Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – The Budget Issue

|

8th April 2022 |

| A quarter of 2022 has passed us by in the blink of an eye, bringing a Federal Election with it. An event usually left for mid-year it was brought forward by a government looking to lay out its vision before a pivotal May vote.

The headline grabber was cost-of-living relief in a budget centred around more spending but lower deficits thanks to a windfall from faster growth and a resources boom. It’s hard to think of any Australian who doesn’t get something out of this budget (Treasurer Josh Frydenberg’s fourth) – High earners with big cars will enjoy the temporary cut to fuel excise, for pensioners and those on benefits there’s a one-off $250 cost-of-living bonus, and for Australians earning up to $126,000 there’s a $420 boost to the tax offset. Perhaps the more complex dilemma for Australia will be how the government returns to a position of ‘economic repair’ via productivity growth rather than austerity. We hope you enjoy this special Budget edition of the View. |

|

| From an industry perspective, it was not the ‘supercharged’ budget of recent years.

In fact, the only superannuation announcement of note was the extension of the 50% reduction in the minimum drawdown for super pensions. Thankfully, it would seem that superannuation has lost its proclivity as a fiscal punching bag. Apparently, deficits don’t matter as much as they used to, and the retiree vote is a lot more important. Despite Treasurer Frydenberg benefiting from a strong economy, the budget is forecast to show a $78 billion deficit for the 2022-2023 financial year following a $79.8 billion shortfall in the current year. It should be noted that the deficits are well down on what was forecast in last year’s budget, $106.6 billion and $99.3 billion, respectively, but are still among the largest on record. Since Treasurer Frydenberg used his 2019-20 budget to forecast a surplus, the Coalition is on track to record deficits worth a combined $524 billion by 2026, and the path back looks like a long and winding road for future governments of any persuasion. The majority of you will have read the facts and figures and by now will have an understanding of the proposed measures. Normally our summary would not be a simple reiteration of these facts, however this year (from a financial planning perspective), there is so little that the normal ambiguities are distinctly missing. Nonetheless, we seek to report on the relevant measures with clarity. As always, we will have to wait for the actual legislation to be passed and receive Royal Assent (which is likely subject to the May election results). Our 2022/23 Federal Budget report can be found here.

|

|

| Every Federal Budget is, of course, a balance of politics and economics. Treasurer Josh Frydenberg 2022/23 Budget is seemingly no different with a raft of short-term goodies, including; a reduction in fuel excise, a temporary tax cut of $420 for 10 million workers and a payment of $250 to 6 million welfare recipients. Perhaps the sting in the tail here is that most of this additional spending relates to this calendar year – excise is scheduled to return in six months, and the entire $1,500 Low and Middle Income Tax Offset (LMITO) will end next financial year (we note that both problems are the other side of the election, so we’re guessing its something to sort out later…).

So, what is to be made of the announcements? In summing up ‘the good, the bad and the ugly’, we share this sage perspective from AMP Chief Economist Dr Shane Oliver and Senior Economist Diana Mousina. The budget contains a number of commendable measures:

However, at a micro level, the budget may be criticised on the grounds that:

At a macro level, there are two big risks flowing from the budget:

The full article can be found here.

|

|

| Our view that the Reserve Bank of Australia (RBA) will be slower to raise rates than other major central banks around the world, particularly the US Federal Reserve, remains – this is a positive as it means monetary policy will be more supportive for economic growth.

It is important to view this budget against the backdrop of an increased focus on what central banks are looking to do this year. And as previously mentioned, a significant amount of front-loaded stimulus could be enough to see the RBA raise rates faster than expected. With this in mind, it is less about the budget deficit and more about the fiscal thrust (i.e. the change in the budget position relative to last year). Whilst the budget deficit is running close to 3% of GDP, this is very similar to last year, and thus the fiscal thrust is close to zero. In our view this reduces the risk of the RBA raising rates faster than previously predicted. Experts are forecasting a first-rate hike around May/June and the cash rate to reach 1% by year-end and 1.5% next year. The extra stimulus in the budget increases the chance that the first-rate hike may be higher than originally predicted but is unlikely to contribute to the general upward trend. It is important to remember that like the US, the market is well ahead of the central bankers, meaning rate hikes are already factored in well in advance. This should hopefully mean less negative reaction when the hikes arrive.

|

|

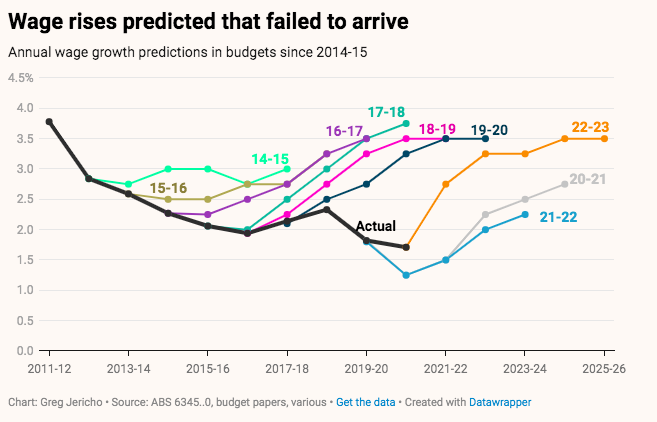

| On the labour market, the budget adopts very similar forecasts to the RBA — with the unemployment rate expected to dip below 4% in coming years, but wage growth fairly contained at below 3.5%.

Interestingly governments have not had a great record of forecasting wages as our chart of the week depicts. It is easy to justify actual wage growth figures coming in under budget estimates based on historically low inflation, but other forces such as imported labour, technology advancements and a benign industrial relations environment have also played a significant role. With inflation rising, if we continue to undershoot budget forecasts on wage growth, it will highlight the impact of these other forces. Will we see the budget estimates start to miss on the downside, or are we actually about to see some wage growth?

|

|

| The fiscal setting in Australia plays a small role relative to the overall momentum of the economy.

At the margin, the support to household incomes should provide support to the consumer discretionary sector of the Australian equity market, while the increase in infrastructure spending is additive to construction earnings. The measures relating to the housing market are going to be offset by the dampening impact that rising interest rates is having on-demand, and so the impact on demand for mortgages (and earnings for the major banks) will be more mixed. In terms of rates and government bonds, this budget is unlikely to contribute to the general upward trend in interest rates. As noted above, we don’t think that the budget announcements are significant enough to change the path of RBA cash rate increases. Finally, on currency, given there is limited fiscal thrust and no associated impact on interest rates, it is hard to make the case that this budget will have a noticeable impact on the Australian dollar. That said, we continue to think that the Australian dollar has some more upside left, given positioning is still quite negative (i.e., a lot of negative news is still priced in), commodity prices remain elevated, and economic growth is accelerating (as compared to decelerating in many other countries). In summary Cash and term deposits – cash returns are poor, but they will start to rise as the RBA starts hiking from mid-year. Bonds – ongoing budget deficits add to upwards pressure on bond yields. The rising trend in yields resulting in capital loss means that long-dated bond returns (as opposed to short-dated securities) are likely to suffer. Shares – more fiscal stimulus, strong growth and still-low rates all remain supportive of Australian shares, but rising bond yields & RBA hikes will result in a more constrained & volatile ride. Property – more home buyer incentives are unlikely to offset the negative impact of poor affordability and rising mortgage rates in driving a cyclical softening of house prices. The $A – strong commodity prices point to more upside. |

|

|

| A slight detour from all things budget.

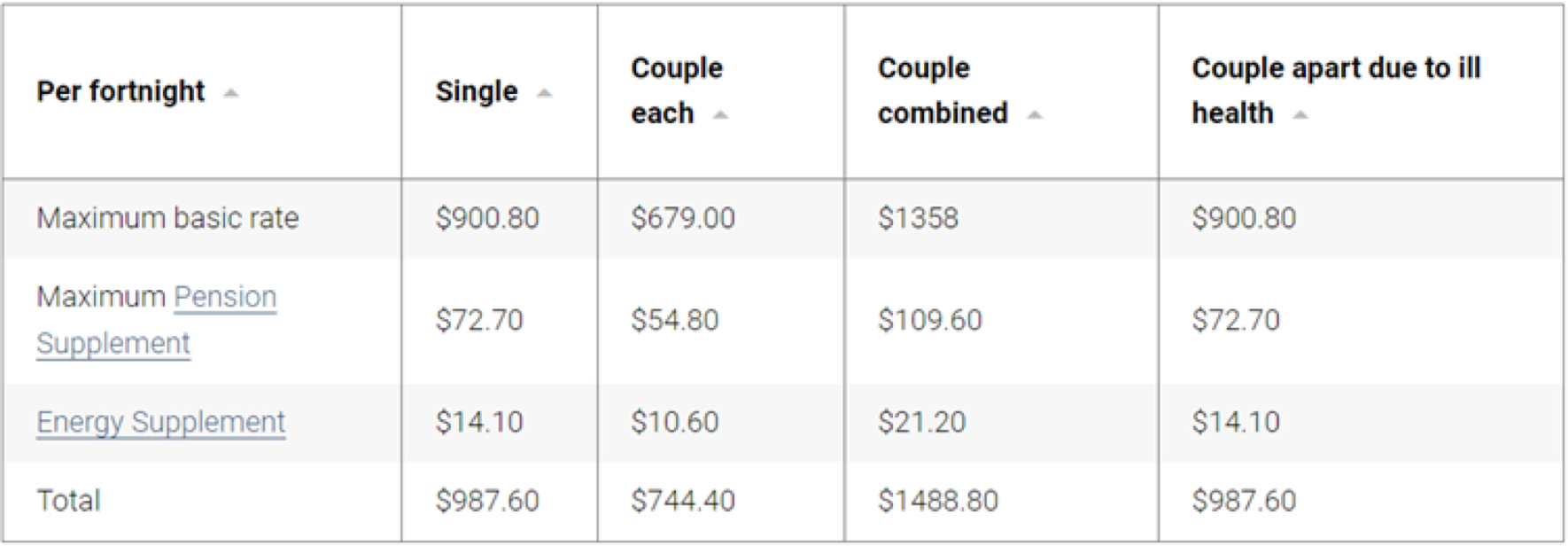

In March, Australia’s age pension rose to reflect inflation and the growing cost of living pressures. This change represents a pay rise of just over 2% and is the biggest increase in the payment in almost a decade. Single pensioners will be $20.10 better off per fortnight, and couples up to $30.20 per fortnight (where both members of the couple are eligible). Indexation also means that some people who were previously ineligible for a pension may become eligible as the cut-off amounts of assets and income are also increased. Payments The maximum rate of age pension payment for singles increased by $20.10 per fortnight from $967.50 to $987.60. The maximum rate for couples increased by $15.10 each from $729.30 per fortnight for each eligible member to $744.40. A couple where both members are eligible to receive the maximum payment can receive $1,488.80 per fortnight or $38,708.80 per year combined.

Assets For homeowners who are single, the asset test cut-off increased from $593,000 to $599,750. For couples it increased from $891,500 to $901,500. For couples who are separated by illness, as is the case when one or both move into aged care, the cut-off increased from $1,050,000 to $1,063,500. *It’s important to remember that the value of your home is not included in these assets. IncomeFor singles, the amount of income you can earn before the age pension ceases has increased from $2,115 per fortnight to $2,155.20. For couples, the cut-off has increased from $3,237.20 per fortnight to $3,297.60. *It’s important to remember that income earned under the work bonus (up to $7,800 per year) is not included. Income from investments is based on deemed income rather than the actual income earned.

|

| At a time like this (post budget, pre-election) our news feeds, inboxes and social platforms are literally saturated with ‘new’ news and opinion pieces – navigating the noise is not always easy.

This may be a clip from 2016, but Denzel Washington’s message is as profound as it is provocative.

|