Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Intergenerational report, China’s millennials, 150 years of Australian shares and more.

Issue: 9th July 2021

The 2021 Intergenerational Report is in.

The 2021 Intergenerational Report (IGR) was released on the 28th June revealing the treasurers educated guess at what Australia will look like in 2060.

It is a five-yearly reminder that, without action, an ageing population, and other issues will leave public finances looking ugly.

To use Treasurer Frydenberg’s own word, the latest IGR was “sobering” on two main fronts.

- The population is growing slower and ageing faster than expected.

- Baby boomers are now of retirement age (57 years to 75 years old). As recently as 1982, there were 6.6 people of working age for each person over 65. It is now 4 and in 2060 will fall to 2.7.

Treasury called the ageing of our population “Australia’s greatest demographic challenge” estimating that from 2020 to 2060, the number of people aged 65 and older will double to around 9 million (23% of the population), up from only 16% in 2020.

The impact on workforce participation and the flow-on effect will be profound, not to mention the implications for health, pensions, taxes and aged care. And, with superannuation balances set to increase significantly as the system matures, we can’t help but think that super will remain a socially and politically divisive issue for all of our lifetimes.

- Australia’s fertility rate at 1.6 is well below the replacement rate of around 2. However, the report is optimistic about the rebound to migration stating that in the last decade, net overseas migration accounted for about 60% of population growth and is expected to contribute around 74% of growth by 2060.

This of course will depend primarily on government policy, but it shows how important a sustained annual intake of migrants is. A strong post-pandemic recovery is imperative!

- The Australian economy will continue to grow but slower than previously thought.

- Any promises of ‘back in black’ were decimated by the pandemic’s impact and has left the underlying cash balance in deficit for the next 40 years, with an estimate of 2.3% GDP growth p.a. by 2060. Gross debt is projected at 41% of GDP and net debt 34% of GDP in 2060.

Although the new numbers are high (gross debt was expected to fall to only 15% of GDP but is now forecast to peak at over 50% of GDP by 2030), the net debt is less than half the average of G20 advanced economies (a frightening statistic albeit of a different kind).

The treasurer had this to say about it.

“Once our economic recovery is secure, we have a responsibility to again do the work necessary to restore our finances and rebuild our fiscal buffers.”

The prediction that debt will remain high for 40 years under current policy settings means that fiscal repair will no doubt become the parties battlefield during the upcoming election.

We are guessing that lifting productivity, reforming age-based tax breaks, improving migration and lowering barriers to workforce participation for women and older Australians are also set to become popular battle cries. After all, economic growth is driven by the ‘3 Ps’ (population, participation and productivity). At some stage, the world’s population will peak, so we better get pretty good at the other two!

Expect to hear plenty of noise and arguments about who is best to handle it ‘all’ in the months ahead.

A copy of the full report can be found here.

The next Baby Boomers are China’s millennials

Sticking with the generational theme, a recent Financial Review article authored by Russel Chesler, head of investments and capital markets at VanEck, has touted a new world order in which younger Chinese consumers are taking over Baby Boomers with their influence.Highlighting the fact that Baby Boomers have been the most influential generation in terms of commerce and world markets since World War II, it considers how markets have responded to the rise of Baby Boomers during this time.

“In 1948, when the leading edge of this big population group was turning two years old, someone recognised that kids love toys so created Toys R Us. In 1955, as some Baby Boomers approached nine years old, the McDonald brothers combined a child’s love of burgers, family dining and speed to create the modern fast-food restaurant.

Jump forward a few years. This population group is exiting their 20s and wants to stay active and young. Enter a sportswear company already established in the Pacific Northwest: Nike listed in 1980.”

You get the point – creating a good or service that is needed and wanted by a big population group equates to success.And so, the argument goes for China’s millennials.

- China is experiencing the fastest expansion of the middle class the world has ever seen (during a period when the global middle class is expanding at a historically unprecedented rate).

- China’s population is relatively young (China had its own Baby Boom in the late 80s and 90s)

- This group of millennials are privileged, having grown up in a period of economic reform and the country’s opening (70 per cent own their own home compared with 35 per cent in the US and 30 per cent in Australia).

China is on a trajectory to becoming the world’s biggest economy, and it would seem its China’s Millennials who could be at the forefront of that economic growth. Opportunities in companies and sectors with good exposure to these Millennials is an area we certainly will be watching closely.

The full article can be accessed by clicking here. Albeit behind the paywall.

Chart of the week

The true scale of Australia, the planet’s sixth-largest country by size, just got real! Digest this map properly, and we guarantee you will never view our country’s landmass (or that of many other countries) in the same way ever again.

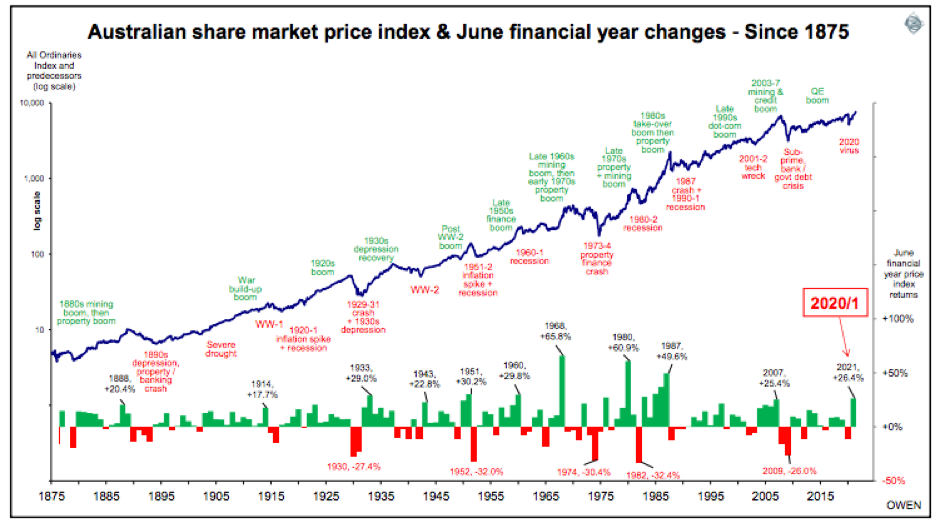

Australian shares – good, better, best…

The broad Australian share market has just posted its best June financial year since the 1980s. It is an extraordinary performance that almost no other country in the world can match.Incredibly, when indexed over the past 150 years, it shows that the growth rate for share prices across the market as a whole have been relatively consistent over very long periods – world wars, depressions, bouts of hyperinflation and deflation, changes in political regimes, global trade patterns and everything else along the way.

What is of particular interest is the picture it paints with regard to previous years of great returns.

- 2007 at the top of the speculative China/credit boom, before the 2008-9 GFC crash

- 1987 at the top of the 1980s speculative take-over boom, before the October 1987 crash

- 1980 at the top of the late 1970s property/mining boom, before the recession sell-off

- 1968 at the top of the 1960s speculative mining boom, before the mining crash

- 1960 at the top of the late-1950s consumer finance boom, before the recession sell-off

- 1951 at the top of the post-war boom, before the 1951-2 Korean War inflation sell-off

- 1914 at the top of the war build-up boom, before the outbreak of WW1

- 1888 at the top of the 1880s mining and speculative property booms, before the property/banking collapse that triggered the 1890s depression

Mmm… While past performance is not an indicator of future performance, it certainly serves as a reminder that the very drivers of markets (particularly speculative behaviour) can also be responsible for their undoing. Peeling back the curtain on the good years to identify possible risks is a critical mandate to good investing.A big thank you to Ashley Owen, Chief Investment Officer of Stanford Brown, for compiling this data.

Intergenerational Wealth Planning

In recent years we have found matters relating to intergenerational wealth planning are increasingly front of mind for our clients. Questions such as, should we pass on wealth earlier? How do we balance our retirement needs whilst helping children? Sometimes even more fundamental considerations arise such as, transferring your wealth, planning for ageing and what are the questions to consider before you make a will?As part of our focus on intergenerational wealth planning, we will be answering these questions and many more in upcoming views. As an introduction to this series, this missive discusses probably the most common concern that families raise with us – how to help adult children, while balancing one’s own retirement.

Naturally increasing life expectancy and higher expectations of a comfortable retirement means this has become more of a balancing act than it once was. There are some families who will be comfortable enough to fund their own retirement and have the ability to pass on wealth to the next generation. For others, they will be left wondering can I do it? And, what is the best way to do it?The key is to start with what you need. Retirement changes over time and spending in retirement is not linear. Questions to consider include: What does your retirement look like? How healthy are you? Do you want to preserve capital or spend every last cent?

Once you have planned for your own needs, you can be confident in exploring how you might wish to use the rest of your wealth, including whether and how you help your adult children. The most common routes tend to be around educating the grandchildren or providing a loan or gift to help them onto the property ladder. But not all help you provide adult children needs such a large capital outlay. For example:

- Assisting your children with the insurances they need to ensure they have a plan B. This is the gift that keeps on giving. It ensures neither you nor your child’s finances are derailed if something unforeseen happens, such as job loss through sickness or accident.

- Helping children to get on the right track with financial advice. As simple as a conversation with a financial adviser to discuss:

- how you invest in the share market

- understanding the role superannuation plays

- why you might need insurances; and

- how to save for a home deposit (what are your options).

- Shared experiences. You may wish to use your funds to provide experiences to your children or grandchildren paying for family holidays, funding pursuits such as music lessons or theatre.

- Never underestimate or undervalue what you already do.

- Finally, fair Vs equal. Do you want to treat all your children equally, or do different circumstances require a different approach?

Balancing your retirement and helping your adult children traverses investment strategies, taxation structures and estate planning. We encourage you to take the time to think about what it is you are trying to achieve.

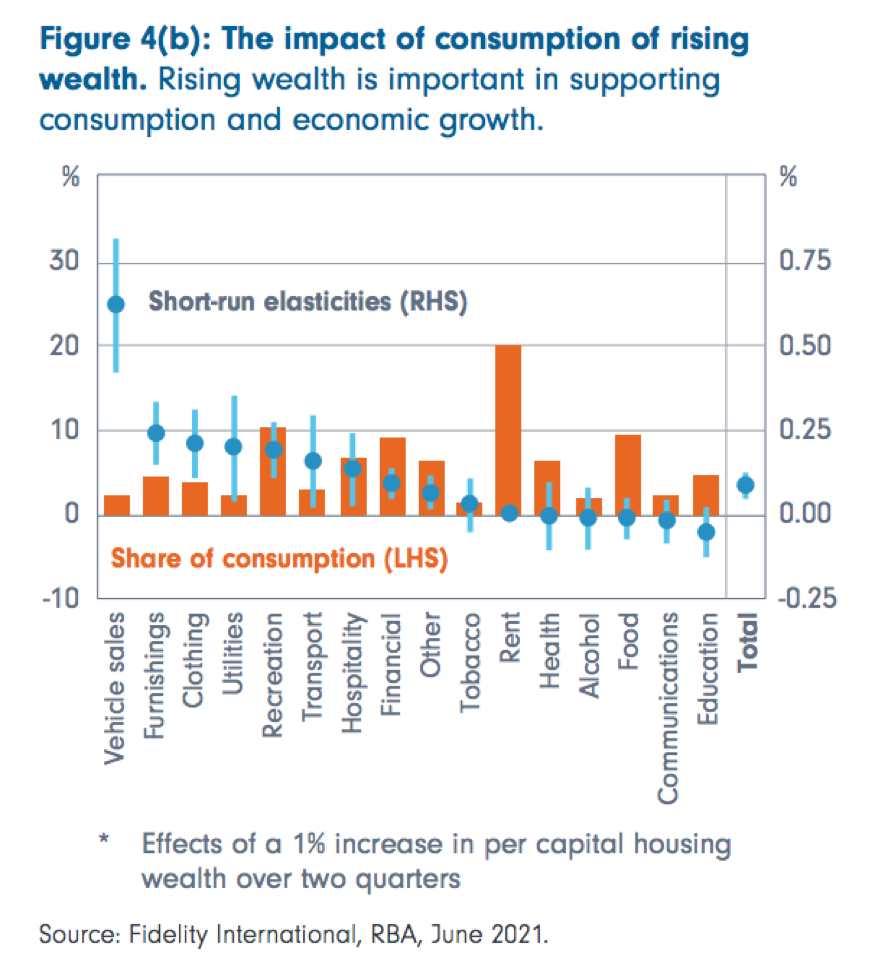

Interest rates, house prices, super: keys to Australia’s household wealth

This white paper from Fidelity examines the ‘wealth effect’ for Australia and its households, especially due to rising residential property prices.

One of the most important impacts of lower interest rates has been rising asset prices, which leads to increased levels of household wealth and consumption. These changes in the ‘wealth effect’ are a key factor in assessing the outlook for the Australian economy, given that a large share of our economy is driven by household consumption.

For investors, understanding the impacts of higher house prices on wealth and which companies and sectors stand to benefit most from the increased consumption that will likely follow can help in the pursuit of long-term share market gains.

The whitepaper can be found here.

The post-pandemic 1920 Olympics

With only two weeks left until the Tokyo 2021 Olympic Games, controversy still dominates the build-up given the public health backdrop, both locally in Japan and globally. That being said, the 2021 European football championships are currently taking place across the continent. Despite the natural health concerns, the attention quickly switched from the off-field health debate to the on-field action, and it’s not unrealistic to expect the same will happen this month once the flame is lit.100 years ago, Antwerp hosted the 1920 Olympics. It too, was a Games held post a global pandemic but with the added tumult of the first world war.

There were no Winter Olympics or Paralympics in 1920; the modern Olympics were less than a quarter of a century old at that time; amateurism dominated, and there were few professional coaches around. Far fewer women were able to participate then, and only 29 nations were involved in a much smaller event.The story of the Antwerp Games offers a fascinating account of just how much the Olympics have changed across a century and the degree to which questions of politics, economics, sociology and health in various guises can never be evacuated.

This short video is 10 minutes of footage from the Antwerp Olympics. The first minute contains wonderful scenes of athletes training aboard ships as they travel to the games – well worth the watch!

Stay safe and look after one another. Enjoy the weekend and as always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.