Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Russia invades Ukraine, Wage growth, Who is Stephen Jones and More

|

25th February 2022 |

| The Russia-Ukraine issue is dominating every newsfeed, with the disturbing escalation of events over the last 24 hours. As you will be all too aware yesterday, Russian President Vladimir Putin ended weeks of speculation declaring war on Ukraine, claiming Russian self-defence as he sought to demilitarise and replace its leaders.

As disturbing as these events are, they are not entirely unexpected. It was widely speculated that Putin would see the backdrop of the Winter Olympics as a suitable window to make his move. He has some history in this regard. Putin invaded Georgia in August 2008, just before the 2008 summer Olympics (Beijing) and invaded Crimea in February 2014, right after the end of the 2014 winter Olympics (Sochi). An attack during the Beijing winter Olympics would have been a poor strategic move for Russian Chinese relations (a relationship that is very important to Putin given his reduced sphere of influence on Russia’s Western Front). A move shortly after the games is consistent with his prior playbook. Of course, the real driver behind Putin’s aggression seems to be a personal mission to rewrite the history of the end of the Cold War. He is pushing 70 and is hungry to reverse what he has seen as the erosion of the Russian empire post the collapse of the Iron Curtain. And, if it is personal, then Putin’s appetite for risk may be much higher. On every level, these are significantly troubling events, and the prospect for substantial loss of life and destruction of livelihoods is first and foremost in our minds. Moreover, there is the potential for further escalation in events from here and additional humanitarian and economic implications. Over the last couple of weeks, we have spent considerable time speaking with our world of experts and analysing the impact these military actions will have on share markets – our lead article this week serves to provide a summary of views. |

|

| For many investors who haven’t seen anything like this in their lifetimes, it’s understandably difficult to anticipate how markets will react.

The initial reaction (military crises inevitably trigger abrupt selloffs) reflects a combination of uncertainty around how far the conflict will go. Namely:

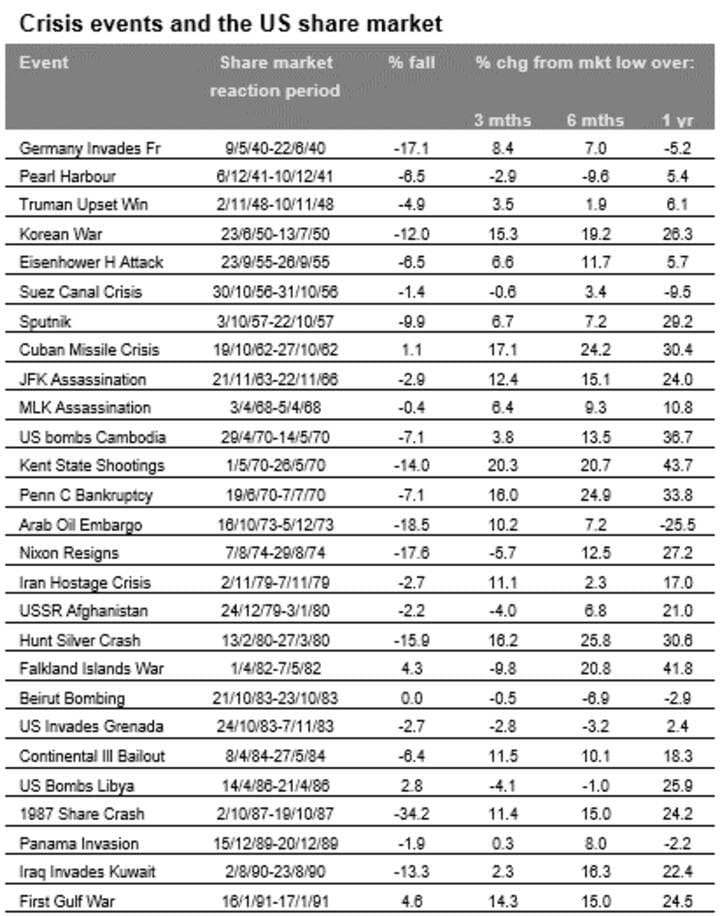

The European Union depends on Russia for an estimated 40% of its gas supplies (Germany relies on Russia for 50% of its gas, and Austria is 100% dependent). About a third of those flows are via Ukraine. Low fuel inventories last year sent prices to record levels, and volumes from Russia have been reduced since the second half of 2021. The outbreak of the conflict has thrown this critical energy supply into question, and the response from energy markets to this uncertainty has been as you would expect. In Europe on Thursday, gas futures were trading up over 50% at some points. European coal futures gained over 20%. While some of this will represent an initial overreaction to events unfolding, we can expect continued pressure on energy supply and energy prices for the foreseeable future. Crisis and share markets Of course, there is a long history of various crisis events impacting share markets. This includes major events such as wars, terrorist attacks, financial crisis etc.. Interestingly, whilst they always trigger immediate selloffs, they have almost all recovered to above their pre-crisis levels within months. The following table (taken from a recent article by AMP Chief Economist Shane Oliver) shows such events since World War Two (the first column), the period over which the US share market initially reacts (second column), the percentage share markets fall (third column) and the percentage change from the low over 3, 6 and 12 months in the final three columns.

The pattern is pretty much the same – An initial sharp fall followed by a rebound. Since World War Two, the average decline has been 6%, but six months later, the share market is up 9% on average and one year later, it is up around 15%. This consistency is attributed to the fact that military activities generally lead to increases in demand, spending, company revenues and profits and therefore are positive for share markets, especially Australia since military activity leads to higher commodities prices. The share selloffs are merely an understandable human reaction to the shock of the event and the associated alarm of the media reaction. Events such as these are not necessarily catastrophic for markets. More broadly and perhaps most significantly will be the reaction of the US Federal Reserve. Rising oil prices feed into inflation numbers and therefore drive the risk of more aggressive rate hikes. Conversely, rising energy prices may cause slowdowns in spending and economic growth and jobs – which is why bond yields have been declining in recent days. The oil price can be just as effective in managing the speed of an economy as interest rates. It makes for a complex situation indeed! We have been anticipating this potential development, and while it certainly concerns from a humanitarian standpoint, we are not alarmed by it from an investment perspective. We continue to monitor the situation as it unfolds and consider the implications for our clients. No doubt this will continue to be a talking point in the FinSec View for some time to come.

|

|

| The Australian Wage Price Index (WPI) measures changes in the price of labour in the workforce. The Australian Bureau of Statistics this week published the WPI for the last quarter of 2021 showing a 0.7% increase in seasonally adjusted terms, and in line with economists’ estimates.

On a yearly basis, the WPI was up 2.3% on the previous December quarter, the sharpest (seasonally) adjusted rise since the September quarter of 2018. The quarterly increase was enjoyed equally by private and public sector workers but on an annual basis those in private jobs enjoyed a 2.4% increase compared with 2.1% in public sector work, the ABS reported. By contrast, consumer prices rose 3.5% in the December quarter from a year earlier, while the underlying inflation increase was 2.6% when more volatile changes are removed. In simple terms, the rate of wage increases failed to keep pace with the increased cost of living and this has driven speculation that the wage rise pressures will continue to build in 2022 and further add to the inflationary pressures on the economy. At this point, the RBA retains a much more passive stance on interest rate increases than their counterparts in the US Federal Reserve. RBA Governor Philip Lowe said this month it would be good to see a couple more quarterly inflation reports before lifting interest rates. Based on when these reports are published (following the end of the quarter) this would make August the earliest point at which the RBA could lift rates. Lowe maintains that he still believes wage growth must pick up to about 3% for inflation to be sustainably in the 2% to 3% target band.

|

|

| In reading this week’s editorial for Firstlinks, managing editor Graham Hand opened his missive with a powerful story.

We share it with our readers, not to be alarmist but to remind us all that estate planning is often one of those items left on the ‘to do’ list – Something we will get to tomorrow. Unfortunately, a tomorrow job bellies the fact that illness and death strike thousands of Australians every day and it can happen to anyone. If this hits a nerve, please take action and talk to your adviser. Last year, two of my close friends passed away, both in their late 60s. One was undergoing cancer treatment, so it was not a major surprise although he had been improving. The other suffered a heart attack while he slept at night, and his passing was a massive shock. Putting aside the personal tragedy, in both cases, their estates were left to their wives who had not been heavily involved in managing their investments. Both are strong women capable of handling the stress but not everyone has their fortitude. One wife turned to the financial adviser her husband had worked with, but the other was forced to quickly pull together the financial pieces. There are additional complexities with SMSFs. Most are managed by a dominant trustee, usually the husband, yet women have longer life expectancies. It’s possible the surviving spouse will not want to continue to manage the investments, there are tax and estate implications and some assets may be illiquid. Regardless of personal circumstances – health or financial – we should all take the time to ensure spouses or partners know in advance what steps to take if someone dies or becomes otherwise incapacitated.

|

|

On 10 February, a number of changes to superannuation were passed into legislation. Regulations are yet to be drafted; however, these changes are set to come into effect from 1 July 2022. A summary is provided below.

The $15,00 contribution limit per financial year remains unchanged.

Note: funds must be preserved within the super account until such time he or she can meet a nil condition of release.

Note: Individuals aged between 67 and 75 who wish to make personal deductible contributions to super will still be required to meet the 40-hour work test. These changes formed part of previous announcements and more information can be found in our Budget report here.

|

|

| As election season nears, speculation naturally builds regarding the likely policy platform the leaders and their parties will take to the electorate come May.

And so, we ask the question, how many people know Stephen Jones, the ‘shadow’ Labor minister in Jane Hume’s portfolio of financial services and superannuation? Given the polls suggest the May election will be close, it is worth understanding his views. Mr Jones was a guest of honour at the PritchittBland Communications New Year kick-off on 27 January 2022 in Sydney. To a room of financial services executives and media, he delivered a speech outlining his views on the financial services industry and the opportunities ahead. An excerpt from that speech can be found here. Spoiler alert he has strong opinions around various reforms imposed on advisers and (seemingly) has no real appetite for further major reforms to superannuation.

|

|

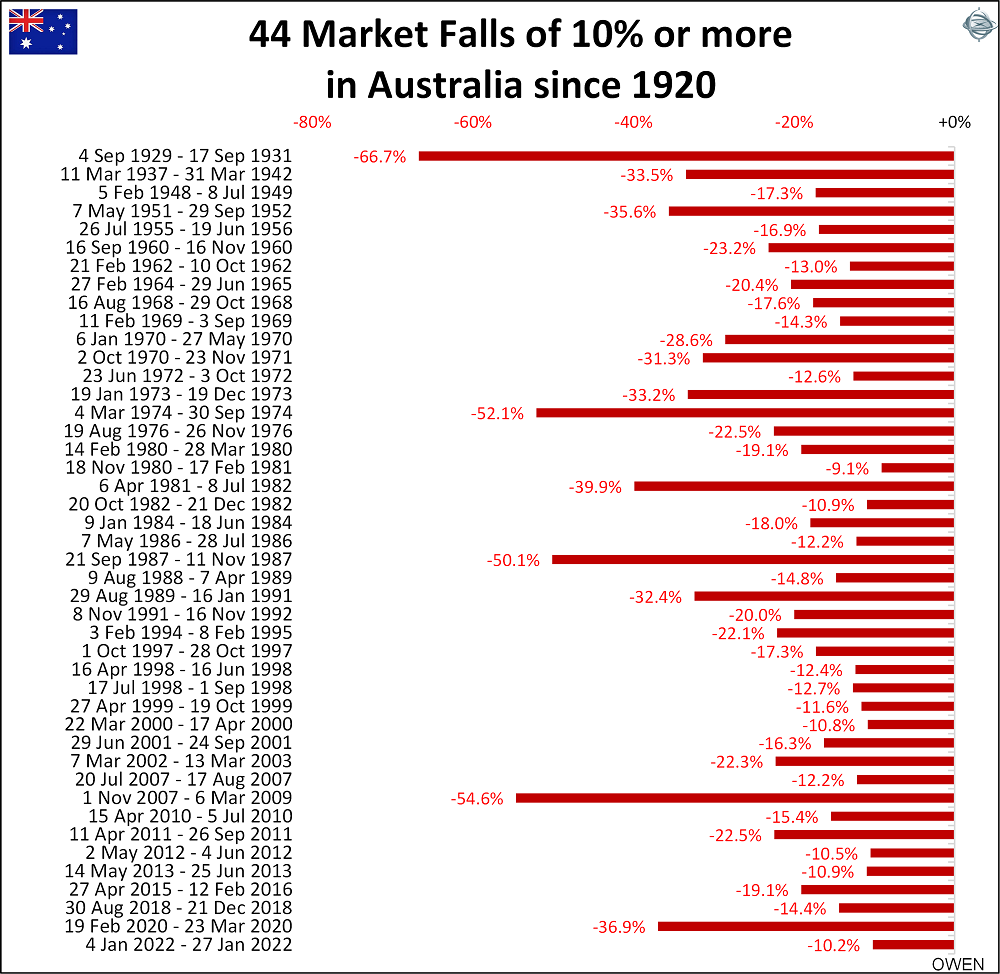

| This is a chart we often use with clients, and it never fails to surprise. The data shows the reality of share market investing and serves as a vital reminder for all investors.

Share prices will fall by at least 10% every two or three years, by 20% a couple of times each decade, and by 30% to 50% every generation (defined as 20-30 years). Nobody is immune, and it is a reality that investors must accept it if they want long-term rewards from equities. The good news is regardless of these falls, markets have always recovered beyond their previous highs and paper losses are usually only realised by those that sell. As always, be patient and rely on Albert Einstein’s 8th wonder of the world – the slow compounding of wealth in quality companies.

Source: Ashley Owen, Chief Investment Officer Stanford Brown |

|

| The pandemic has consumed our lives for the last few years, and it’s hard to imagine a more challenging time in a global sense. But, placed in the context of wars, famines, and natural disasters, it probably doesn’t get close to the worst periods in human history.

Should you have a fondness for history and a good constitution, then you might just enjoy this brief 24 minute podcast from NY based WYNC Studios RadioLab looking into ‘What was the worst year to be alive on planet Earth?’. RadioLab make a case for 536 AD, a year of catastrophes including; a supervolcano that saw ash and debris line the ground like a blanket of snow, casting a veil of darkness over Europe, the Middle East and parts of Asia. The ash ‘fog’ blocked the sun during the day, causing temperatures to drop, crops to fail, plagues of hungry rats and ultimately, people to die. It was, you might say, the literal Dark Age. Using evidence painstakingly gathered from around the world – from Mongolian tree rings to Greenlandic ice cores to Mayan artefacts – the podcast paints a portrait of what scientists and historians think went wrong and what it may have felt like to be there in real-time (not for the faint of heart).

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |

|

|