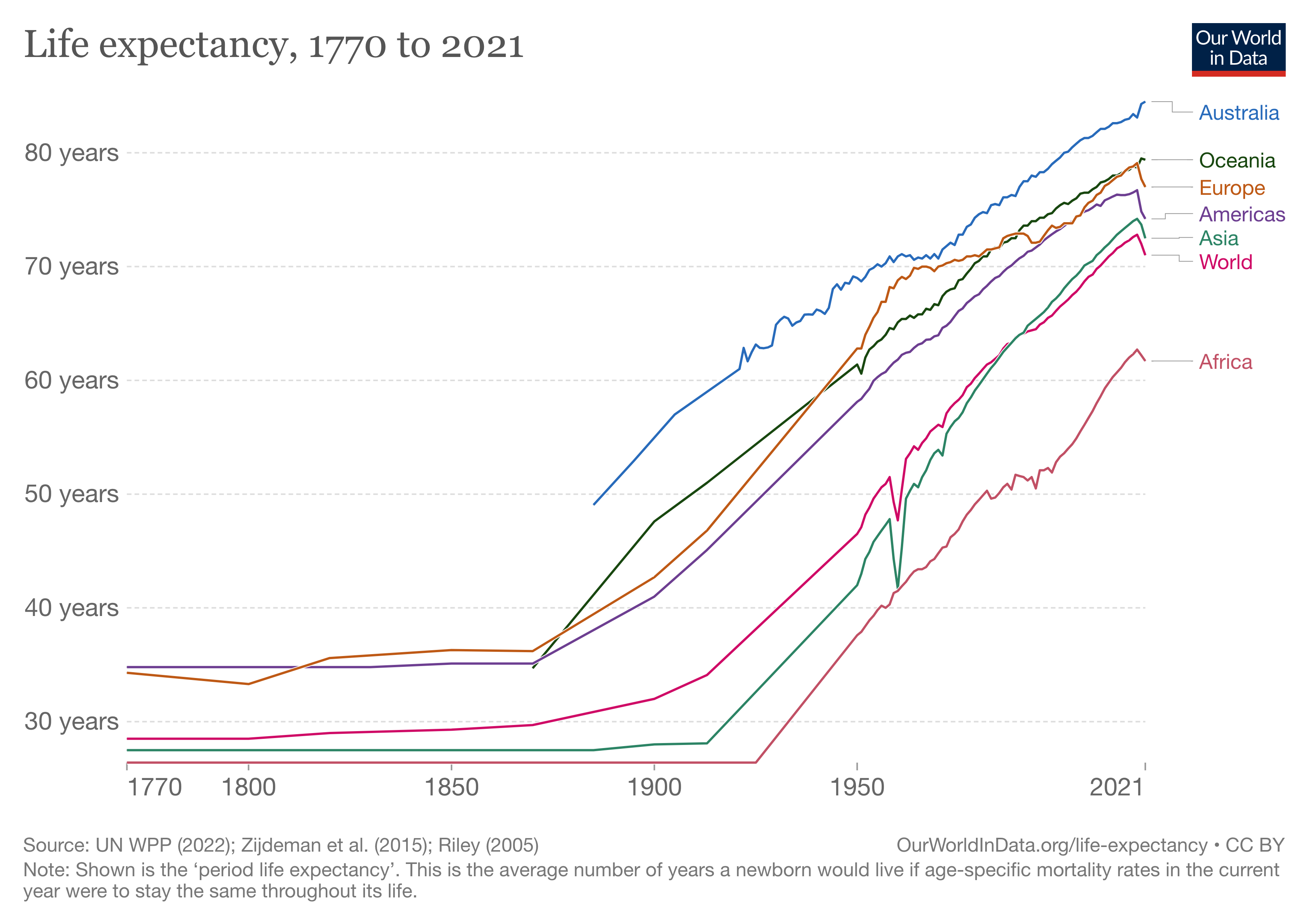

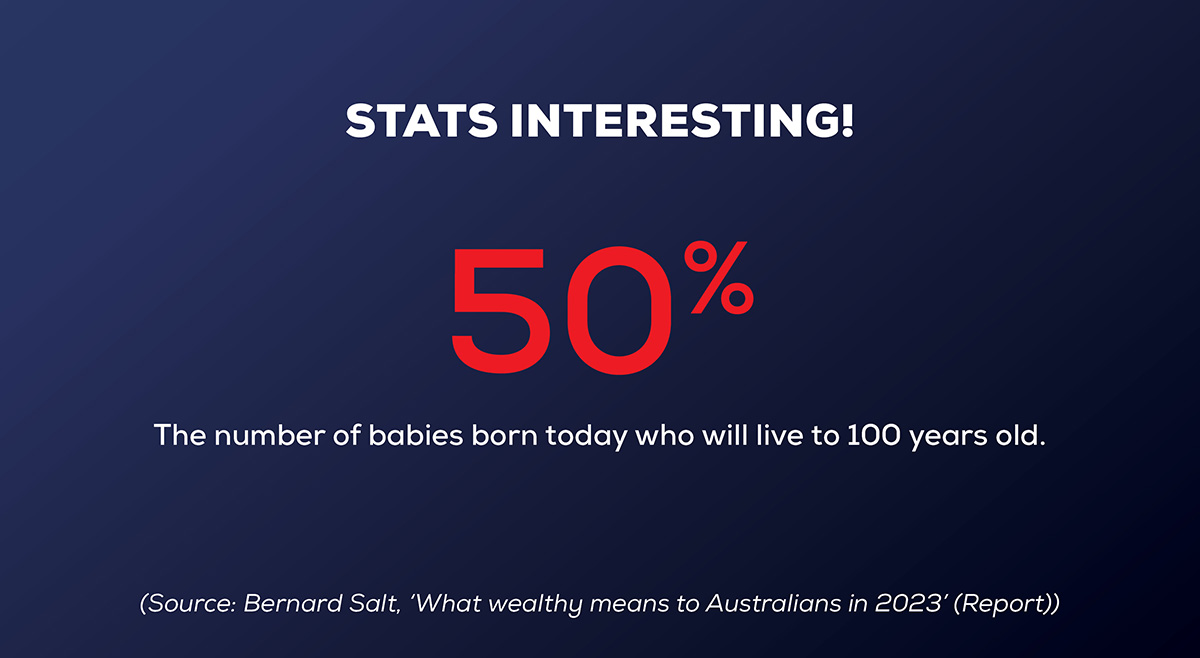

On the subject of living for a long time (in the context of superannuation), the latest life expectancy data has good and bad news for Australians. On the bad side, around the world, the pandemic has shortened life expectancy like no other single health issue for many decades, and this has continued into 2022/2023. On the good side, the data below shows that as it stands today, Australians will live to around 84 years (chart 1), the longest of any of the data sets in the comparison (chart 2).

Hanging on to decent superannuation balances is essential for Aussies as we will live so long!

Which is also why retirement planning is entering a new chapter. With an extra 20+ years to plan for (compared with the 1950s when the Boomer generation was born), we are seeing massive innovation in retirement income products. Sequencing, longevity risk products and a new age of investment (insurance) bonds have us particularly excited. As they say, watch this space.

Market Update

On interest rates

There will almost certainly be more rate hikes in Australia and the US. How many depends on the lagged impacts of the recent rate hikes on spending and jobs and how quickly the easing of supply constraints brings down inflation numbers. The effects of rate hikes on the residential housing market are beginning to flow through, particularly in construction and we may see bankruptcies in this sector accelerate with knock-on effects for trades, customers and suppliers. Of all countries, Australia is one of the most vulnerable to rate hikes due to its uniquely high proportion of floating rate debt and our large construction sector.

On inflation

It looks as though the worst of the inflation numbers are now behind us, as supply constraints ease, alternative sources of supply (energy, food etc..) kick in and as rate hikes slow spending. Although inflation will most probably remain stubbornly high, it is unlikely that we will return to the persistent double digit inflation of the 1970s (despite the media’s scaremongering).

On markets

Australian markets have already priced in assumptions that there will be big cuts to company profits and dividends.

In the US market, profit outlooks are no longer suffering from the ‘over-optimism’ of 2021/early 2022, but a ‘soft landing’ is still assumed with the likelihood of a recession.

Why the $3 million Super Cap Matters (even if you’re not a millionaire)

At the end of February Jim Chalmers announced a new Government policy set to double the concessional tax rate, from 15% to 30%, for superannuation balances over $3 million. If legislated the move will begin in the 25/26 financial year. It is scheduled to take effect after the next election (despite being passed into law in the current term). It won’t be retrospective.

So, is it good policy?

We’ll leave that to the political commentators and the voters to decide at the next election. From our perspective there does however seem to be a few major flaws.

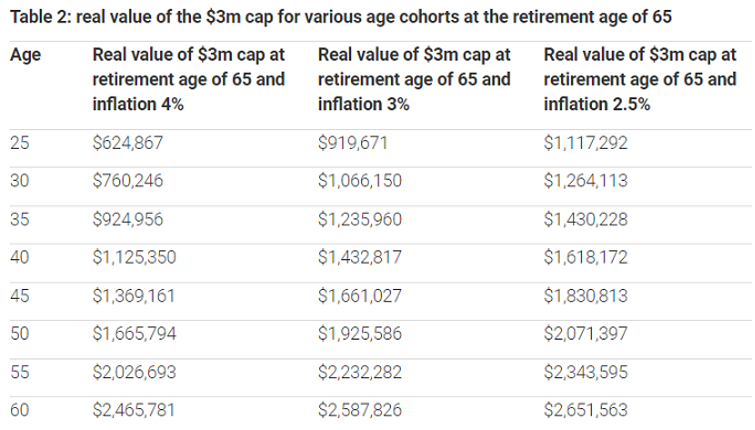

Currently the move is expected to impact 80,000 people, or just 0.5% of super accounts (in today’s money). However, lately, you might have heard of inflation. It is currently running at 7.8% and will erode the real value of the $3 million cap over time, affect many people and may even eventually remove the incentive to save in superannuation at all.

The Financial Services Council (FSC) which represents large superannuation funds states:

“If the Government does not index the proposed $3 million superannuation balance cap, 500,000 Australian taxpayers will breach the cap in their life and face a 30% earnings tax, including 204,000 Australians under the age of 30 … Leaving the cap stuck at $3 million will mean that in today’s dollars a 30-year-old will have a real cap of around $1 million, calling into question the intergenerational fairness of an unindexed cap.”

They provide this table showing the real value of $3 million at various inflation rates.

As if the millennials need another reason to be grumpy at the boomers!

Just as contentious is the issue of tax on unrealised investment gains. Mmm… This is a big departure from the existing tax system in Australia (or anywhere else in the world for that matter).

In Australia, the current tax regime only taxes capital gains when they are realised (if and when an asset is sold for more than its cost base). Under the new Super tax, all investment returns will be taxed, including ‘paper’ gains from rises in share prices, property values, or any other asset.

Note: a return is defined as any increase to your super balance from the start to the end of the year (after adjusting for contributions and withdrawals).

As much of the gains from shares and real estate are from inflation, it means investors will pay tax on the ‘paper’ rises in the value of assets due simply to inflation. Once again mmm… The government creates inflation through money printing and deficit spending, then taxes you on that inflation…

For assets with publicly available prices. Such as shares, managed funds, listed bonds etc., the unrealised gains will be easy to track and tax each year (the ATO has kindly offered to do this for you!). For unlisted assets such as direct real estate and collectables, it will have to rely on valuations, so it will depend on the frequency and the basis of the valuation (even wild guesses). Where an unlisted asset such as property is the main asset in a super fund (think farmland), the unrealised gains have the potential to be huge in any given year. The fund’s members will be left to come up with this extra ‘magic’ cash to pay the yearly tax despite having sold nothing in order to do so.

As most of the gains from long-term investment assets come from long-term value gains (most of which is inflation) rather than cashflows such as rent or dividends etc., this new Super tax would amount to a heavy tax on long-term investments ‘aka’ a wealth tax on the big savers.

As an aside, we’d also be interested to know how the government is intending to deal with life insurance payments to super funds.

It is only draft legislation at this stage. We can’t help but think that once the broader implications are fully understood, it could not possibly pass through parliament in its current form (the cynic in us queries whether this is the idea – think concessions for the Teals in Kooyong and Wentworth!).

If it does pass, it will add complexity and costs to running super funds. This and other mooted plans for super would appear to depart from the government’s overarching goal of simplification.

Chart of the Week

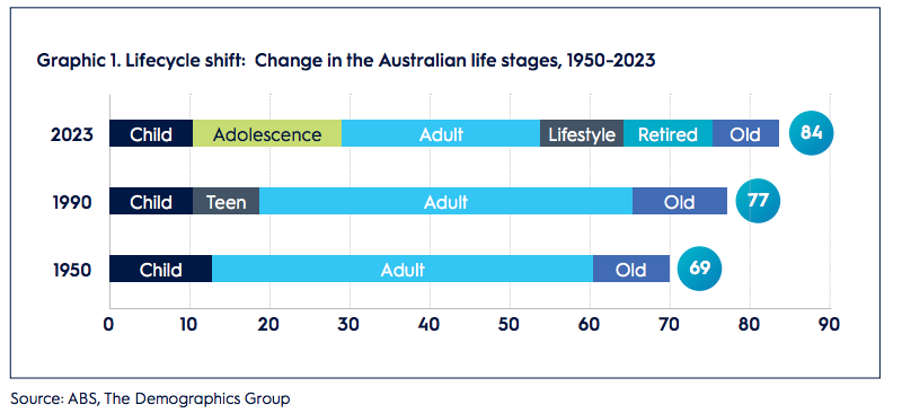

When does adulthood actually begin? Legally, it begins the minute we turn 18, but according to new research by demographer Bernard Salt, Australians aren’t becoming truly adult until they hit 28 (we can hear you giggling from here).

That’s because longer periods of training for knowledge-based jobs have birthed an extended adolescence that spans from 12 to 28.

And at the other end of the spectrum, we’re also getting older later. Rather than retiring into instant old age, many Australians are cruising through a “lifestyle” period towards the end of their career, before retiring.

According to Salt, it’s changing the way we think about wealth.

The report highlights the need for personal advice, because the goalposts had shifted to an ability to “pursue unique passions and goals” across the age spectrum.

Modern day wealth requires us to consider what our goals are and to put a financial plan in place. The earlier we do this, the more likely we are to achieve those goals,” Salt says.

Wealth Wisdom

Marketing guru Seth Godin has written a new post in his blog every day since 2008. This bit of career advice is gold and also applies to investing:

Golf or Surfing?

Every golf scorecard has a map of the course on the back. Moving the hole placement is a big deal, accompanied by meetings and oversight. A big shift is whether or not it rained last week.

On the other hand, every wave is the first and last of its kind. It has never happened before and will never happen again.

Golf is an endless asymptotic journey toward elusive perfection.

Surfing, on the other hand, is about wayfinding. A surf park with a repeated wave might be useful for training, but it’s not surfing.

Metaphor over, the question is: what’s your job like?

It gets a lot easier if you bring the appropriate mindset. It’s hard to surf with a putter.

Using Godin’s terminology, investing is more like surfing than it is like golf – meaning it is an art as well as a science. The science of investing is crunching data and reading up on history, the art of investing is knowing which lessons from the past are useful and whether those lessons will be relevant for the future. Because each market wave is unique, the art is often more important than the science. Investing by only looking at the past is like driving by only looking at the rear-view mirror – difficult but doable if the road ahead is exactly like the road behind, dangerous if and when there is an unexpected twist in the road!

Insurers Put on Notice Over Claims Handling

Highlighting the importance of the underwriting and claims process, when it comes to personal insurance is a recent review by ASIC into claims handling.

The commission’s review of nearly 4,800 individual disability income insurance claims has found deficiencies in protecting consumers from unfair practices in non-disclosure investigations and physical surveillance.

How to protect yourself:

- Beware of ‘morning TV’ traps and insurance sales over the phone

- Work with a specialised risk expert to ensure:

- You have undergone a full and robust pre-assessment and underwriting process*Remember – ‘you don’t know what you don’t know’, have someone who does walk you through the process

- You understand the definitions within trauma contracts

- You understand your Total Permanent Disability (TPD) options at end of a claim

- Your premiums are optimised for affordability

Please talk to us if you would like a health check of your current policies. We do have a dedicated risk specialist on the team who can be contacted directly via email gerry.mcavoy@finsecpartners.com.au

This month in (financial) historyIn March 1933, at the height of the Great Depression, Franklin D. Roosevelt was inaugurated as the 32nd president of the United States promising an “adequate but sound” currency. The next day, a Sunday, he declared a nationwide bank moratorium and declared to a group of private advisers “we are now off the gold standard”.Hereafter, the government seized all gold bullion and coins via Executive Order forcing citizens to sell at well below market rates.The stated reason for the order was that hard times had caused “hoarding” of gold, stalling economic growth and worsening the depression.The actual rationale behind the order was to remove the constraint on the Federal Reserve preventing it from increasing the money supply during the depression. The Federal Reserve Act (1913) required 40% gold backing of Federal Reserve Notes that were issued. By the late 1920s, the Federal Reserve had almost reached the limit of allowable credit, in the form of Federal Reserve demand notes, which could be backed by the gold in its possession.This was the era of the gold standard.

Thought of the Week

Flavour of the week

With Easter approaching hot cross buns have been a staple on supermarket shelves for weeks now and apparently traditional just doesn’t cut it anymore…. as Marlon Brando said in Apocalypse Now: “The horror… the horror…”

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.