Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View – Markets, Unemployment rates, Tax reforms & More…

|

24th April 2024 |

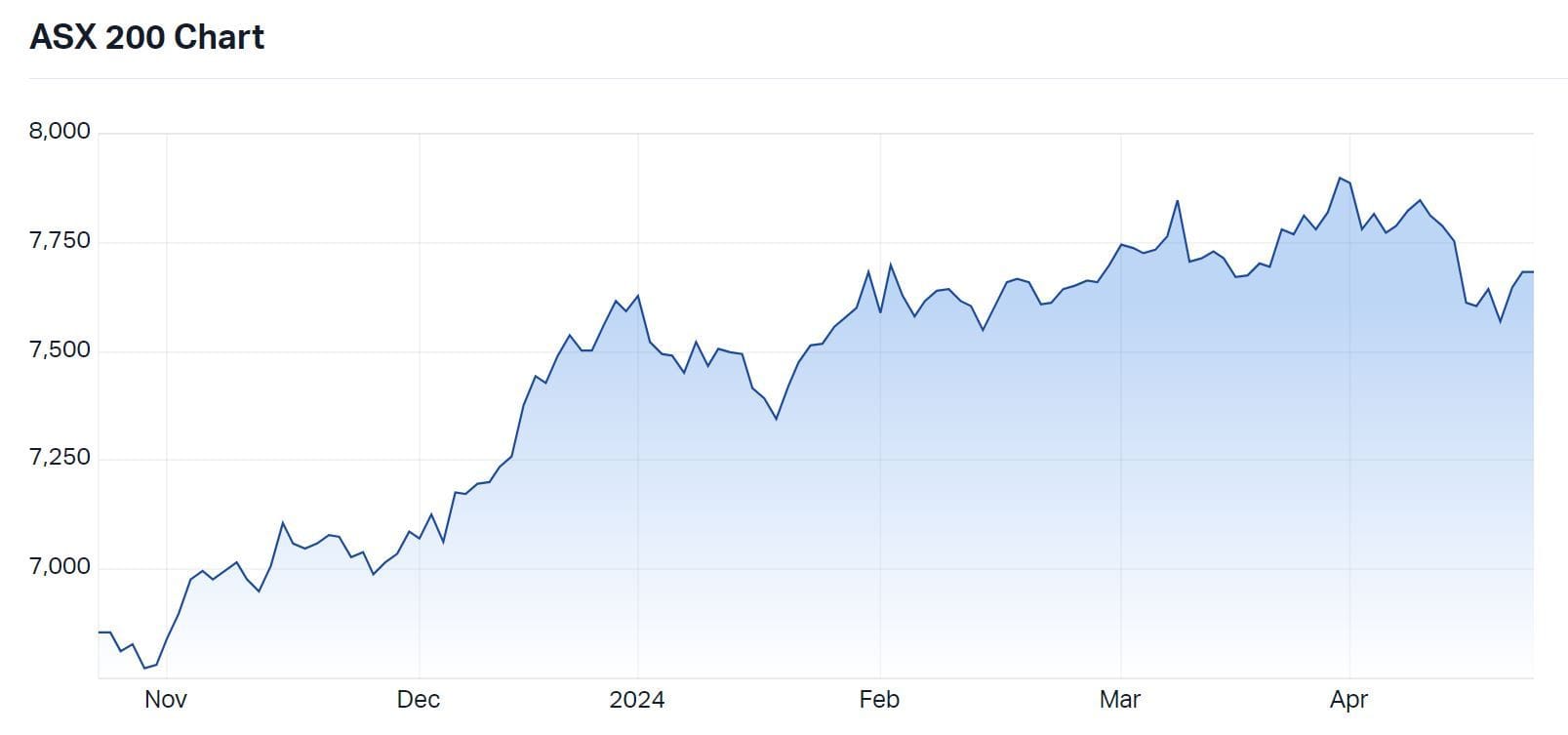

Just when we were getting used to the idea of markets looking ahead into a recovery, April has seen a reality check. Having rallied by 17% since October a combination of an escalation in the Middle East and the realisation by markets that rates might be higher for longer, saw the calendar year’s gains (about 3.5% at the peak) taken away in a matter of days. Inflation is proving stickier than expected meaning markets have repriced on the assumption that they will not get midyear rate cuts as anticipated. The good news is that there appears to have been a de-escalation in the Middle East and markets have stabilised. It looks as though the global investment landscape might be transformed over the coming months as the trajectories of major economies start to diverge. Europe has slowed and, in some parts, commenced the rate reduction cycle however, the US has maintained its momentum suggesting there will be no rate cut sugar hits this year. A soft landing remains achievable in the US subject to no surprises from left field. The extent to which the Fed is willing to accept somewhat above target inflation for an extended period remains a key question for the outlook. This environment underscores the importance of global diversification, prudent risk mitigation and constructing resilient portfolios through active management. We expect the traditional inverse correlation between stocks and bonds to resume with the potential for fixed income investments to appreciate if the pricing of recession risk rises again. |

|

|

According to the Reserve Bank, just 14 per cent of all transactions in Australia are still made with cash accounting for just 8 per cent of the total value. More than 40 per cent of us no longer carry any cash at all, while cheques are about as common as receiving a fax or watching a DVD. The sharp decline in oujr use of cash as a means of payment was turbocharged by the pandemic. Money transportation or cash-in-transit businesses are now experiencing what photographic paper companies such as Kodak, Agfa, and Fuji went through at the turn of the century when we all started taking photos on our smartphones and stopped having our photos processed. Armaguard, owned by the Linfox Group, is Australia’s largest currency transport business, services about 90 percent of the cash-in-transit market but even having a monopoly—after buying out its only competitor, Prosegur—the company is struggling. Last year, Armaguard said it would need a $190 million lifeline over the next three years to stay afloat. In early April, the company rejected a $26 million rescue offer put together by some of Australia’s biggest banks and retailers, which would have required it to open its books. Instead, it opted for a smaller $10 million package from its parent company that will see it through the next few weeks. The company’s uncertain future is worrying the Reserve Bank and major retailers. The RBA believes in maintaining cash as a store of wealth and means of payment for many people, particularly as a backup option when electronic payment systems are unavailable or offline. One idea is to form an industry co-operative involving the major banks, regional banks, and large retailers, including Bunnings, the big supermarkets and Australia Post, which provides cash services in its branches under contracts with banks. Such models already exist across Europe; in the UK, the not-for-profit Link network connects almost all of the country’s ATMs and allows consumers to withdraw cash regardless of who they bank with. While Australians love the convenience of card, phone and watch tapping at point of sale, few of us stop to consider the implications and consequences of our habit change. Our financial system is anti-privacy by design, meaning our banks and financial institutions, other companies, and governments are increasingly tracing every transaction or purchase and building valuable profiles of our lives and behaviours. However, this data collection doesn’t always have to be considered evil, as the banks are also using it for the benefit of their customers and the strength of the sector as a whole. Using data analytics, banks can assess the creditworthiness of individuals who might not qualify for traditional loans based on credit score alone. Personalised financial guidance is also a growing part of most banks’ online banking and app offerings. Fraud detection and prevention now make up one of the largest budget lines in financial institutions. By analysing spending patterns and identifying unusual activity, banks can prevent fraudulent transactions and protect their customers from financial loss. Despite its decreasing use for payments, cash remains important for segments of the community, including the elderly, migrants, those with disabilities, and spenders seeking anonymity. It is also Federal Government policy that cash should be made available to those who wish to spend with it. However, if cash usage continues to fall, it could be argued its simply uneconomic for banks and other ATM providers to offer cash services in some areas, particularly the regions.

|

|

|

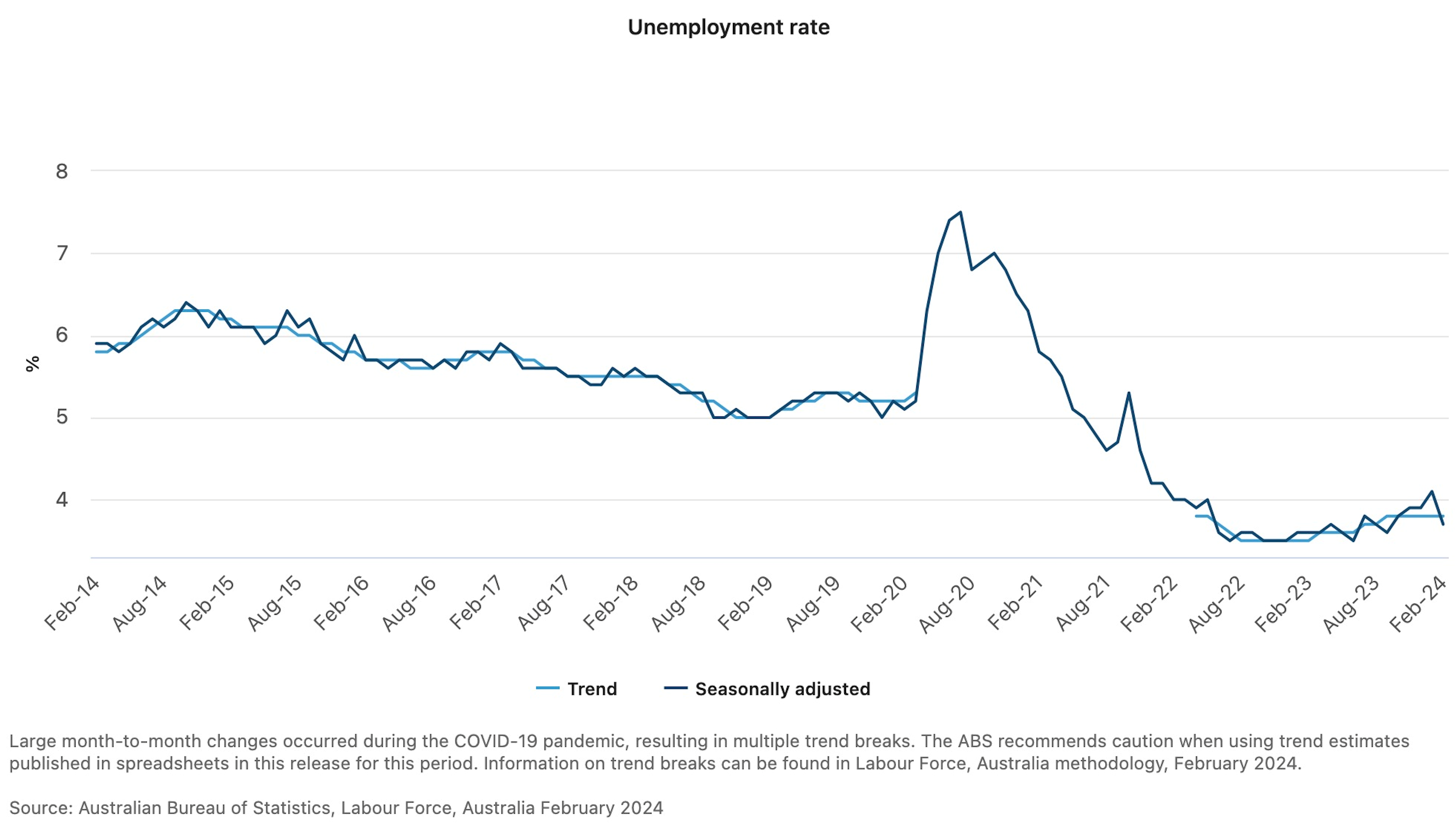

| Australia has an enviable high participation or low unemployment rate, but how real is the rate, and to what extent is it taxpayer-funded?

The unemployment rate unexpectedly fell to 3.7 per cent in February from 4.1 per cent in January and rose slightly to 3.8 per cent in March.

According to new research from investment bank Jarden (as reported by Michael Read in the AFR earlier this month), about 130,000 of the 437,000 people who gained work in the 12 months to February 2024 were employed in the National Disability Insurance Scheme-related sub-industries such as allied health and non-childcare social assistance. Jarden economists Carlos Cacho and Anthony Malouf say the growth in publicly funded employment is masking the slowdown in the private sector jobs market. Public sector employment grew by 6 per cent over the 12 months to February, while growth in demand-sensitive parts of the private sector, such as construction, retail, and manufacturing, was just 1.4 per cent. Using data from the monthly labour force survey, the Jarden economists found that NDIS-related work accounted for 30 per cent of annual employment growth despite representing just 6 per cent of jobs. According to the Jarden economists, the strength of public sector employment is one reason the labour market has shown surprising resilience in the face of a material slowdown in consumer spending. “All else being equal, without jobs growth in NDIS-related areas, the unemployment rate would be 4.6 per cent… whilst this is unrealistic, given some workers would have moved into other jobs, it illustrates how much support the program is providing to the labour market and economy,” Mr Cacho said. Anyone with a family member who has a permanent or significant physical or intellectual disability appreciates the role the NDIS has in the broader Australian community. Nevertheless, costs for the NDIS have been rapidly growing. In 2023, it was the second largest source of government expenditure after the aged pension. It has been growing rapidly in part due to the number of new participants but also due to issues with waste, inefficiency, and inflationary costs. Participant numbers hit 646,000 in December 2023, putting the program on track to exceed projections from the May 2023 federal budget that the scheme would cost $42 billion to run in 2023-24. Recent budget blowouts have been due to a surge in children with autism and developmental delay joining the NDIS. The Albanese Government has begun overhauling the NDIS in order to reduce it’s current unsustainable 23 per cent annual growth rate to 8 per cent by 2026. Legislation is currently before Parliament that reflects the recommendations in last year’s NDIS review to address administrative delays, improve access to early intervention services, eliminate fraud and dodgy providers and ensure better planning and sustainability. The exact impact of taxpayer-funded programs on the unemployment rate is difficult to isolate, nor is it a recent phenomenon. Government subsidies, incentives and job creation programs have been propping up employment figures without addressing underlying structural issues since the ABS was created. JobKeeper, during the COVID-19 pandemic, which provided wage subsidies to keep employees on payroll, was hailed for its benefits but, in reality, was another taxpayer-funded scheme that distorted the true unemployment rate by masking the extent of job losses that would have occurred without government intervention. Moreover, the quality of employment matters just as much as the quantity. Even if the unemployment rate is low, if a significant portion of jobs are low-paying, part-time, or precarious, it may not reflect a truly healthy labour market. This is often a concern raised in discussions about underemployment, where individuals are working fewer hours than they desire or are overqualified for their current positions.

While Australia’s low unemployment rate may indeed reflect genuine improvements in the labour market, it’s essential to critically evaluate the factors contributing to this trend and consider the quality and sustainability of employment opportunities. Additionally, ongoing scrutiny and analysis are necessary to ensure that taxpayer-funded initiatives are effectively supporting job creation and economic growth without masking underlying systemic challenges. |

|

|

This chart highlights the challenge facing the US Federal Reserve with sticky inflation. Put simply, sticky inflation means prices continue to creep up rather than stabilise. And once they rise, they rarely, if ever, actually fall. The inflation rise in early 2021 was initially considered “transitory,” but it persisted into 2023 (Swan Global Investments) and now into 2024. Signs of Stickiness:

Combating Sticky Inflation:

Uncertainties:

|

|

|

That’s the number of overseas tourists (officially short-term visitors) to arrive in Australia in February 2024 – a year-on-year increase of 257,240. And that is in one of our usually quieter months. We’re not back at the pre-COVID levels of 2019, when 8.7 million tourists visited Australia from overseas and we had an industry worth $166 billion. But we are creeping up back. However, that depends on your data source – the ABS site, which is responsible for the latest figures, says there were 7,187,430 visitor arrivals in 2023, nearly double the number in 2022, which was a sad (but understandable) 3,694,380. But Tourism Research Australia, part of the Commonwealth Government’s Australian Trade & Investment Commission is claiming only 6.6 million international visitors last year. Either way, one of the biggest takeaways from the latest data is that China was the largest source country of tourists, accounting for 18% of all visitor arrivals. China was followed by New Zealand (9%) and the USA (7%). These latest figures have been causing a stir because, as we appreciate, tourism plays a significant part in Australia’s economy, contributing to both GDP and employment. These December 2023 figures from Tourism Research Australia for international tourism explain why:

|

|

|

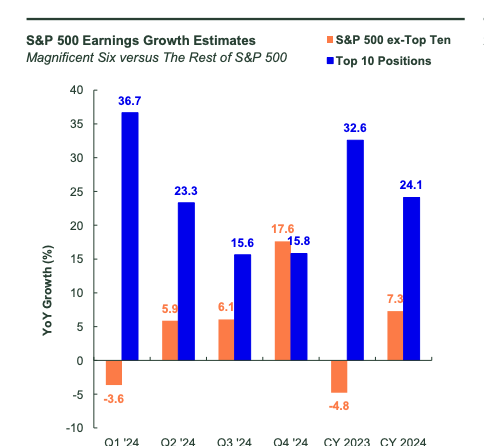

| The US stock market has been on a tear thanks to the rise of large technology companies, and some worry it will not continue.

Still, many believe that overall valuations are not overstretched, even with the recent increases. Although there may be some volatility related to earnings, elections, interest rate cuts, or political events, most market watchers are optimistic.

According to a recent Capital Group analysis, here are five reasons why equities may continue their sweet spot:

So, what’s our overall takeaway here at The View? Look beyond the index and stay optimistically cautious. |

|

|

When the head of a major bank goes off-script, freestyles ideas or puts their head above the parapet to outline a range of structural changes to Australia’s taxation structure in front of the big end of town, it’s big news. Speaking at The Australian Financial Review’s recent Banking Summit, CBA CEO Matt Comyn was asked an off-the-cuff question about how he would revive productivity specifically through political, tax, and industrial relations reform. The question and answer were framed in the context of the 2023 Intergenerational Report, which forecasted Australia’s growth to average around a disappointing 2.2 per cent over the next 40 years. Much to the horror of his CBA corporate affairs team, Comyn then proceeded to list off a range of reforms – which media love to describe as “sweeping” – that would drastically simplify income taxes, raise the GST, ban cash payments above a threshold and impose a levy on technology giants in order to revive Australia’s flagging economic prospects. The head of the nation’s largest lender argued that turning around Australia’s projected long-term growth slowdown required a focus on “growing the pie, international competitiveness dynamism, and supporting both the mobility of labour and capital across the economy”. Align political cycles Firstly, Comyn added his voice to calls from other big bank chiefs to extend all election cycles—federal and state—to four terms to provide policy certainty. He said state elections should be on the “off-cycle (to the Federal Election) … so every two years there’s an election and nothing in between”. This was “because one part of the tax reform debate is difficult with harmonisation in particularly with the states”. A simple, personal tax scale Comyn’s personal tax reform would be to make the first $20,000 of earnings subject to no tax, then 20% tax on incomes above $20,000 up to $80,000, 30% on incomes above $80,000 up to $300,000 and a top rate of 45% above that. All personal income tax deductions would be abolished, with the exception of charitable donations. GST increase The GST would be increased and broadened with the rate increased from 10% to 15%, which would raise $60 billion – $20 billion of which would be spent to compensate low-income pensioners and welfare recipients. Cash payment thresholds All cash payments would be limited to $500 max to curb the black economy operating outside the tax system. Any cash payments of over $500 would be made through the electronic payments system, he said. This would likely save the government about $5 billion in tax revenue leaks. Abolish payroll tax and stamp duties Comyn believes the company tax rate should stay at 30%, but he wants state payroll tax and stamp duties on property purchases and insurance scrapped, saying they make Australia less competitive and are “extremely inefficient taxes.” Tech tax and better Government spending Comyn’s concerns about big multinational technology companies such as Meta and particularly Apple have been widely reported. He wants them to be forced to pay multiple billions in “tech tax” on their local turnover or payments made to offshore affiliates. “Whether something like a turnover levy, or you could seek to limit their transfer payments to somewhere like 80 per cent … (to) the Cayman Islands,” he said, referring to the big offshore companies’ practice of making payments to affiliates to minimise tax. Comyn acknowledged there would be “difficulties” navigating tax treaties to execute the latter plan but said the measure could capture about $5bn in tax receipts. Overall, Comyn acknowledged his radical tax overhaul would leave a $30 billion fiscal gap to fill. But as The Australian noted, his ideas represented some of the “blunt” policies needed to lift economic growth forecasts which Treasurer Jim Chalmers has labelled inadequate. Comyn demonstrates that genuine reform requires bold and courageous change, without which we will never shift the dial. The video is behind the paywall but for AFR subscribers, you can watch it here: |

|

|

|

John Maynard Keynes once said: “When the facts change, I change my mind.” He also said: “The difficulty lies, not in the new ideas, but in escaping from the old ones.” Nobel Prize-winning British-American economist Sir Angus Deaton has recently been changing his mind about his own long-held views and, according to a piece he penned online for the International Monetary Fund, he’s finding it a “discomfiting process’’. First a bit of background: Deaton is a renowned economist known for his ground-breaking work in the field of economics, particularly in the areas of health, development, and inequality. He has held prominent academic positions at institutions such as Princeton University, where he was a professor of economics and international affairs. He is best known for his research on consumption, poverty, and welfare. One of his significant contributions is the development of the Almost Ideal Demand System (AIDS) model, which provides a framework for analysing consumer behaviour and demand. In 2015, Deaton was awarded the Nobel Prize in Economic Sciences for his “analysis of consumption, poverty, and welfare.” His work has had a profound impact on the field of economics, shaping both academic research and public policy discussions around the world. In the IMF piece, Deaton argues that economists need to question their own assumptions and methods in light of recent events.

Reflecting on Deaton’s change of heart, The View wonders what would happen if politicians and economists actually debated the middle ground of economic rationalism and social justice with a long-term agenda rather than pandering to the short-term election cycle. Would we be seeing real productivity, tax and welfare reform rather than the politically expedient headline grabbing policies of recent western governments. |

|

|

Does this cartoon resonate with you? When’s the last time you got a genuine card or letter posted by hand? In an age of relentles emails, SMS, group chats on WhatsApp, and habitual Facebook birthday posts, snail mail might seem vintage, but it’s so much more meaningful. It’s like receiving someone’s words or thoughts gift-wrapped – priceless. |