Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View – SuperConcepts Update, Juxtaposition, Bill Shock, ChatGPT & The View and More

16th June 2023

Earlier this week, the Albanese government released its first response to the Quality of Advice Review (QAR), an independent review commissioned by the previous government (led by Michelle Levy) with the goal of simplifying the laws governing financial advice. It has accepted 14 of the review’s recommendations “in full or in principle” but left the door open on eight more.

As a financial advice firm, we have been very hopeful about the results of this review, but we will spare you every twist and turn of the legal fracas. This said, its outcome matters for every investor and, indeed, every household in Australia.

According to the latest figures, just 10% of Australians receive professional financial advice. Why? A big reason is the increasing costs due to onerous compliance and red tape.

The review concluded that “20 years’ worth of complex and overlapping laws aimed at cleaning up the once-wayward sector” are to blame for the problem.

The government has broadly accepted this thesis and has agreed to act. First, it will remove some hefty paperwork for professional advice, and second, it will allow superannuation funds to get more advice to members to help them move into retirement.

Reducing the red tape for advisers and super funds is in the public interest. Long legal (compliance) documents are not helpful for anyone. The estimated 3.6 million Australians moving from the accumulation phase to the retirement phase of superannuation over the next 10 years would probably agree.

Most of them – especially middle-income earners – will retire on a mix of superannuation, personal savings and investments or the equity in their home. This means they face difficult decisions such as how to draw down their superannuation savings, whether they should downsize to a smaller home (and take advantage of government incentives), and how the aged pension and/or a decumulation product fits the strategy. Let’s also not forget that regardless of means, one of the biggest fears of retirees is outliving their money. This is the guidance that qualified financial advisers are best placed to give.

The country desperately needs a model that allows advice firms to concentrate on the delivery of quality advice (accessible by as many people as possible) rather than compliance and red tape. QAR was a step in the right direction, and now with bi-partisan support for more than half of its findings, we may just have lift-off.

Economic and Market Update

As one fund manager cleverly described in a missive this week “as we approach the middle of the year, the Australian economy is transitioning through the current cycle in a ‘hop, skip and a jump’ fashion”.

For now, the economy is ‘hopping’ along better than expected after such an abrupt rate hiking cycle. This resilience has markets considering if a few further rate hikes may be needed to complete the intended slowdown in spending needed to dent demand-driven inflation. Central Bankers know they have already done a great deal in moving rates quickly to restrictive territory, and whilst they acknowledge inflation is yet to fully moderate, they are trying to buy time, knowing the lag effect will complete the process at some stage, and therefore much of their communications references ‘skipping’ a few meetings on the road to further rate hikes to access more incoming data.

Due to the long and variable lag effects of monetary policy, any further hikes now will likely continue to affect the economy well into 2024, meaning at some point, the cumulative tightening will trigger the economy to ‘jump’ into a protracted slowdown, killing inflation and allowing for a new cycle to be born as monetary policy moves away from restrictive settings.

There is significant divergence as we look around other developed economies, with each country now embarking on its own rates journey.

Last month the Reserve Bank of New Zealand (RBNZ) completed its rate hiking cycle, lifting rates to 5.50% and, importantly, telegraphed that it expects to now remain on hold at this level. This is important, as the RBNZ was one the first and fastest rate hikers in this global cycle. The New Zealand economy is currently in recession, with a raft of negative economic data across the board (retail sales, consumer confidence, activity outlook, and business confidence all negative).

The US Fed also paused (or skipped) hiking rates this week, as it too wishes to view more data and access the fallout from the regional banking crisis. US data has also been patchy, with weak purchasing managers index (PMI) readings and weak (negative) regional confidence or outlooks from a raft of areas.

The bond market is telling us that the US will enter a recession, yet the equity market is predicting a soft landing. No wonder investing is hard! Our philosophy – ‘hope for the best, prepare for the worst’.

Looking ahead, there are many pressing issues that could propel markets into the ‘jump’ territory. The prevailing belief among market participants is that this outcome is ultimately inevitable. While the specific triggers and timing are uncertain, given the recent significant interest rate hikes and the shift towards more restrictive measures, the anticipation is that the future will present a more demanding and challenging environment.

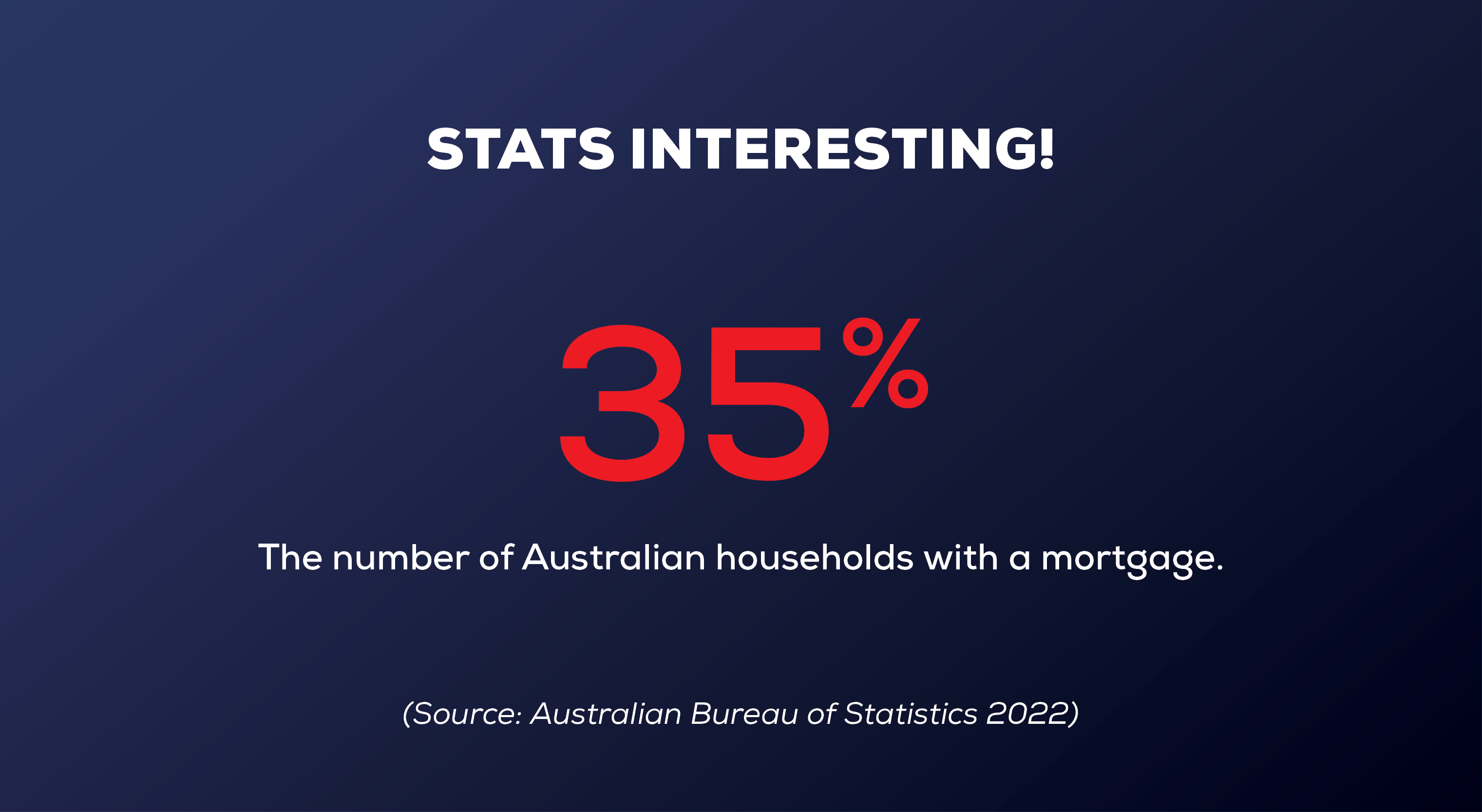

This figure may surprise some people, for a nation ‘obsessed’ with property, we certainly thought it would be higher.

Our point is that it makes controlling inflation a big challenge when interest rates only compromise a third of Australian households. This and the fact that rising interest rates actually benefit other segments of the population – savers. A retiree who has for the last few years been unable to get more than half a percent on a term deposit can now demand something in the high fours.

For the Reserve Bank trying to slow the economy, this is a real juxtaposition – on the one hand, they raise rates which hits mortgage holders hard and slows spending. On the other hand, they are putting more money in the pockets of retirees.

As if the millennials didn’t have enough reasons to be grumpy about the boomers!

The solution lies in policy beyond the central bank. Interest rates are but a blunt instrument and arguably less effective than ever. What we would really like to see is a government focused on progressive tax policy and productivity-based wage rises that can work in tandem with the central bank in fighting inflationary pressures.

Collaboration between fiscal and monetary authorities is crucial. Policy coordination can help strike a balance between supporting productivity growth, managing income distribution, and maintaining price stability. It requires careful analysis, monitoring, and adjustment of policies to ensure they are implemented in a manner that supports both economic growth and inflation control.

With so much else going on in Canberra, we hope this does not slip through the cracks.

Housekeeping Matters

Re: SuperConcepts

This week we received communication that self-managed superannuation administration provider, SuperConcepts has announced a shift to private ownership.

The business has been acquired wholly from the AMP and will not be merged into an existing venture. The AMP’s challenges over the last couple of years have been widely documented, and SuperConcepts believe that this new operating structure will provide them with the necessary focus needed for improved innovation and investment.

Having spoken directly with our representatives at SuperConcepts we have been assured that all parties will co-ordinate closely to ensure a seamless transition and smooth continuation of client services. Most importantly, there will be no change for our business or our clients.

Should you have any questions, please do not hesitate to contact your adviser.

Super Savings & Strategies

It’s that time of year when we all look at what last-minute things we can do to maximise tax savings. In the words of the late Kerry Packer to a Senate estimates committee, “Of course I am minimising my tax. And if anybody in this country doesn’t minimise their tax, they want their heads read.”

Tax deductions for topping up super

You can make up to $27,500 in concessional contributions each year, assuming your super balance has not reached its limit. If the contributions made by your employer or under a salary sacrifice agreement have not reached this $27,500 limit, you can make a personal contribution and claim a tax deduction.

For those aged between 67 and 74, you will need to meet the ‘work test’ to contribute personal concessional contributions and claim a deduction – you must have worked at least 40 hours within 30 consecutive days in a financial year before your super fund can accept voluntary contributions from you. To be able to claim the tax deduction for these contributions, the contribution needs to be with the super fund before 30 June (watch out for processing times). You will also need to lodge a Notice of intent to claim or vary a deduction for personal super contributions with your super fund before you lodge your tax return to advise them of the amount you intend to claim as a deduction.

Bringing forward unused contribution caps

If your total super balance is below $500,000, and you have not reached your cap in the previous four years, you might be able to carry forward any unused contributions and make a larger tax-deductible contribution this year.

For example, if your total concessional contributions in the 2021-22 financial year were $10,000, you can ‘carry forward’ the unused $17,500 into this financial year, make a higher personal contribution and take the tax deduction. This is a helpful way to reduce your tax liability, particularly if you have made a capital gain.

If you have never used your contribution cap, for example, you have recently become a resident or have returned from overseas, you can also bolster your superannuation by contributing five years’ worth of concessional contributions in one year (assuming you have not reached your balance cap).

Doubling the benefit for SMSFs

For self-managed superannuation funds, a quirk in the way concessional contributions are reported means that a concessional contribution can be made in June but not allocated to the member until 28 days later in July. The practical effect is that a member can make a contribution of up to $55,000 this financial year (2 x the $27,500 cap – assuming you have not used your cap) and take the full tax deduction, but the fund recognises the contribution in two amounts; one amount in June and the second allocated to the member from the SMSF’s reserve in July. This strategy is particularly helpful for the self-employed who need to boost their superannuation and reduce their tax liability in a particular year.

Top up your partner’s super

With a cap on how much you can transfer into a tax-free retirement account, it makes sense to even out how much super each person holds to maximise the tax savings for a couple. If your spouse’s assessable income is less than $37,000, make a contribution of $3,000 or more on their behalf, and you can take a tax offset of up to $540. Another way of topping up your spouse’s super is super splitting. If your spouse has not retired and is below their preservation age, you can roll over up to 85% of a financial year’s taxed splittable contributions to their account.

For more information on these strategies (and more), please talk to your adviser.

Wealth Wisdom

With the end of the financial year upon us, some wise words:

“I have watched many people squander their tax return, considering it ‘free money’. Not true … you worked for that money, so put it to good use.”

— Jessica Brady, Financial literacy advocate

Jessica advises splitting your tax refund into three buckets: 50 per cent into your long-term savings and investing plan, 30 per cent for self-improvement such as a vocational course or activity, and the remaining 20 per cent for something that brings you joy.

Bill Shock

If you’ve received an insurance policy renewal of late, chances are you may be suffering a bout of ‘bill shock’. Insurance premiums (whether it be your house, car or life), are up. Floods, fires and difficult investment markets mean insurance companies are re-building their books. On the life insurance front, there are some different forces at work.

Whilst we all expect life insurance companies to increase premiums as we age and as our cover increases with inflation, what we don’t expect are significant increases as a result of seismic shifts in the way that the underlying financials of the industry work. The below serves as an insight into the changing landscape of the life insurance industry.

- Increased life expectancy – Australians are living longer on average, which means life insurance policies may need to cover a longer period. Insurers adjust premiums to account for the extended duration of coverage, increasing the cost.

- Regulatory factors – Regulatory requirements, such as capital adequacy regulations and compliance, have added huge costs to life insurance companies and, in-turn, influence the pricing of life insurance premiums.

- Protect Your Super (PYS) – The PYS measures in Australia aimed to address issues of unnecessary erosion of superannuation accounts. While these measures were introduced with good intentions, they have also had unintended consequences.

Specifically for life insurers, the cancellation of insurance policies for inactive accounts meant they lost economies of scale and increased their risk pool due to the removal of low-risk policyholders. With a smaller pool of insured individuals, insurers have to spread the cost of providing insurance across a reduced number of policyholders.

In short – PYS was an important measure, but due to the apathy of the nation, it has somewhat undermined the economics of the entire system.

- Medical Advancement – healthcare costs and medical advancements have had an impact on premiums. As medical expenses rise over time, insurers will have to adjust premiums to cover potential costs associated with policyholders’ medical care and treatment.

What to expect

Be warned; premiums are up…

But let’s not forget the value of life insurance; financial protection for dependents, debt coverage, business continuity, estate planning, tax management and, of course, peace of mind.

What to do next?

If you haven’t had your policy’ stress tested’ for some time, there may be scope to ‘re-optimise’. If in doubt, we encourage you to talk directly with our resident risk expert Gerry McAvoy – a conversation won’t cost you a thing, but it could save you a lot.

Gerry can be contacted via email gerry.mcavoy@finsecpartners.com.au or by phone on 08 8357 7840.

Friday Funny

No wonder English is such a hard language to learn!

ChatGPT on The View

Finally, inspired by our recent articles on AI, we asked ChatGPT the question: “Describe (FinSec Partners) Australian finance newsletter, The View in 100 words or less”. To which it replied:

The View is a highly regarded Australian finance newsletter delivering timely and insightful information to its subscribers. Produced by a team of financial experts, this newsletter offers a concise and comprehensive snapshot of the financial landscape. Packed with market analysis, investment trends, economic updates, and expert commentary. The View equips readers with valuable insights to make informed financial decisions and stay ahead of the curve. Whether you’re an investor, business professional, or finance enthusiast, The View provides a trusted source of knowledge, helping you stay updated on the latest developments and navigate the complexities of the financial world in Australia.

Perfect. Further evidence of how good this AI is.

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.